By Matthew Gaude & Shawn McGuire

The Federal Reserve concluded their March 19th/20th meeting by leaving interest rates unchanged, per the headlines from CNBC.com.

Key Takeaways

- The Federal Reserve left interest rates unchanged for the fifth straight meeting.

- The Federal Reserve reiterated the expectations that they will cut interest rates 3 times in 2024.

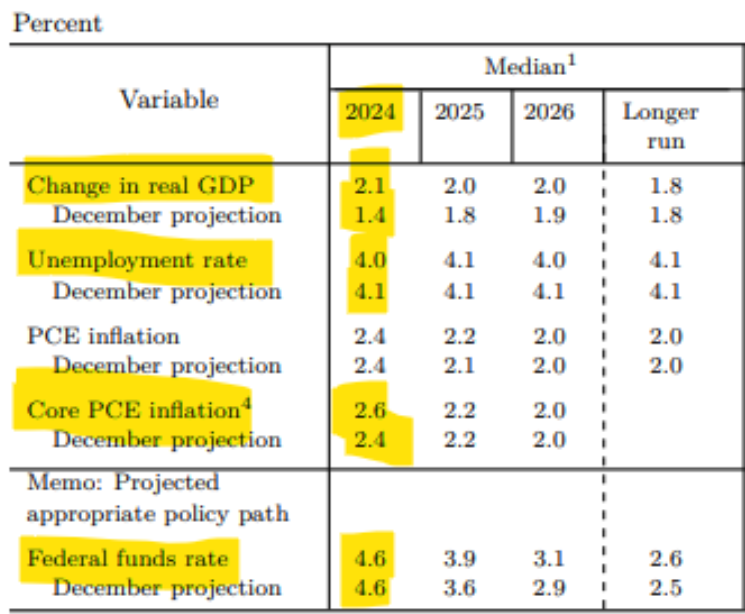

- The Federal Reserve increased their inflation forecast from 2.4% to 2.6%.

- The Federal Reserve increased their growth forecast from 1.4% to 2.1%.

- Inflation has eased but remains elevated; the Fed does not expect to start cutting interest rates until “greater confidence” inflation is moving toward their 2% target.

- Reducing interest rates too fast could reverse inflation progress.

The Federal Reserve made some tweaks to their Summary of Economic Projections, which they provide at the end of their meeting each quarter. After undershooting on growth all last year, by a lot, they increased their growth estimates (through 2026).

They see employment remaining strong, and inflation getting to target (“over time”).

Take a look at the federal funds rate highlighted area. These projections suggest the economy will be stronger, without increasing inflation, all while the Fed will keep interest rates higher than they thought just three months ago. As you can see, they’ve revised up the Fed Funds rate (interest rates) for 2025, 2026, AND in the longer run.

Source: https://www.federalreserve.gov/monetarypolicy/guide-to-the-summary-of-economic-projections.htm

What Does the Fed Decision Mean for Markets? Still All About Growth

The Fed decision was essentially not as bearish given the recent inflation data, and the practical impact of yesterday’s decision was to:

1. Keep markets expecting a June rate hike, and

2. Keep the “impending Fed rate cuts” part of the bullish mantra powering stocks higher intact.

So, a bullish forecast combined with a still-intact bullish narrative pushed stocks to new highs on Wednesday in the wake of the Fed decision. But if there was a “beneath the surface” takeaway from the Fed, it’s that the major focus for investors right now needs to be on growth, and specifically whether growth can hold up. There were some small hints that Powell and the Fed may be a bit more worried about growth than the market currently expects, but the bottom line is that the market is not getting more than three rate cuts in 2024 unless growth slows down, and at that point, it’s too late anyway.

Growth matters because it implies that interest rates are indeed going to be mostly higher for longer and higher rates will continue to act as a headwind on growth. Put differently, the relief from high rates that investors keyed on during the Q4 2023 rally is not coming. Yes, there will be two to three cuts barring a slowdown in growth, but we’re still going to end 2024 with interest rates over 4.5%. Markets have tolerated that disappointment well so far in 2024 for two reasons:

- First, artificial intelligence enthusiasm continues to rage, which is helping to keep the bull market alive and well.

- Second (and this is more fundamentally important), it’s because growth has held up. The market doesn’t care if we get fewer rate hikes as long as growth isn’t showing any signs of slowing. But if those signs of cracking do start to appear, then the fact that there will only have been one rate cut by July will matter—a lot—because policy will be viewed as restrictive and the outlook for markets will change, with the potential for a lot of market volatility.

Bottom line, with Fed policy known and major relief on rates not coming in 2024, we must focus on growth and make sure we see, as early as possible, any evidence of a rollover. Because if that happens, it’s a major problem for this market. And that’s exactly what we’ll be doing for you. For now, the bullish mantra of solid growth, falling inflation, impending Fed rate cuts, and artificial intelligence enthusiasm is alive and well and the S&P 500 has hit new highs. Until multiple points in the mantra are invalidated, the path of least resistance in this market remains higher…for now.

Takeaway

The Fed decision largely met our “What’s Expected” scenario as Federal Reserve Chairman Jay Powell mentioned three rate cuts in 2024 while forward guidance was unchanged, signaling that it’s unlikely the Fed will cut rates at the next meeting in May. During Powell’s Q&A session, he mentioned that the Fed “does not expect it will be appropriate to reduce their inflation target range until it has gained greater confidence” that inflation will move to the 2% target. Again, this was largely as expected and the net result was that rate cut expectations for June didn’t change (a June rate cut is still widely expected).

Turning to the Q&A session, Powell largely repeated what he said at the semi-annual Congressional testimony from two weeks ago, namely the Fed was getting closer to lowering rates but wasn’t quite there yet, as he wanted to see inflation continue to come down toward their 2% target. From a market standpoint, the reaction was one of relief as investors were concerned the Fed would be hawkish in response to the sticky inflation data. Since they were not, we saw a dovish response as stocks rallied and bond yields fell modestly. Bottom line, the Fed reiterated what markets have expected for weeks—that the Fed will start to cut rates in June. In this market, that’s good enough to spur a rally and that’s why stocks vaulted to new highs.

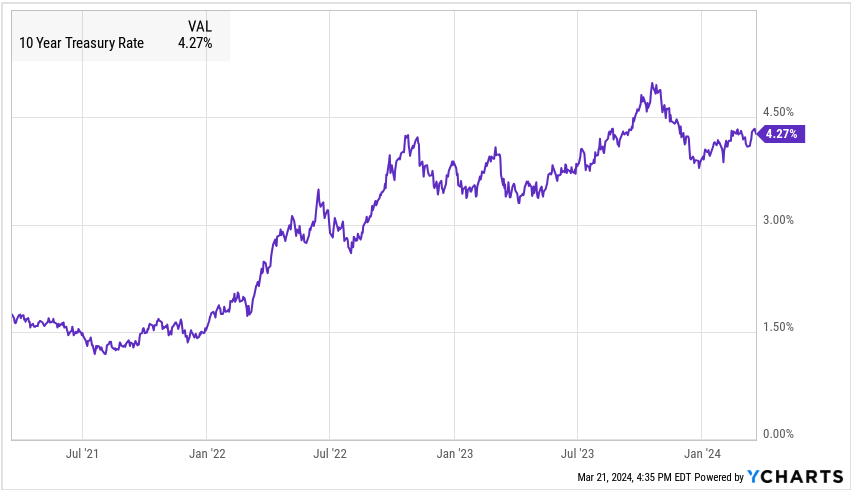

As a result, the 10-year Treasury rate ticked down to 4.27%. In our 2/27/24 update, the 10-year Treasury rate was at 4.28%, so not a lot of movement in the 10-year Treasury rate over the last month.

Bottom line, investors appear to already be reconsidering how three rate cuts in the next eight months are still warranted if growth is seen firming and inflation is going to be higher than previously thought. It presents a dilemma between theory and practice and underscores that the Fed is “stuck between a rock and a hard place” here as there are two major policy risks in play. If the Fed cuts too early, they risk reigniting inflation. If the Fed keeps rates high for too long, they risk sending the economy into a likely painful recession. A soft landing is still possible and markets are currently pricing in that outcome, however, we need to stay aware of the two aforementioned policy risks as they are both major threats to the long-term outlook for the rally in stocks.

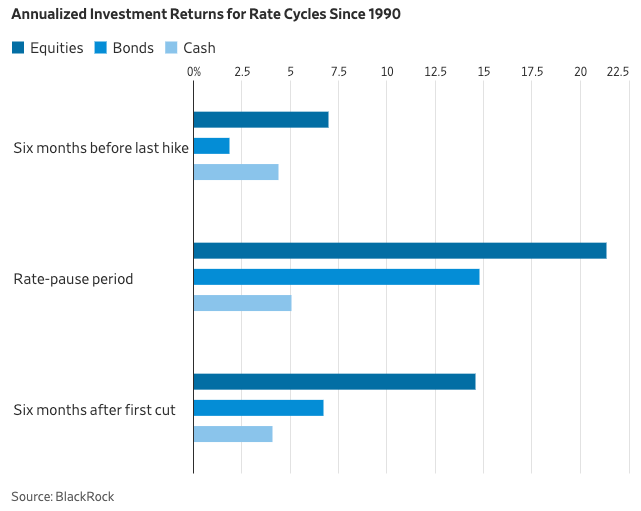

Stocks and bonds both tend to perform better in a pause before rate cuts than after, according to an analysis from BlackRock. Since 1990, stocks purchased in the six months after the first rate cut in a cycle have returned an annualized average of 15%, compared with a 21% return for investments made during the pause. Bonds returned an average 15% in the pause before the cuts and 7% afterward.

Affects On Our Fixed-Income Investment Strategy

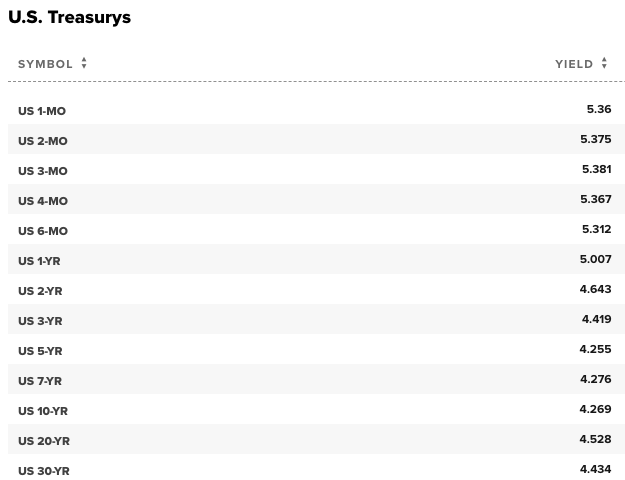

1. The first part of our strategy has been buying 3-month, 4-month, and 6-month T-Bills. The following rates are from CNBC.com on 3/21/24. Short-term rates have held relatively steady and will until the Federal Reserve starts to cut interest rates. At one point last year, we were able to get over 5.50% annualized interest on a 6-month T-Bill. Now the 6-month T-Bill is at 5.34%. Our strategy has been, when T-Bills are redeemed, we have been able to reinvest at the same to higher rates than before. We may not have that chance anymore. We knew this opportunity would not last forever, however, we wanted to take advantage while we could. Short-term rates will not be going lower immediately, but will be dependent on when the Federal Reserve cuts interest rates. T-Bills and money markets have been the fixed-income investment of 2023 for risk-free money and continues to be with over $6 trillion in money markets and cash equivalents. This will change, but not overnight. Risk-free rates at 5% are still attractive, which allows us to continue reinvesting in 3-, 4-, and 6-month T-Bills until the Federal Reserve lowers interest rates below the 5% threshold.

Following are interest rates as of 3/21/2024. There has been very little change in short-term Treasury rates as the 3-month and 4-month have been around the 5.36%-5.39%.

2. Intermediate-term (12 month) bonds. Since 2022, we have been purchasing high-quality bonds from banks such as JPMorgan, Wells Fargo, Bank of America, Citigroup, and Royal Bank of Canada. When we first started buying bonds toward the end of 2022, we were receiving 4.50% on a Royal Bank of Canada bond that matured on 11/20/2023. We have seen interest rates come down from the 5.7% JPMorgan 12-month corporate bond that was issued several months ago. Unfortunately, there are very few quality bonds being issued currently. Those that are being issued are with interest rates between 5.2-5.3% over a 12-to-24-month time period. As these bonds mature, we are reinvesting in our core bond funds as well as several new fixed-income funds we have purchased.

3. The third part of our 3-pronged strategy has been our Leader High Quality Income Fund, and our Allspring Short-Term High Income Fund. They have been part of our core fixed-income portfolio and have performed very well.

We are very happy with the performance of both the Leader High Quality Income Fund and the Allspring Short-Term High Income Fund, as outlined in our 2/27/24 update.

In the meantime, we will continue to eagerly earn higher rates of interest at current levels.

A Short Bond Lesson

There is an inverse relationship between bond prices and interest rates. As interest rates go lower, bond prices go higher and vice versa. So, although we will be earning less interest, bond prices will go up, thus increasing the value of the bonds in our funds. If you go back to the Allspring Short-Term High Income Fund chart above and look at the time period from October-December 2023 when interest rates declined from 5% to 3.79% on the 10-year Treasury, this is an example of when interest rates declined substantially, thus increasing bond prices and the effect on returns.

We have also added some additional bond funds to your account, which we will discuss in more detail with you during our meetings. If you would like to set up a review now, you can simply click here to schedule an appointment online.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.