By Matthew Gaude & Shawn McGuire

There’s almost no good news today. The Fed is raising rates and starting quantitative tightening. Inflation is out of control. Gas prices are hitting American households hard. Former tech leaders have been taking it on the chin. This seems to have everyone now expecting a protracted bear market. And, to be honest, it will be the first bear market in history for which almost all market participants are now prepared. Everyone is hunkering down and preparing for the absolute worst.

But, is that how the market works?

Well, not usually. When everyone maintains the exact same expectation, that’s often when the market turns on everyone. We’ll discuss this in more detail later.

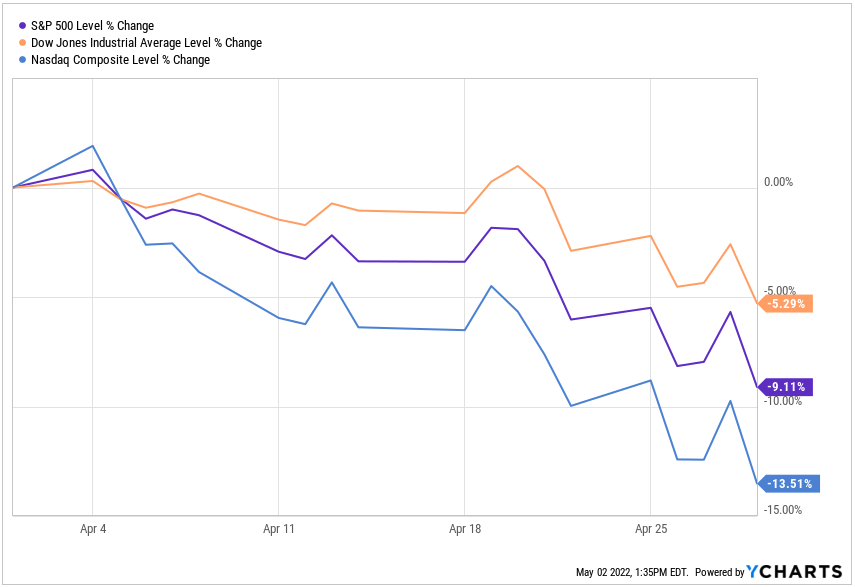

In the meantime, interest rates keep going up, inflation keeps going up and the stock market keeps going down. For the month of April, the S&P 500 was down -9.11%, the Dow Jones Industrial Average was down -5.29% while the Nasdaq was down -13.51% as you can see in the chart below.

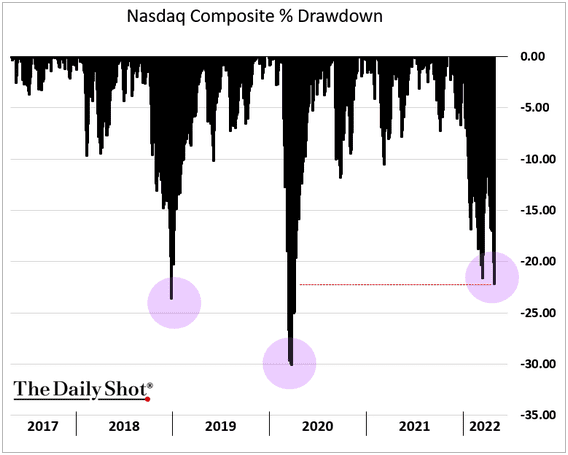

At -22%, the Nasdaq drawdown (from high to low) is comparable to the last two major drawdowns in December 2018 and March 2020.

3 Questions For the Selloff:

Why have stocks dropped to the March lows, what makes this stop, and how bad can it get? As shown above, the Nasdaq has seen its largest drawdown since March 2020 and December 2018. The S&P 500 is off to one of its worst starts in history. Given this steep decline in the stock market, I wanted to step back and clearly explain: 1) Why stocks have dropped so sharply this year, 2) What makes this stop and 3) How bad it could get.

1. Why Have Stocks Dropped to YTD Lows?

The S&P 500 declined 9.11% in April and -3.82% during the last week of April. If there is a singular reason “why,” it is rising worries about a global recession. Notably, it’s not coming from the U.S. or the Federal Reserve. The outlook for Fed policy hasn’t changed nearly as much as the drop in stocks would imply. Instead, it’s coming from overseas. China is doubling down on its hopeless “Zero COVID” policy, whereby it shuts down huge cities and essentially causes economic “brown outs” in an attempt to stop the spread of COVID. And since that’s a futile strategy that won’t work, markets are concerned this will go on in perpetuity. Bottom line, if the Chinese economy plunges into recession, it’s bad for every major economy (including the U.S.). Meanwhile, when Russia first invaded Ukraine, the longer this dragged on, the worse it would be for economic growth—especially in Europe, because it would continue the rapid rise of commodity prices and other inflation. Well, we are two months into the war, and there are no signs it’s ending anytime soon, and more signs it could spread beyond Ukraine into Moldova. The growth headwinds from this war are raising the chances of a recession in Europe and the UK, and if that happens it’ll be bad for every major economy (including the U.S.). Bottom line, what’s changed is that worries about a global recession have surged given 1) concerns about Chinese growth 2) the Russia/Ukraine war isn’t ending anytime soon and may actually spread. That’s one reason the S&P 500 is down so sharply.

2. What Makes It Stop?

The core concern is a looming global slowdown, so we have to get news that reduces that concern. Specifically, that means 1) China reversing its “Zero COVID” policy or COVID subsiding so there are no more lockdown threats, 2) Russia and Ukraine declaring a ceasefire or truce, and 3) the Fed backing off its hawkish rhetoric. Unfortunately, none of those events are likely near term, and until some of them at least partially occur, it’ll be tough for stocks to mount a real rally.

3. How Bad Could It Get?

For those that have been with us for some time, you probably have been through a few cycles of this type of action with us. As the market sells off, the worst fears come to the forefront, and bearishness rises to the extent that we begin to hear downside stock market targets that seem absurd from otherwise reasonable investors.

For those that were with us during the early 2020 market melt-down, you likely remember that as we were approaching the lows, you would see analysts and investors post about how the stock market had to continue lower. This is what emotion does to us as the market approaches the lows. It makes us “feel” as though the downside will never end. We believe we are closer to the stock market finding a bottom in the 3930-4040 area on the S&P 500.

I want to highlight something I took note of this past week that did surprise me. The American Association of Individual Investors Survey registered only 16.4% of investors surveyed that expected stock prices to rise in the coming six months; the highest amount of pessimism since 1990.

“Bullish sentiment, expectations that stock prices will rise over the next six months, decreased by 2.4 percentage points to 16.4%. This is just the 35th time in the history of the survey that bullish sentiment is below 20%. (The survey was started in 1987.) Optimism is below its historical average of 38.0% for the 23rd consecutive week and is at an unusually low level (below 27.9%) for the 13th time out of the last 16 weeks.

Neutral sentiment, expectations that stock prices will stay essentially unchanged over the next six months, fell by 13.1 percentage points to 24.2%. The drop puts neutral sentiment below its historical average of 31.5% for the first time in six weeks.

Bearish sentiment, expectations that stock prices will fall over the next six months, rose sharply by 15.5 percentage points to 59.4%. Pessimism was last higher on March 5, 2009 (70.3%). This is the fourth consecutive week and the 22nd time out of the last 23 that bearish sentiment is above its historical average of 30.5%. It is also the 12th time out of the last 15 weeks with an unusually high level of pessimism.

This week’s bearish sentiment reading ranks among the 10th highest in the history of the survey. This week’s bull-bear spread (bullish minus bearish sentiment) of –42.9% is the sixth most negative it has ever been.”3

This is likely the most significant news that came out this past week, and most investors likely did not even know it. You see, when the boat gets tilted a bit too much on one side, well, we all know what happens. And, it seems that the bears are seriously tipping the boat. While I do not rely often upon the AAII survey as I do not see a huge amount of value from it most of the time, the times to really take note are when it is flashing an extreme sign. And, I believe we are seeing an extreme sign.

As Mr. Rotblutt, the editor of the AAII Journal, also appropriately noted:

“Historically, the S&P 500 index has gone on to realize above-average and above-median returns during the six- and 12-month periods following unusually low readings for bullish sentiment and for the bull-bear spread. (This week’s bull-bear spread of –42.92% is unusually low too.) Unusually high bearish sentiment readings historically have also been followed by above-average and above-median six-month returns in the S&P 500.”3

Also in his article, he outlined the reasons cited by investors as to why they did not expect a bullish resolution to the current market conditions. And, if you would read the article(click here to read), you would see the usual suspects that we have all been hearing about of late: Russia, inflation, supply shocks, earnings expectations, etc.

But, consider whether this is worse than the economic shutdowns, high Covid deaths, record unemployment, economists declaring us to be in recession, earnings estimates being slashed like we experienced at the bottom of the market in March of 2020 right before the S&P500 went on a parabolic 1000+ point rally. To be honest, we really do not even have to make a comparison. The point is that the significant majority of the market is not bullish, and they clearly have their “reasons” to be so. But, historically, such bearishness has led to rallies rather than breakdowns. Of course, this time may be different, but that is why we use our market analysis to guide us.

By the time you read this, the Federal Reserve will have met on May 3-4. Over the last several weeks, we have seen almost every single Federal Reserve member talk about how much they need to raise interest rates to catch up with inflation due to policy mistakes last year believing that inflation was “transitory” (temporary). Leading the way is Federal Reserve Bank of St. Louis President James Bullard. If he gets his way, get ready for massive rate hikes.

From CNBC:

Bullard, a voting member on the FOMC this year, said Thursday that “inflation is too high” and the Fed needs to act.

Bullard believes the central bank needs to tighten policy quickly. He’s worried that the longer it takes for interest rates to rise, the worse the inflation problem will grow. But there’s a twist: he feels policy doesn’t just need to go to a point where inflation stops rising, he thinks rates must rise to a level where prices start to contract. James Bullard is worried the central bank is behind the curve when it comes to tightening monetary policy. He said an interest-rate hike of 75 basis points, or 0.75%, is not out of the realm of possibilities. He made the comments during a presentation to the Council on Foreign Relations.

He clarified that a 50-basis-point increase is his base-case scenario for the May meeting of the policy-setting Federal Open Market Committee (“FOMC”). But he said he wouldn’t rule out the potential for a larger bump in interest rates. Such a large move hasn’t been made by the central bank since 1994. The St. Louis Fed chief is calling for an interest-rate target of around 3.5% by the end of 2022. 1

Along with the rest of the country, Jay Powell and James Bullard are both concerned with inflation’s explosion higher. The Fed is worried the longer it waits to adjust policy, the more prices for everything will increase. Other governors and regional bank presidents have been calling for rapid policy tightening. But the more inflation rises, the greater damage it can cause to economic output. As households see more money going to the same amounts of gas and bread, they worry. They realize they have less money to spend on things they want.

Consumers have no way of knowing when price increases will stop. They see the negative headlines every night about China, Russia, and Ukraine. Households begin to lose confidence in the economy. So they spend less because they’re unsure about the future. That’s a big problem for the economy. According to the St. Louis Federal Reserve, consumers account for almost 70% of gross domestic product (“GDP”). If confidence goes down the tubes, the economy is going with it. Compounding the problems are Russia’s war in Ukraine and the COVID-driven lockdowns in China. The Ukraine conflict has limited the supply of energy and grain stores available for global consumption. China’s zero-COVID policy has halted the manufacture and export of goods. The loss of these items is driving high inflation even higher. Demand hasn’t dropped as supply has dwindled. The dynamic means prices will go up. Food costs will rise and companies have to pay more to produce anything.

So the central bank has two choices…

It can act aggressively now or wait until the problem gets worse. But if inflation continues to run at its current rate, the interest-rate increases will be even worse down the road. Both Powell and Bullard feel that by following this course of action, the central bank can stop inflation’s rise. In short, they want to stop the bleeding. They don’t think inflation will drop to the Fed’s 2% target right away. But by getting policy back to neutral, it will be easier to make the appropriate interest rate changes going forward.

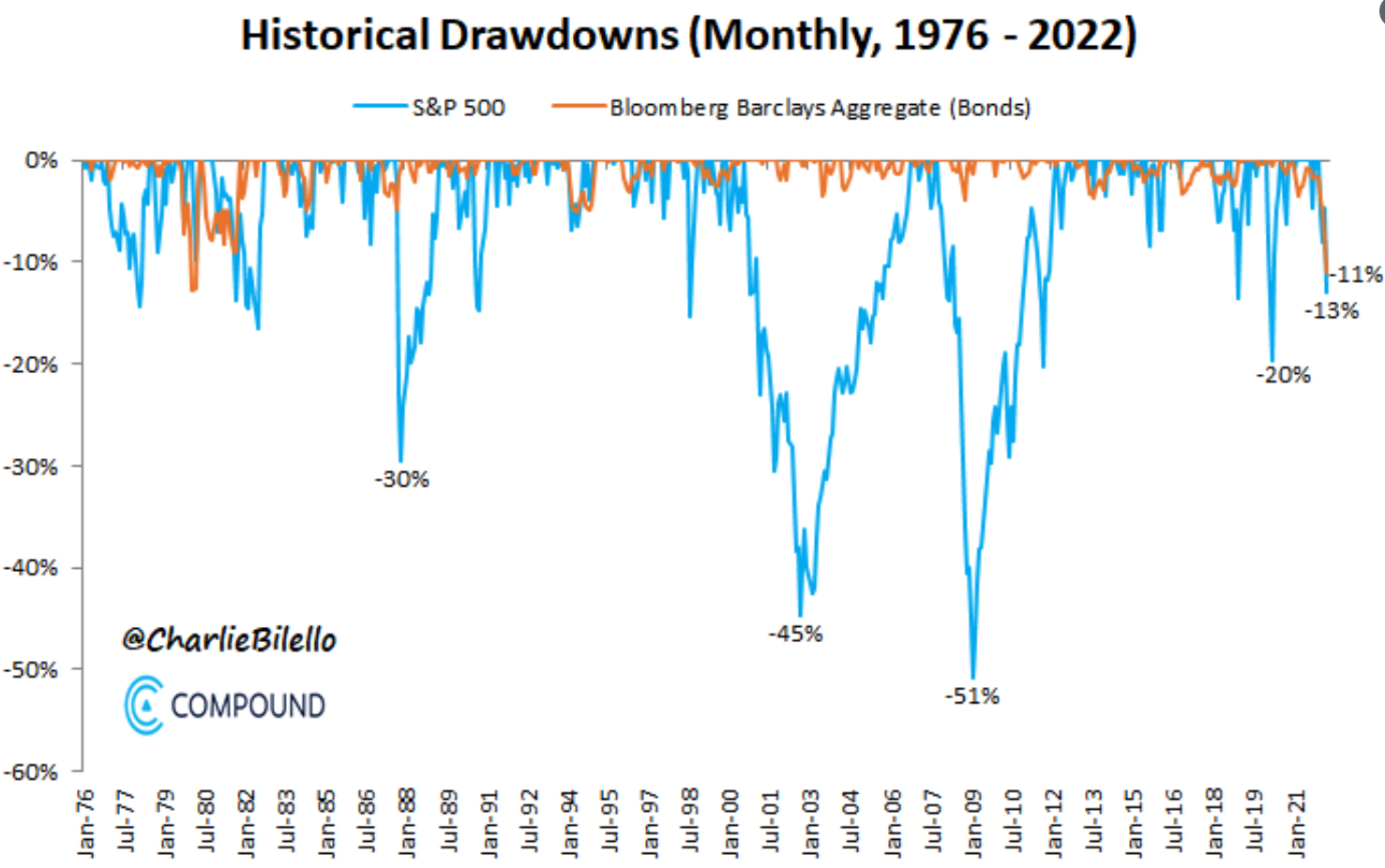

In response to all this hawkishness, the 10-year Treasury yield has been surging. As I write Monday morning, it’s at 2.99%, the highest level since early 2019. I want you to think back to March 2020 and the 35% drop in the S&P 500 in 33 trading days. Well, we are witnessing very similar types of moves in the bond market.

From market researcher Jim Bianco: “The carnage is epic. This is not only the worst bond market in our career (total return) but might be the worst of our lifetime.”2

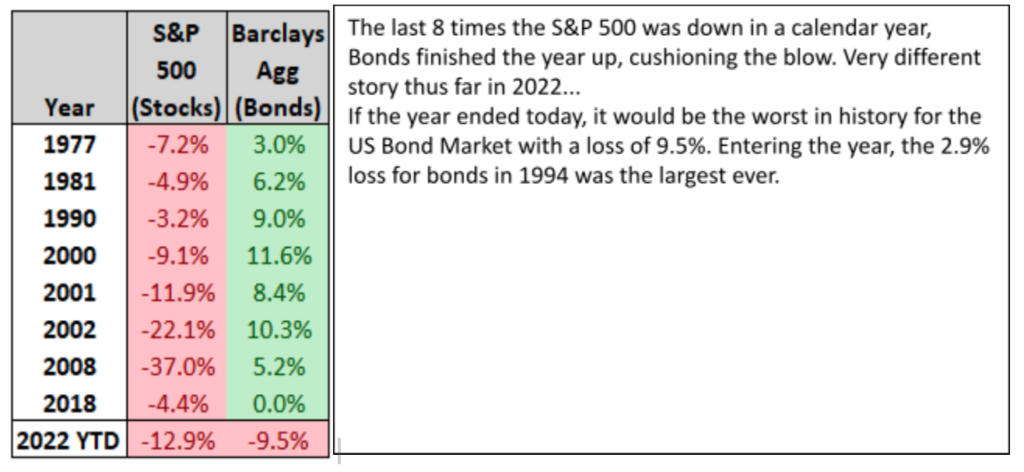

With data going back to 1976, this is the first time ever that both stocks and bonds are in a >10% drawdown at the same time. The S&P 500 is in a 13% drawdown while bonds are 11% below their 2020 high. (note: using monthly total return data)

As noted previously, we’re seeing more and more Fed members turn exceptionally hawkish, upping their interest rate targets, as well as the speed with which they want to reach those targets. The problem is that, just like driving a car, when you accelerate incredibly fast and keep your foot on the pedal, it increases the odds that a small mistake could result in big consequences.

Back to Bianco on the risk of a miscalculation:

“The Fed doesn’t want to create the mistake in the other direction by being too timid right now. That’s out the window now. They don’t want to create a broken market. They don’t want to create a recession. But when you go down that path and you’re that adamant about trying to rein in inflation, it makes it very likely that you will create a mistake…It will be 50 [basis points] all the way through until the Fed basically raises rates too much and breaks something.”2 It is also not comforting to know that the Federal Reserve has not successfully implemented a plan of ending quantitative easing without causing a recession.

In the meantime, I just want to conclude with the perspective that I still think the stock market is likely bottoming. Lastly, I want to remind you that even if we do bottom over the coming weeks, it will likely still take us a number of months before we are ready to break out to new all-time highs. In the meantime, we will let the bulls and bears battle it out. So, it will not likely be until the fall before we see new all-time highs, or maybe even a bit later. And, to be honest, I cannot even imagine the amount of bearishness we may see at those lows. You will have to emotionally prepare as we get closer to the completion of this decline. You see, the closer we move to that target, the more you will hear about targets of 3800, 3600, and even 3000. Remember, the more the market drops, the more bearish participants become. We still remain very bullish for the last half of 2022.

2 https://www.cnbc.com/2022/04/07/carnage-is-epic-in-bonds-due-to-feds-inflation-error-jim-bianco.html

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Information has been obtained from sources believed to be reliable and are subject to change without notification. The information presented is provided for informational purposes only and not to be construed as a recommendation or solicitation. Investors must make their own determination as to the appropriateness of an investment or strategy based on their specific investment objectives, financial status and risk tolerance. Past performance is not an indication of future results. Investments involve risk and the possible loss of principal.