The Federal Reserve doesn’t want to crash the economy…

That was Chairman Jerome Powell’s last message prior to the December 13th & 14th monetary policy meeting. He made the statement a couple of weeks ago as part of a presentation at American research group The Brookings Institution. He was speaking about how the U.S. central bank is using monetary policy to subdue inflation growth and restore price stability.

At the time, the central bank chief recognized that inflation pressures are starting to ease. Powell noted that core goods prices have dropped from “very high levels” earlier this year and housing inflation has been declining since this summer. This marked the first time he had made such a comment since mid-2021.

The development drove Powell to say the rate-setting Federal Open Market Committee (FOMC) now feels it’s time to start dialing back the pace of interest-rate hikes. It was an especially striking comment because of the timing. The implication is the central bank will only raise the federal-funds target by 50 basis points instead of the 75 basis points like at its last four meetings.

Chairman Jerome Powell said the central bank is raising the benchmark federal-funds target by 50 basis points, from a range of 3.75% to 4% to a new one of 4.25% to 4.50%. In other words, every home, car, and credit card loan just got more expensive.

In typical central-bank fashion, Powell reiterated its commitment to bringing down inflation to the sustained 2% target. As a result, Powell said the rate-setting Federal Open Market Committee (FOMC) expects to keep raising interest rates next year.

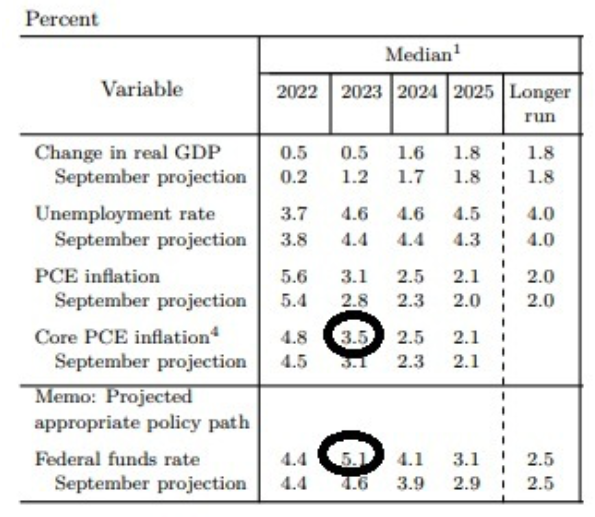

Let’s take a look at how the Fed sees next year according to their projections:

Source: https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20221214.htm

For 2023, according to the economic projections above, the Fed sees very little economic growth (which would be a second consecutive year). They see their favored gauge of inflation coming down to 3.5%. And yet they see rates up another three-quarters of a percentage point—at over 5%. That’s an illogical formula. With that, the 10-year Treasury yield went down (on this news), not up.

What does it mean? The market is not buying what the Fed is selling.

The benchmark interest rate (widely viewed as the “smart money”) is now trading 1.50% below where the Fed is projecting to take short-term rates next year.

So, who’s smarter: The Fed or the interest rate market? Well, we know that the Fed’s projections have a history of being very wrong (AND their projections can, and do, change, with no apologies).

So, the question now becomes one of the havoc the central bank is wreaking on the economy. After all, policymakers like Vice Chair Lael Brainard and Federal Bank of San Francisco President Mary Daly have said it takes at least six to eight months before monetary policy changes start to show up in the economic data.

If we follow that thinking, the economic fallout we’re seeing currently is based on the 75 basis points of rate hikes made in March and May. The 350 basis points’ worth of additional increases has yet to even be felt.

Fed policy-makers are entering a new phase of policy tightening in which they are trying to determine just how high to raise rates. Fed Chair Jerome Powell said in a news conference it was “broadly right” that slowing rate rises to more traditional quarter-percentage-point increments as soon as the Fed’s next meeting (Jan. 31-Feb. 1) would provide the best way to manage the risk of overtightening.

With all the above in mind, the Fed set the following expectations in September. The Fed continues to err on the side of overtightening, and they want us to know it:

1) They have more “ground to cover” on rates.

2) They think they will get to a higher level on the Fed funds rate now than they forecast just two months ago, now at 5.1% vs. 4.6% in September.

3) Powell made an effort to include in his “off-script” Q&A session that he thinks “it’s very premature to think about pausing (on rate hikes).” Emphasis on very.

4) And he says they are committed to bringing inflation down (erring on the side of overtightening).

It looks like inflation is finally cresting now that the Fed has gotten serious about fighting it. This is similar to what we saw back in 1947, when the central bank’s actions cooled inflation by more than two-thirds in a matter of months. It’s also similar to what former Fed Chairman Paul Volcker managed in the 1980s; he raised interest rates as high as 20% until inflation was back under control.

Today’s interest-rate hikes are working. We’re no longer staring down a decade of high inflation and weak economic growth, like we saw in the dreaded 1970s. That is certainly a silver lining. Most people are dreading a repeat of 2008—folks losing their homes, mass layoffs, a stock market crash, and credit markets shutting down.

That’s not what we expect from this potential recession at all. The reality is that consumer credit is remarkably healthy today. Delinquency rates are below 2%—the lowest they’ve been since before the Great Recession. Similarly, corporations look like they’ll be able to manage a credit contraction. They have a good amount of cash on hand. In other words, companies may need to tighten their purse strings in the next year or two.

Heading into the 2008 recession, consumers were in a much worse position. And corporations and banks were stretching their balance sheets to the brink. That’s why the recession was so deep…and why the stock market crashed so hard.

Consumers and corporations are far healthier heading into whatever recession is in the works today…. We believe a more realistic scenario is a mild recession that looks like what we saw from 1948 to 1949. Similar to back then, extreme demand is driving inflation…the Fed is trying to slow that demand down…and balance sheets remain pretty healthy heading into tough times.

Said another way, this downturn is more about the Fed trying to slow spending and lessen demand than it is about borrowers behaving badly.

As mentioned previously, the bond market and the Federal Reserve are currently at odds. The bond market is forecasting that the Federal Reserve will need to cut rates sometime in the second half of 2023 and stop raising rates soon based on current weakness in many areas of the economy. Conversely, the Fed sent a message on December 14th that they were quite willing to maintain a chokehold on the economy.

With the same hubris that they committed to the “inflation is transitory” messaging of last year, which inflated asset bubbles, they are now doing in reverse.

We know that the Fed’s projections have a history of being very wrong (AND their projections can, and do, change, with no apologies). The examples of how wrong they can be are not hard to uncover: After finally acknowledging the level and persistence of inflation late last year, at the December Fed meeting one year ago, they projected that the Fed funds rate would go to less than 1% in 2022. It’s now 4.4%. (1) And at the December Fed meeting one year ago, they projected that the Fed funds rate would go to just 1.6% in 2023. Now they project 5.1%. (2)

In our opinion, the Fed has gone too far already. The 10-year yield is telling us the lag effect from the Fed action hasn’t hit just yet. But it’s coming. When you take the Fed funds rate from zero to 3.75% in eight months, and spike mortgage rates from 2.75% to near 8% that quickly, you’re going to get damage, and a retrenchment in economic activity—and maybe even deflation.

The Federal Reserve seems committed to continue raising interest rates and potentially keeping interest rates at a high level to combat inflation. Here’s Reuters quoting Federal Reserve Bank of Cleveland President Loretta Mester:

(Mester) said on Friday that she believes the U.S. central bank will have to raise interest rates higher than the level most policy makers cited in their Fed forecasts this week.

Against the Fed’s projection that the current federal funds rate of between 4.25% and 4.5% will rise to 5.1% next year, Mester said, “I’m a little higher than the median”…“We need to continue to bring up interest rates into a restrictive stance,” Mester said. “We did a lot of work this year” moving rates up aggressively, she said, adding once the Fed finishes raising rates, it will need to hold them there for “quite a while in order to get inflation on a sustainable downward path.”

Finally, there was Federal Reserve Bank of San Francisco President Mary Daly going full-Scrooge on bulls looking for a quick return to rate-cutting in 2023.

From Reuters:

(Daly) said it’s “reasonable” to think that once the Fed policy rate gets to its peak, it will stay there for nearly a year, and added she’s prepared to keep it there longer if needed.

“Everybody has rates holding for ’23,” Daly said in a virtual event…

“I think 11 months is a starting point, is a reasonable starting point. But I’m prepared to do more if more is required,” she said, adding that it will be the data that determines exactly how long the Fed will keep rates restrictive.

Consumer prices rose last month at the slowest 12-month pace since December 2021, closing out a year in which inflation hit the highest level in four decades and challenged the Federal Reserve’s ability to keep the U.S. economy on track. (3)

The Labor Department said that its consumer-price index, a measurement of what consumers pay for goods and services, climbed 7.1% in November from a year ago, down sharply from 7.7% in October. The pace built on a trend of moderating price increases since June’s 9.1% peak, but it remained well above the 2.1% average rate in the three years before the pandemic. (4)

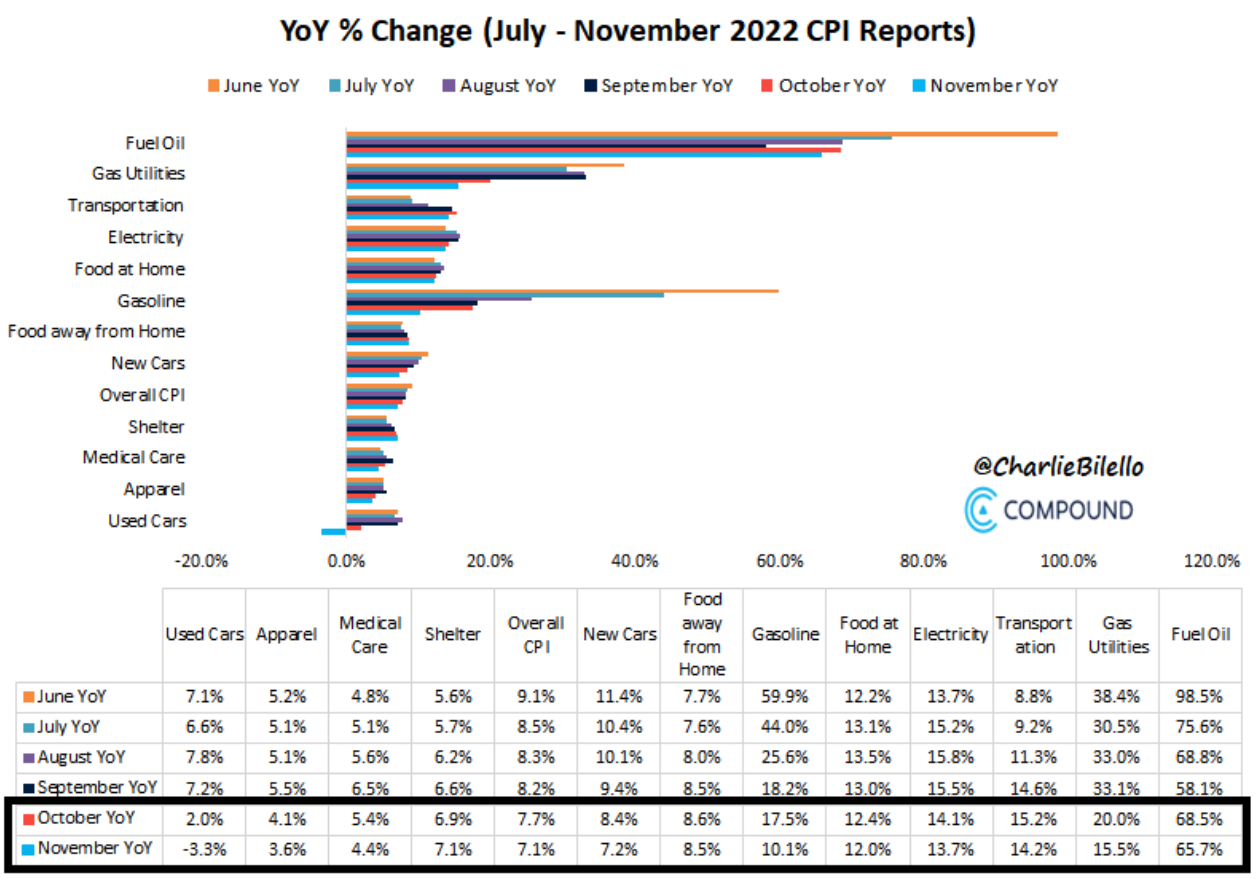

With the exception of Shelter (which is lagging the real-time decline in rents & home prices), all of the major CPI components showed a lower YoY % increase in November than October.

Source: https://www.bls.gov/news.release/cpi.nr0.htm

Prices also softened significantly on a month-to-month basis, with gasoline, utility, medical care services. and used-car prices all falling. Price increases moderated for restaurant meals, while prices for new vehicles remained flat.

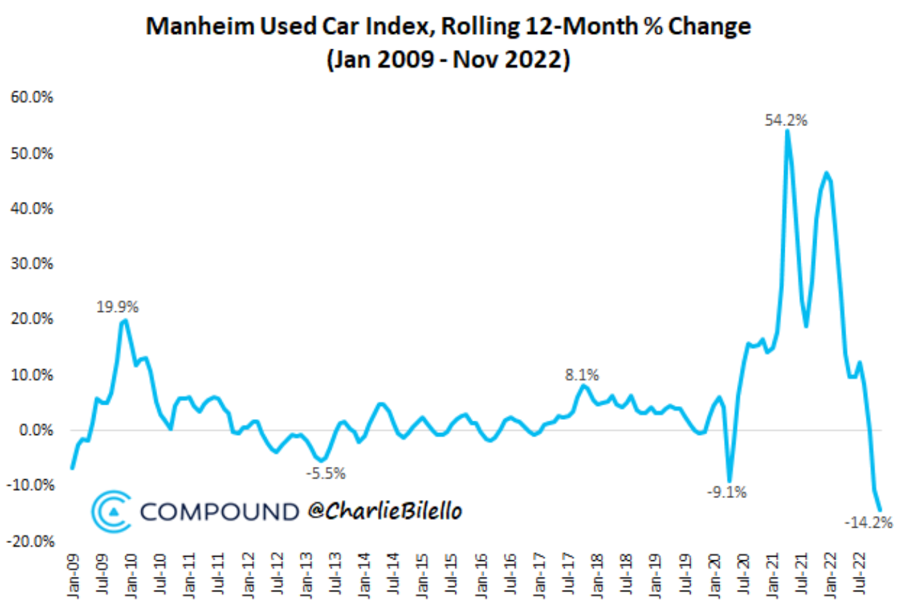

Used-car prices—a big driver of inflation last year—fell for the fifth straight month, slipping in November to their lowest level since September 2021. The Manheim Used Car Index is now down 14% over the past year, the largest YoY decline on record with data going back to 2009. This was a leading indicator of higher inflation rates in 2020, and the recent downturn is likely a leading indicator of lower inflation rates to come. (5)

Many travel-related prices declined in November as well, with airline fares down 3% from October, and car and truck rental prices dropping 2.4%.

However, grocery prices picked up 0.5% in November from the prior month, accelerating slightly from October’s pace, buoyed by increases in prices for bakery products and fruit and vegetables. (6)

Another big positive on the inflation front that hopefully continues: fertilizer prices peaked in late March and are down 39% since, now at the lowest prices since September 2021. This is great news given their high correlation to food prices.

Source: https://compoundadvisors.com/wp-content/uploads/2022/12/image-24.png?ck_subscriber_id=1279763785

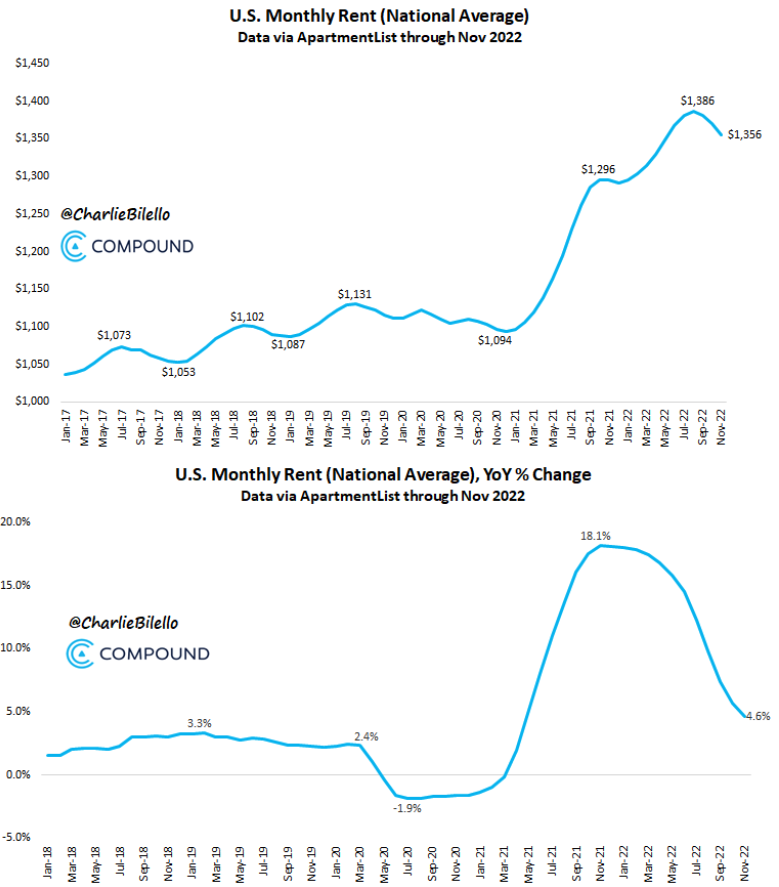

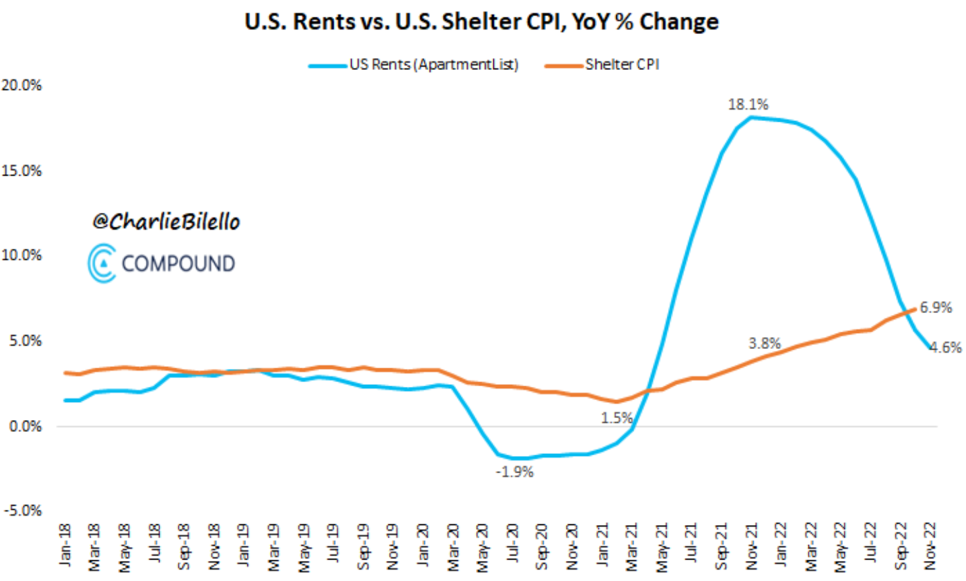

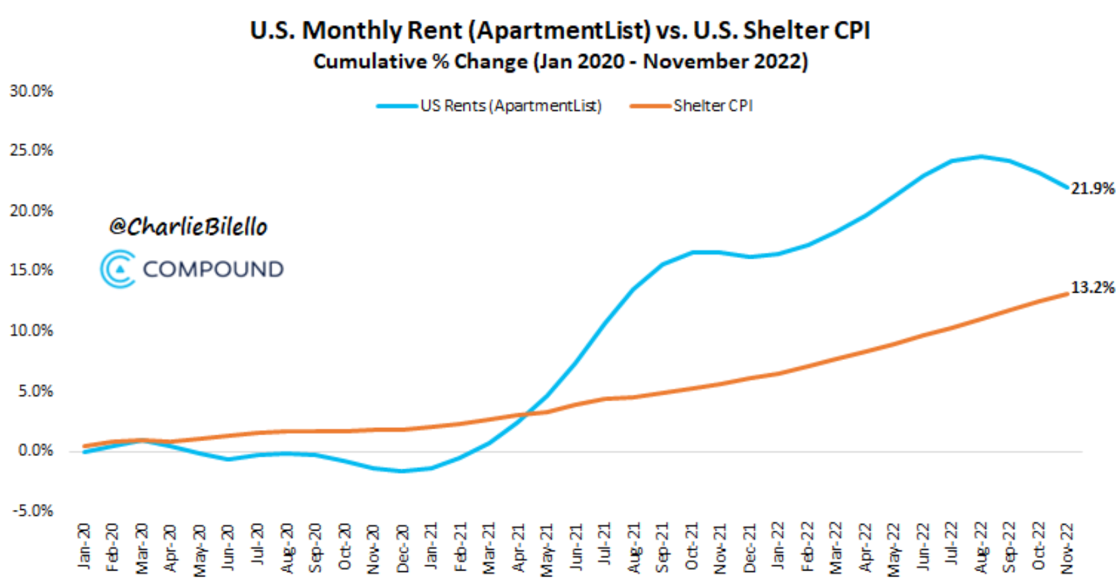

U.S. rents fell 1% in November, the third straight monthly decline. The year-over-year percentage increase has now moved down for 12 consecutive months after peaking at 18.1% last November. At 4.6%, this is the smallest YoY increase since April 2021.

This 4.6% YoY increase is now below the 6.9% increase in the shelter component of CPI. Why is shelter CPI still moving higher while actual rents are moving lower? Shelter CPI is a lagging indicator and has significantly understated actual housing inflation over the last two years.

Shelter is still playing catch-up as it had been wildly understating the actual increases in housing costs. That gap remains but is narrowing fast as rents are now falling, while shelter CPI continues to move higher.

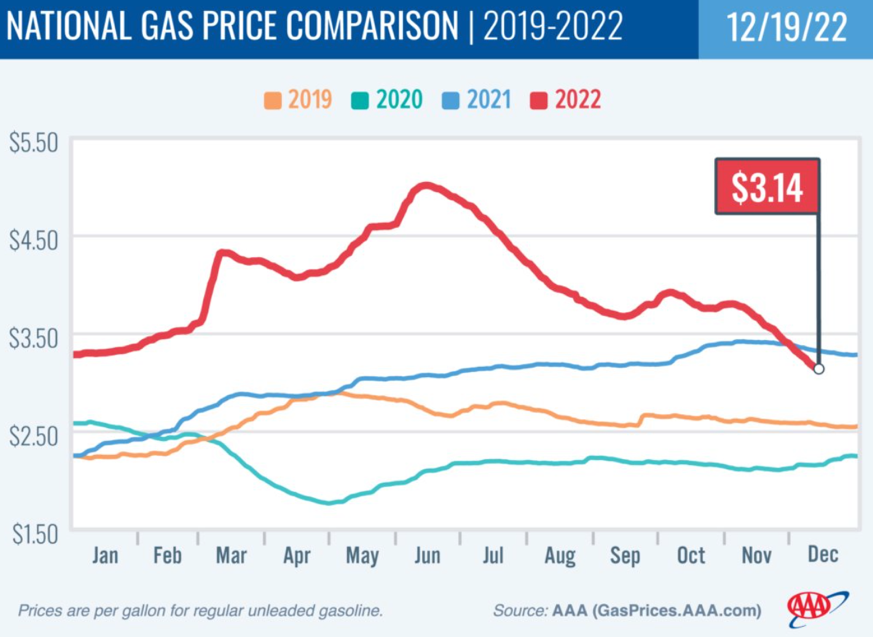

Finally, another positive is gas prices in the U.S. have moved down to $3.14/gallon (national average), 37% below their all-time high in mid-June, and 16 cents below year-ago levels.

We know from real-time CPI inputs (like new and used cars, rents) that prices have been rolling over for months. The government’s report hasn’t reflected it…yet.

We’ve seen the damage in the global financial system, with a near blowup in UK and European sovereign debt over the past several months. We’ve seen some retrenchment in the economy (U.S. and global manufacturing back in contractionary territory).

We haven’t seen falling prices yet in the stale government inflation data. But we may see it finally showing up early next year. Again, the 10-year yield may be giving us that message.

What Does This Mean for the Stock Market?

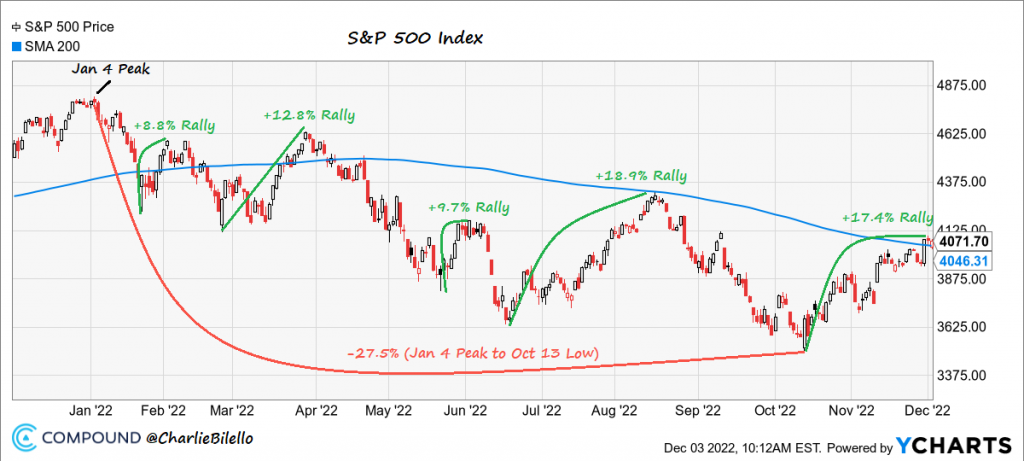

The equity market has been climbing this wall of worry, with a 17% rally off of the October lows. That has been the challenge this year. As you can see from the chart, we experienced bear market rallies of 8.8%, 12.8%, 9.7%, and 18.9% only to see the S&P 500 turn around and make new lows. On this most recent rally, will it be different this time where we will see the S&P 500 stabilize and build on this rally for still higher markets?

|

We are using this pullback as a buying opportunity with a risk management approach. In summary, we think the market is “bottoming” out. And our objective is for a rally to the 4300+ region. The only question is if the bottom has already been struck, or if we get that one more lower low to the 3800-3767 level on the S&P 500. And, in truth, due to how oversold many stocks still remain, it would not shock me to see the next rally extend to the 4500/4600 region, with new all-time highs still remaining well within my sights.

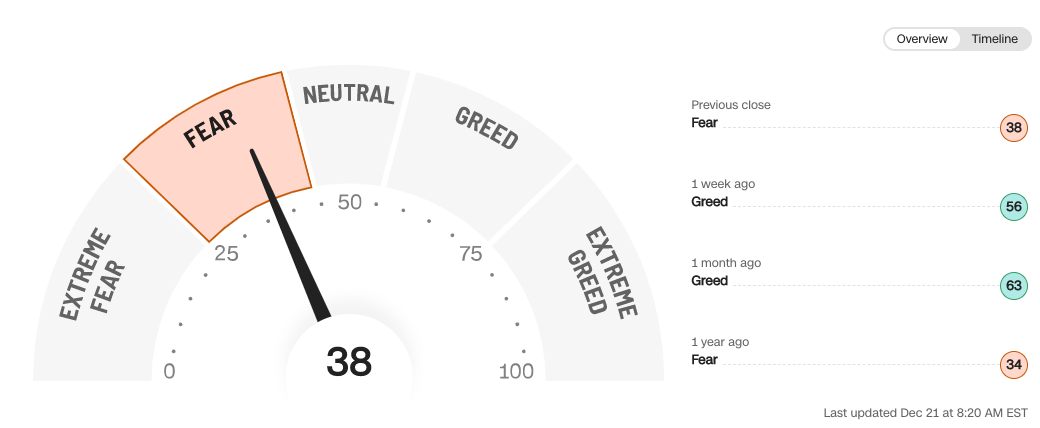

Now, I know many are starting to get very bearish once again, and believe that lower lows below that struck on October 13 are coming with this current decline. While that is certainly “possible,” I would say that if our setup develops as outlined above, it will not be the “probable” outcome. We can see this on the CNN Fear and Greed Index with a current reading of 38 in the Fear category.

Source: https://www.cnn.com/markets/fear-and-greed

There’s no denying that it’s a scary time to be an investor. Doom-and-gloom headlines from the mainstream financial media aren’t making things any better. That being said, it’s also an exciting time…if you know where to look.

2022 has been a VERY challenging year in many areas of the investment markets. So the question now is where are the opportunities to take advantage of in 2023? We will be issuing our Bear Market Recovery Strategy in the new year. We will provide our analysis and thoughts on 2023 as well as where the greatest opportunities are to be positioned for next year.

We understand the risks facing both the markets and the economy, and we are committed to helping you effectively navigate this challenging investment environment. Successful investing is a marathon, not a sprint, and even extended bouts of volatility like we’ve experienced over the past year are unlikely to alter a diversified approach set up to meet your long-term investment goals.

Therefore, it’s critical that we have your financial plan up to date as we’ve worked with you to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.

Rest assured that our entire team will remain dedicated to helping you successfully navigate this market environment.

Happy Holidays, Merry Christmas, and Happy New Year!

If you would like to schedule a call/web meeting/in-person meeting, please click here to access our calendar.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.

___________________

(1) https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20211215.pdf

(2) https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20221214.htm

(4) https://www.wsj.com/articles/us-inflation-november-2022-consumer-price-index-11670883405

(5) https://publish.manheim.com/en/services/consulting/used-vehicle-value-index.html