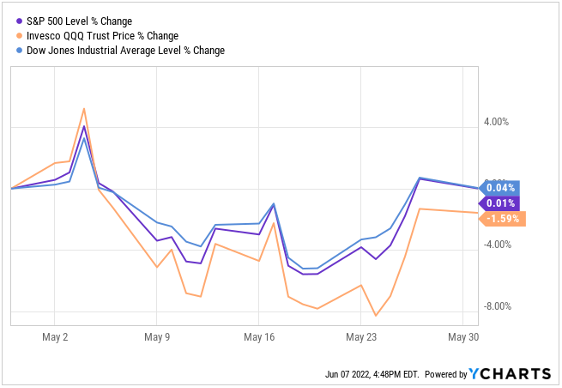

May continued to be a volatile month for the stock market. As you can see in the chart below, the Dow Jones Industrial Average and the S&P 500 were virtually flat while the Nasdaq finished down -1.59% for May.

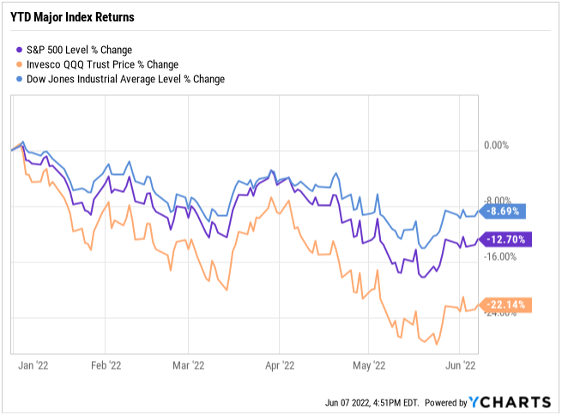

On a year-to-date basis, the major indices are still negative, as you can see in the following chart.

May certainly provided more bad news with volatile market reactions. On May 17th & May 18th, retail giants Walmart (WMT) and Target (TGT) reported earnings suggesting tougher times ahead, with Target CEO Brian Cornell saying the company estimates $1 billion more in fuel costs than it did at the start of the year, stemming from record-high gas prices. Brian Cornell also mentioned, “We never expected the kind of cost increases in freight and transportation that we’re seeing right now.”

Cornell also said consumer behavior was changing… to focus on more staple items instead of big-ticket discretionary purchases. Walmart executives talked about similar issues. After their most recent earnings calls, shares of Walmart and Target fell by 25% and 17%, respectively. (1)

China is reopening and hopefully, the economy will be close to operating at near-full capacity within a month. That will add a large tailwind to the global economy, and perhaps most importantly, ease supply chain stress (which will help pressure inflation).

The Federal Reserve and Their Quest to Raise Interest Rates (and Push the US Economy into a Recession)?

The Federal Reserve is on a mission to bring down inflation, which rose to an annual rate of 8.5% for the 12 months ended March – the highest level in 40 years. Its plan to do this is by raising short-term interest rates as much as necessary to slow the economy down and hopefully prevent further price increases.

Through policy statements and speeches by Chairman Jerome Powell, the Fed has made it clear it is prepared to raise the Fed Funds rate at each of the remaining Fed Open Market Committee (FOMC) meetings this year, if necessary. The Fed has suggested it could raise the key short-term rate by as much as 0.5% (50 basis points) at each of the next two upcoming meetings, which will occur on June 14-15 and July 26-27, and perhaps thereafter if needed. And it has suggested there could be more rate hikes in 2023 if necessary.

That’s a sizeable jump in borrowing costs. The change means households and businesses carrying debt loads will have to spend more money servicing them as credit-card rates increase and the cost to refinance corporate bonds rises. In other words, there will be less discretionary money to be spent on other items going forward, which undermines economic demand.

Federal Reserve board members and regional bank presidents are sending a similar message. Vice-Chair Lael Brainard recently said she doesn’t see a good case for pausing the rate-hike cycle at the September meeting of the policy-setting Federal Open Market Committee. Board member Christopher Waller endorsed another 0.5% increase in September while speaking earlier this week. And Cleveland President Loretta Mester said rates must rise quickly.

So, let me make sure you understand the current situation. Last year, these were all the same people that were saying inflation was “transitory,” or temporary and that the supply chain would right itself and in turn, prices would come down. In the meantime, the Federal Reserve continued to purchase $80 billion of Treasuries and $40 billion of mortgage-backed securities, thus fanning the flames of inflation. Now, at the start of this year, the Federal Reserve members and Chairman Jay Powell started talking tough about raising interest rates to try and bring down inflation, admitting they were wrong about inflation not being a big deal last year. So you can understand why I don’t have much confidence in the Federal Reserve to bring down inflation to a manageable level without causing a recession and some unintended consequences.

Board member Christopher Waller said the central bank is concerned by the shift in job openings compared to individuals seeking work. He stated that prior to the pandemic, there was one job opening for every two unemployed people. But now, there are two openings for every person looking for employment.

This is leading to wage inflation, as employers have to raise salaries for new hires as well as current employees. And that’s driving higher prices since businesses are charging more for their goods and services to cover costs and maintain profits.

Waller stated that despite the recent pullback in inflation, the numbers remain “alarmingly high.” He feels the metrics aren’t coming down enough to meet the central bank’s 2% target any time soon. As a result, Waller said the Fed must aggressively raise interest rates to bring the labor supply-versus-demand picture back into balance and ease inflation.

Policymakers gave their forecast for neutral in March. Currently, the expectation is 2.4%, but that could change at the June policy meeting. Waller is saying interest rates need to be at least 2.75% to start bringing inflation back down. Considering the federal-funds target range is 0.75% to 1% currently, that means another 1.75% worth of rate hikes before the year’s end.

The Federal Open Market Committee only has five meetings left this year, taking place in June, July, September, November, and December. Chairman Jerome Powell is already guiding for 0.5% increases in June and July. Waller is now suggesting September as well. That would leave November and December to raise rates by at least another 0.25%, at a minimum.

However, the official minutes from the Fed’s latest policy meeting on May 3-4 were released on May 25, and those minutes suggested the Fed is not committed to 50 basis-point rate hikes at every meeting this year.

More specifically, those minutes indicated that while a 50 basis-point increase is all but assured at the next two FOMC policy meetings, it was also clear the Fed will be open to smaller rate increases at subsequent meetings this year. In essence, the Fed will hike by 50 basis points at the next two meetings and then reassess based on the outlook for inflation at that time.

The Power of the Federal Reserve Chairman

In a March 2015 blog post from former Federal Reserve Chairman Ben Bernanke, Ben wrote “When I was at the Federal Reserve, I occasionally observed that monetary policy is 98 percent talk and only two percent action. The ability to shape market expectations of future policy through public statements is one of the most powerful tools the Fed has.” (2)

The Fed has explicitly targeted jobs, in the effort to bring down inflation. The Fed Chair, Jay Powell, told us explicitly that they intend to bring the ratio of job openings/job seekers down from two-to-one, to one-to-one. Yes, we have a Fed that is trying to manipulate to the goal of higher unemployment.

In my 20-year career in markets, I’ve never witnessed a Fed that is explicitly attempting to destroy demand and jobs. But here we are. With that, we are in a bad news is good news stock market. The more verbal influence that the Fed can have on markets, and consumer and business psychology, the less work that the Fed has to do with interest rates.

The shallower the path of interest rate hikes, the higher the probability of a soft landing for the economy. That’s a slowing growth scenario (the best-case scenario in this environment).

On that front, so far so good. The markets are doing the Fed’s job for it. Lower equity valuations, higher gas prices, and higher mortgage rates have quickly changed consumer business psychology. Demand is coming down, which should translate into some loosening in the job market.

This was all within the context of what the Fed described in their May meeting notes as a “very strong economy,” “extremely tight labor market,” and “very high inflation.” Financial conditions have tightened.

And with that, consumer psychology is changing. So, this brings me to the power of the Fed’s tough talk. In March, Jay Powell explicitly said they were trying to better align demand with supply (i.e. bring demand down).

Within that strategy, they have explicitly said they want to narrow the job opening to job seeker gap (which has been 2 to 1).

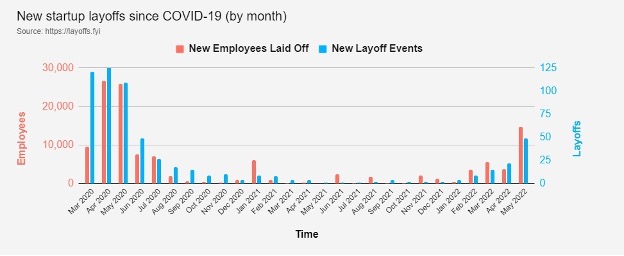

As a proxy, this chart of layoffs in startups are happening (narrowing the gap):

So, just months after telling us they want to bring demand down, the switch seems to have been flipped (per the charts above).

And they haven’t even gotten the effective Fed funds rate to 1% yet. And they haven’t even started their Quantitative Tightening program.

But they have achieved the goal of knocking down animal spirits, curtailing inflation expectations, and extracting liquidity from the system (in the form of lower equity market valuation). If we consider that, we have a Fed that should have the comfort to sit back and watch the inflation data come down.

This is a slow-down scenario. And it has been quick. And it presents the very real possibility that the tightening effect from a stock market decline, high gas prices, and an adjustment in mortgage rates, could be enough to bring inflation under control (without requiring sharply higher interest rates).

It’s the “negative net worth effect” of stocks, and the “cost of living tax” from gas and mortgage rates, that have resulted in a “tightening” effect on the economy.

Bottom line: Markets have seemingly done the Fed’s job for them. Without having to move past 1% on the effective Fed Funds rate (to this point) or sell a single bond from their balance sheet, they’ve gotten the desired result. Slowing demand.

Energy Prices Continue Higher

As we head into summer, let’s talk about oil.

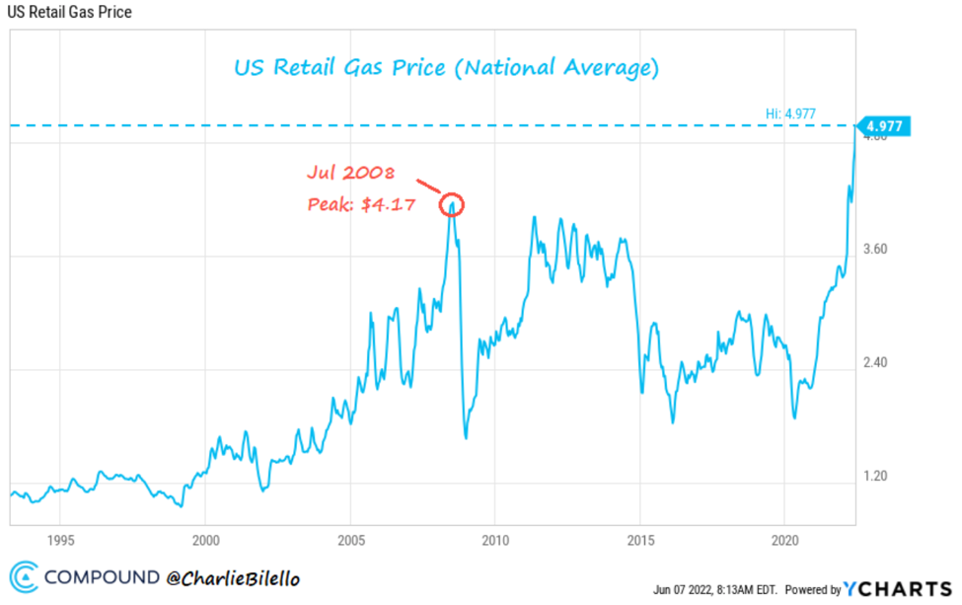

Two years ago (this time of year), the national average price of gas was $1.87. Last year: $3.04. Today, it’s $4.97. Throughout much of the past two years, the “climate actioners” were convinced that oil demand was rapidly eroding, on the fantasy of a rapid change to a world of ubiquitous electric vehicles and wind farms. So, they underestimated demand, while simultaneously regulating away (oil) supply.

The result has been ceding control on oil prices, completely, to OPEC. And that guarantees higher and higher prices (no limit). With that, as we’ve discussed in recent weeks, the energy price input on the cost of living has become a primary headwind for demand.

Gas prices in the US hit another record high, rising to an average of $4.98 per gallon. A year ago the average price was $3.13 and two years ago the average price was $2.06. Today, 14 states are averaging $5 per gallon or more. The cheapest state average is $4.33 in Georgia. Contrary to the Biden administration’s claim, the release of 180 million barrels of oil from the Strategic Petroleum Reserve is not working as oil and gas prices continue to go higher. As long as there is more demand than supply, the increased supply is only a drop in the bucket to fill the supply gap from the Russian oil embargo.

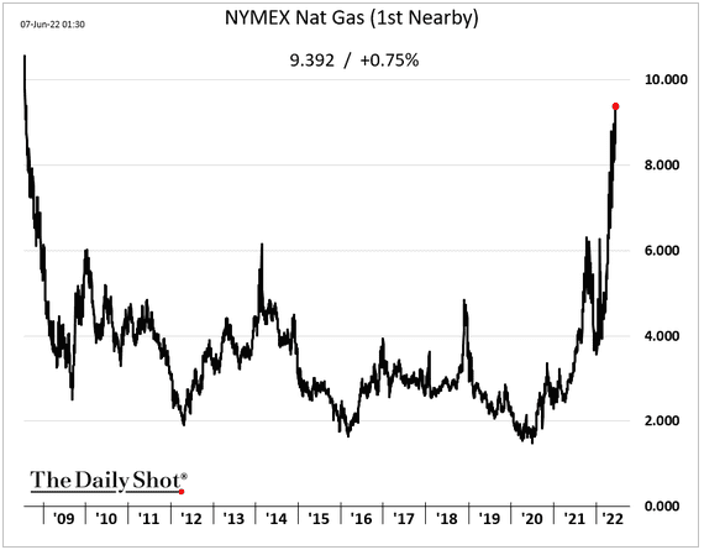

A market you may not hear much about is natural gas. Due to higher temperatures around the country, we have seen the price of natural gas approach $10.00 m/btu, the highest price since 2009, which also means we will be paying more to cool our houses this summer. Unfortunately, it looks like we are not going to get any relief for lower energy costs for the near and intermediate-term.

JPMorgan Chase CEO Jamie Dimon says he is preparing the biggest U.S. bank for an economic hurricane on the horizon.

During a financial conference on June 1st, Jamie Dimon said “You know, I said there’s storm clouds but I’m going to change it … it’s a hurricane. While conditions seem “fine” at the moment, nobody knows if the hurricane is “a minor one or Superstorm Sandy,” he added.

There are two main factors that has Dimon worried: First, the Federal Reserve has signaled it will reverse its emergency bond-buying programs and shrink its balance sheet. The so-called quantitative tightening, or QT, is scheduled to begin this month and will ramp up to $95 billion a month in reduced bond holdings.

“We’ve never had Quantitative Tightening like this, so you’re looking at something you could be writing history books on for 50 years,” Dimon said. Several aspects of quantitative easing programs “backfired,” including negative rates, which he called a “huge mistake.”

Central banks “don’t have a choice because there’s too much liquidity in the system,” Dimon said, referring to the tightening actions. “They have to remove some of the liquidity to stop the speculation, reduce home prices and stuff like that.”

The other large factor worrying Dimon is the Ukraine war and its impact on commodities, including food and fuel. Oil “almost has to go up in price” because of disruptions caused by the worst European conflict since World War II, potentially hitting $150 or $175 a barrel, Dimon said.

“Wars go bad, [they] go south in unintended consequences,” Dimon said. “We’re not taking the proper actions to protect Europe from what’s going to happen to oil in the short run.” 1

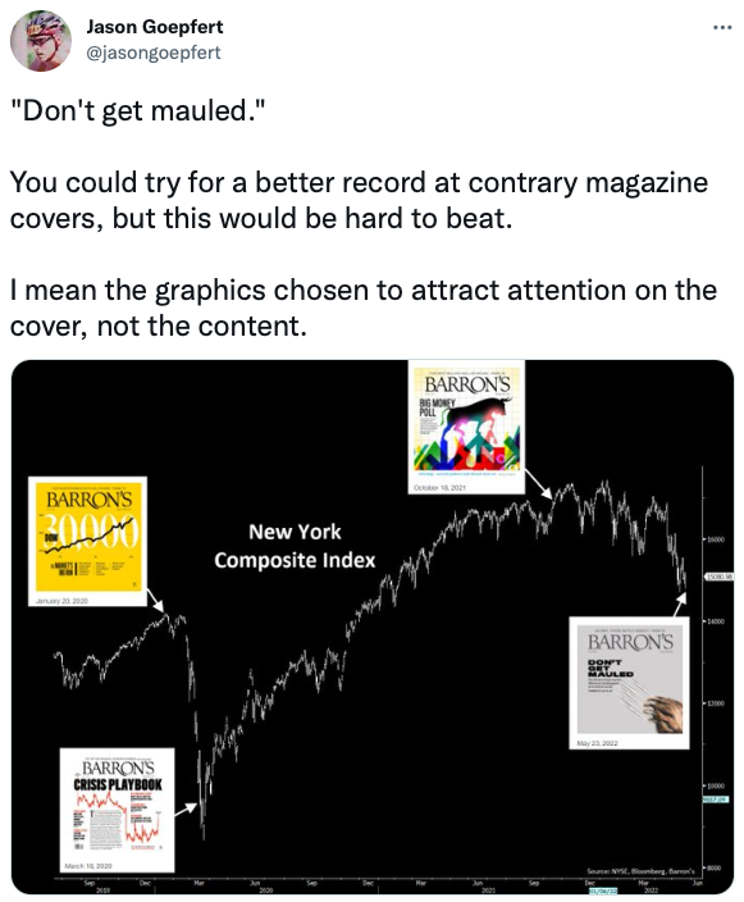

The media is generally a good contra-indicator for stocks

The more negative articles there are, the more likely it is that we’re at or near a bottom. So I view this as a positive sign – there were more articles on Friday May 20th that mentioned “bear market” than any day in the past decade other than one day during the COVID crash:

Here is another tweet from Jason Goepfert showing the number of bear market articles published on Friday May 20th:

Market Outlook & Strategy Update

Despite how emotional the bottom was in March of 2020, I remember getting a chuckle at when the economists declared us likely to be heading into recession just as we were striking the bottom. In fact, it took those brilliant economists until the market was 1500 points off its low to tell us that we were no longer in a recession.

And, it seems as though the market mavens have struck again. Just as they were proclaiming that the S&P 500 has dropped into “bear market territory,” if you listened closely, you would have heard the market gods laughing again as we have rallied approximately 9% off the 3810 low in the S&P 500.

For those that were with us during the 2015 correction, you may remember how the market action at that time caused many to become quite frustrated with the market due to the many months of grinding and downside action. And, we are clearly seeing the same feelings pervasive throughout the market today.

So, let’s try to move past the common views of frustration and that we are in a “bear market,” as it will certainly be making the rounds and will likely scare many to move out of the market. But, the real question is if we have finally hit a bottom to this correction? The answer is that the market has made significant strides, but there is still reason for caution. You see, we have had several “fake outs” over the last several months where we would see a strong rally, and then the market would turn around the next day and give up most if not all of the gains and go on to make new lows.

Another positive sign is that more of our market indicators are turning positive indicating that we may have seen the bottom. The market still needs to prove itself, and if we can continue to see the S&P 500 break through some resistance areas, this will go a long way to becoming more aggressive in making purchases as we still believe we will see new highs.

Before we began this correction, I was warning in late 2021 that the correction we expected in early 2022 was likely going to be the largest correction we have seen since we bottomed in March. Moreover, I also noted that the correction would not likely be over until the significant majority of the market was convinced that the bull market was over.

Now, I want to address those who believe we have begun the long-term bear market. I still do not see this as the most probable resolution to the current market posture. We are hitting bearish extremes that have not been seen since the March 2020 low, and there are some extremes that have not been seen for the last 20-30 years. In the significant majority of times, extremes such as these lead to new all-time highs in almost every instance recorded. All you have to do is refer to our previous section about the number of bearish articles being published.

In terms of investments, we still favor dividend-paying companies and high free cash flow companies that have the ability to raise prices in this environment. If US economic growth is slowing, this will favor growth stocks as well as technology companies. We continue to dollar cost average in these areas. We also believe we are close to a top in interest rates and that we should see a bond market rally (rates going lower and prices higher) that should take us towards the end of this year and possibly into Q1 2023. This will provide opportunities in areas of the bond market that have been beaten down due to the rapid rise in interest rates.

If you would like to schedule a call/web meeting/in-person meeting, please click here to access our calendar.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.

_________________

(2) https://www.brookings.edu/blog/ben-bernanke/2015/03/30/inaugurating-a-new-blog/