By Shawn McGuire & Matthew Gaude

This is the headline from CNBC on November 1st, after the Federal Reserve meeting.

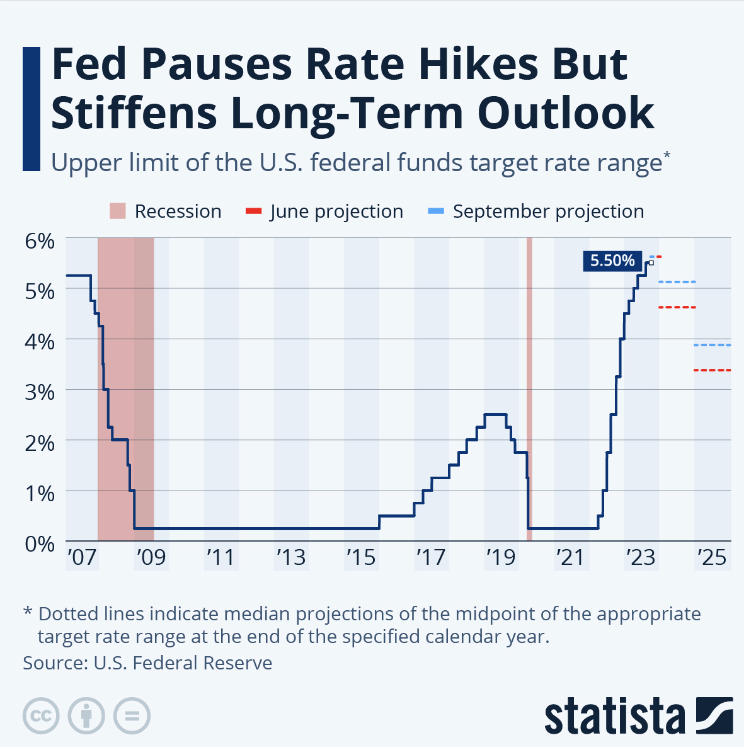

Following their two-day meeting ending November 1st, the Federal Reserve decided not to raise interest rates this month. This was the second consecutive meeting the Federal Reserve chose to hold rates steady, following a string of 11 rate hikes, including four in 2023. The Federal Reserve kept interest rates at 5.25% for the time being. Federal Reserve Chairman Jay Powell mentioned during the press conference, “The process of getting inflation sustainably down to 2% has a long way to go.” Powell, in his remarks at a news conference, stressed that the central bank “hasn’t made any decisions yet for its December meeting.” These comments reinforce our belief that interest rates will continue to stay at these high levels until at least mid-2024.

The Federal Reserve did not hike rates, nor did they make any change to “Forward Guidance,” meaning that, technically speaking, rate cuts are now officially over. However, while the statement had minimal changes, there was one change I do want to point out. In the second sentence of the second paragraph, the Fed stated that “Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity….” That was a change as the Fed added the word “financial” in what is a clear nod to the fact that the 10-year yield is at decade-plus highs, and that will help slow growth.

In plain English, the Fed is saying officially that higher rates are doing its job, and the practical takeaway from that is that the bar to raise rates further is now higher than it was in September. So, while the Fed did not change the statement to officially signal rate hikes are over, they did make a change that very strongly implies it. From a market standpoint, the market acknowledged that change as the 2-year yield fell several basis points to the lows of the day while the dollar dipped slightly.

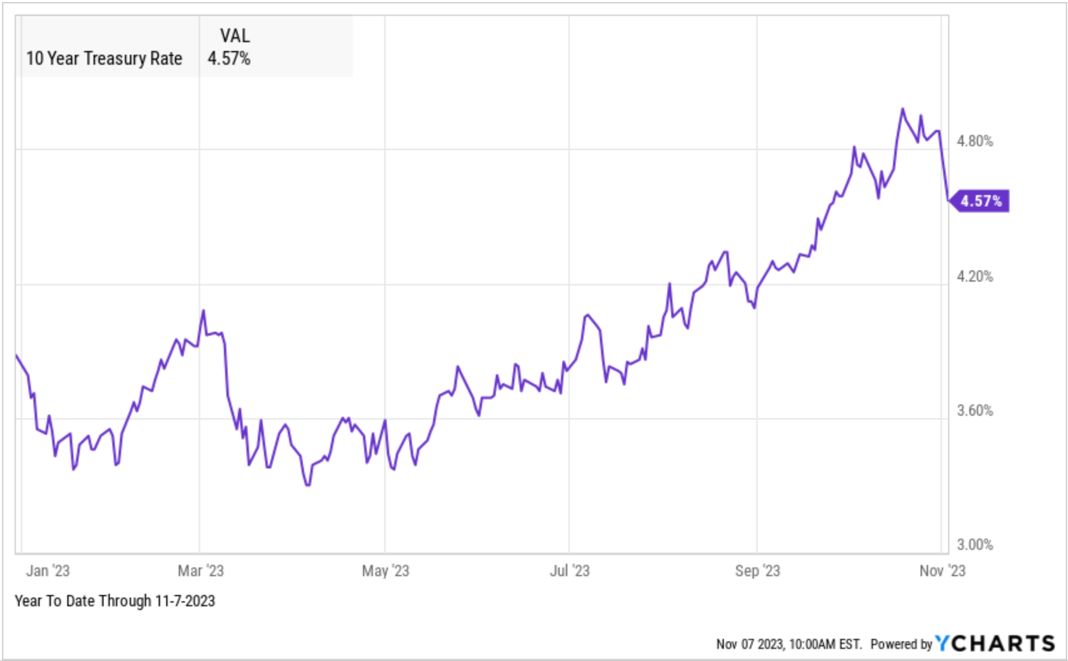

Following is a chart of the 10-year Treasury yield. The 10-year bond briefly touched 5% before falling to current yield of 4.57% due to the Federal Reserve’s comments after their meeting as well as the November unemployment report, signaling slower growth in hiring.

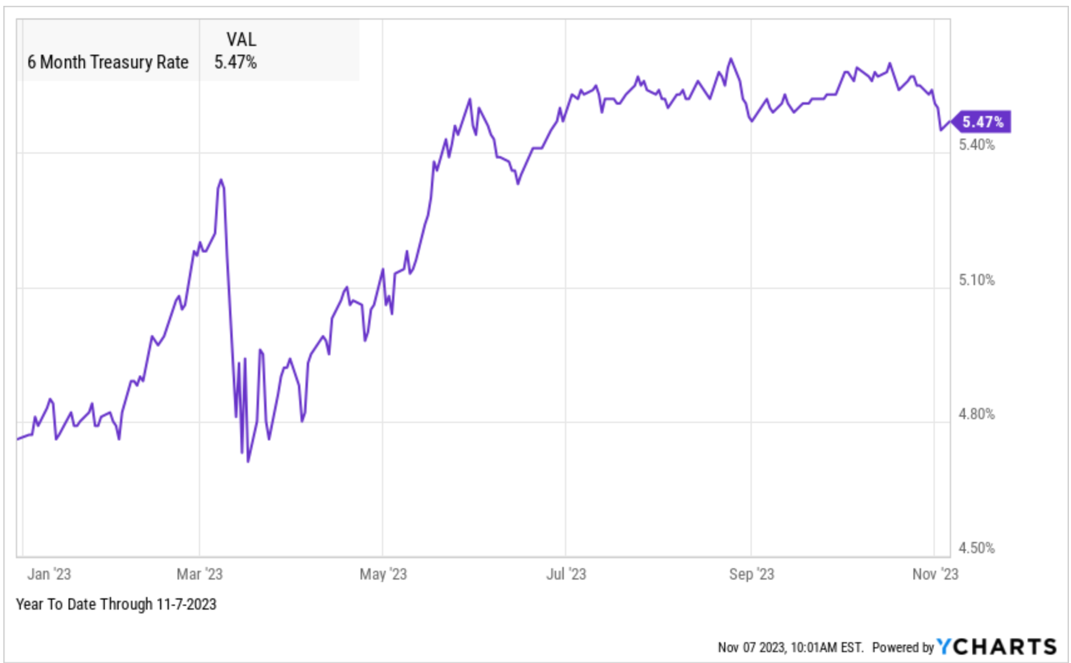

Short-term rates, as indicated by the 6-month T-Bill’s chart below, shows less of a decline in interest rates. The 6-month yield rose to a high of 5.61% on August 25th, and is currently at 5.47%.

Stocks largely ignored the statement as it met widely held expectations. Turning to the press conference, for all the back-and-forth, if one reads between the lines, Powell clearly conveyed that while additional rate hikes are possible, the bar for additional hikes is high, and as such, additional rate hikes are unlikely. He conveyed that message via two direct means: first, he stated rates are restrictive already (meaning they can stay here and slow the economy), and, second, he called inflation risks more two-sided. The market keyed on Powell’s commentary to rally into the close as investors embrace the reality that, barring a surprise jump in economic activity or inflation, the rate hike cycle is done.

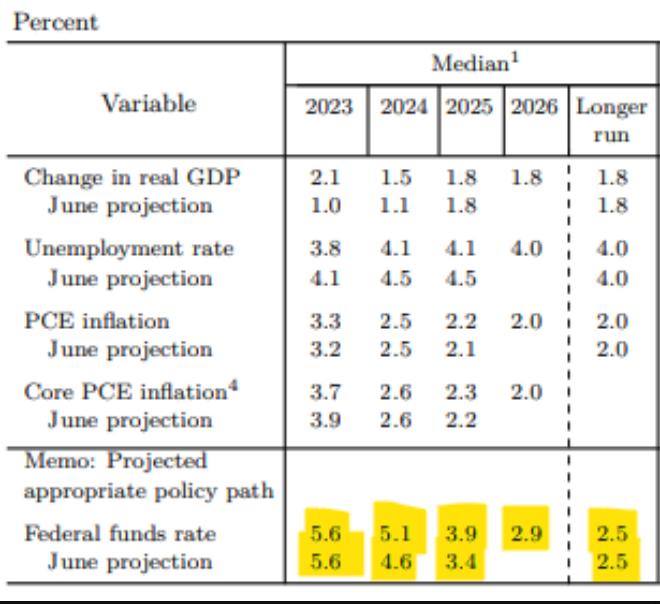

Each quarter, the Federal Reserve releases their summary of economic projections, which essentially is their best guess on future growth of the economy and employment as well as where they think interest rates will be in 2024 and over the next several years.

Part of the surprise in the Fed’s summary was an upward revision of expected economic growth through 2025 (2.1% in 2023, double its 1% estimate in June) while revising down the projected unemployment rate (3.8%, down from 4.1% estimate in June). At the bottom of the summary above, you will see the latest projection for interest rates at the end of 2024 is 5.1, up from 4.6 in June. The projection for the end of 2025 was also raised by 50 basis points (1/2%), from 3.4 to 3.9, as economic conditions are expected to remain strong. In addition, the Federal Reserve members now expect one more rate hike this year followed by two 25-point cuts in 2024. In June, the Federal Reserve’s projections were for 4 interest rate cuts—another factor contributing to keeping interest rates higher for longer with the potential for fewer rate cuts in 2024.

At the same time, though, the central bankers are projecting interest rates to stay above 5% throughout next year, though with a slight 50-basis-point cut. They’re also predicting around a 4% fed-funds rate in 2025, half a percentage point higher than the projection three months ago.

As has been the case all year, economic and inflation data remains the key. The Federal Reserve will be monitoring the economic data going forward to help determine if another increase in interest rates is necessary.

How does this affect our current strategy at Live Oak? It doesn’t. It only reinforces the strategy we have implemented since 2022: Higher rates for longer, potentially, and our three-pronged strategy.

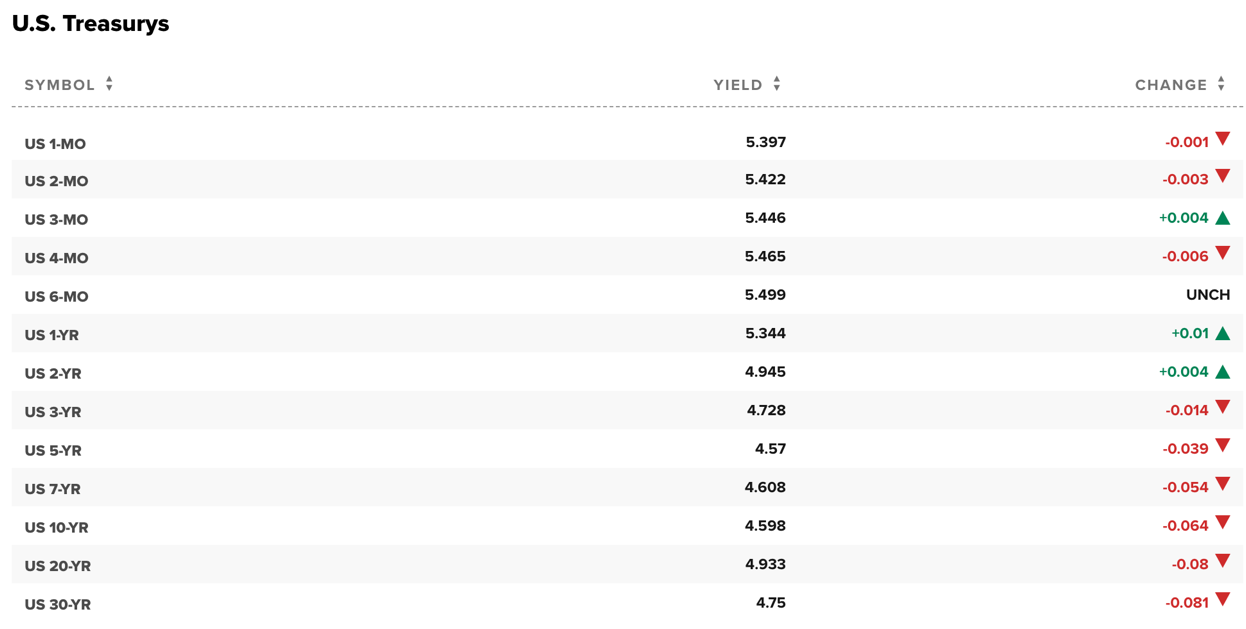

- The first part of our strategy has been buying 3-month, 4-month, and 6-month T-Bills. The following rates are from CNBC.com on 11/7/23. We are now able to earn between 5.446% to 5.499% annualized. Our strategy has been, when T-Bills are redeemed, we have been able to reinvest at the same to higher rates than before. If interest rates do stay higher for longer, this strategy will continue to be very beneficial.

2. Intermediate-term (12 month) bonds. Since 2022, we have been purchasing high-quality bonds from banks such as JPMorgan, Wells Fargo, Bank of America, Citigroup, and Royal Bank of Canada. When we first started buying bonds toward the end of 2022, we were receiving 4.50% on a Royal Bank of Canada bond that will be maturing on 11/20/2023. Now the most recent JPMorgan bond is being issued at 5.70% for the next 12 months. As these bonds mature at lower rates starting in November, we will be able to reinvest at higher rates over the next 12 months.

3. The third part of our 3-pronged strategy has been our Leader High Quality Income Fund, which is currently paying 7.17%, an increase from 7.11% and our Allspring Short-Term High Income fund paying 7.62%, an increase from 6.91%. The Leader High Quality Income Fund benefits as interest rates have risen. As a result, effective August 1, 2023, Leader High Quality Income increased their dividend from 6.5% to 7.17%.

A fourth area is preferred stocks. There continue to be great opportunities in preferred stocks that have been beaten up due to rising interest rates. We continue to find bargains yielding between 6.5%-9%+.

I will add that we have mostly been focusing on purchasing shorter-duration (3-6 months) when purchasing T-Bills. Due to the softening of the economy in several key areas, as well as tightening financial conditions, we will be extending our purchases to slightly longer-term, potentially up to 2 years. We are also seeing interest rates on fixed products such as fixed annuities and multi-year guaranteed annuities in the 5.95% to 6.15% range for 3-5 years.

Are you interested in setting up a review? If so, you can simply click here to schedule an appointment online.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insights and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.