The invasion of Ukraine is a serious and scary escalation in tensions between Russia, Europe, and the United States. Before we dive into what it could mean, let’s take a moment to think about the many folks who are suffering and dying as well as the ordinary Russians who will suffer from sanctions, instability, and economic damage.

Given Ukraine’s critical pipelines and Western sanctions on Russia, the crisis is leading to higher energy prices, which is increasing gas prices and heating fuel costs. We will discuss this in more detail in addition to why inflation will continue to be higher in the months ahead.

Interest Rates and the Federal Reserve

During Jay Powell’s Congressional and Senate testimony on Wednesday, March 2, he stated “The implications for the U.S. economy are highly uncertain, and we will be monitoring the situation closely. The near-term effects on the U.S. economy of the invasion of Ukraine, the ongoing war, the sanctions, and of events to come, remain highly uncertain,” he added. “Making appropriate monetary policy in this environment requires a recognition that the economy evolves in unexpected ways. We will need to be nimble in responding to incoming data and the evolving outlook.” Jay Powell said he still sees interest rate hikes ahead though he noted the “implications for the U.S. economy are highly uncertain” from the Ukraine war. (1)

The next Federal Reserve meeting is scheduled for March 15-16th. During their meeting, the Federal Reserve will start to raise interest rates, at a minimum of 25 basis points, or .25%. We have discussed how far behind the Federal Reserve is on raising interest rates. How much and how fast will be determined by the economy and inflation.

Stock Market Performance

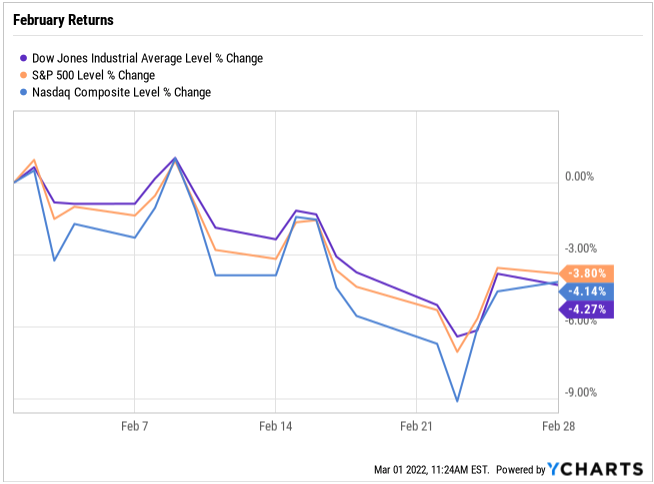

For the month of February, the Dow Jones Industrial Average declined 4.27%, the S&P 500 declined 3.80% and the Nasdaq declined 4.14%.

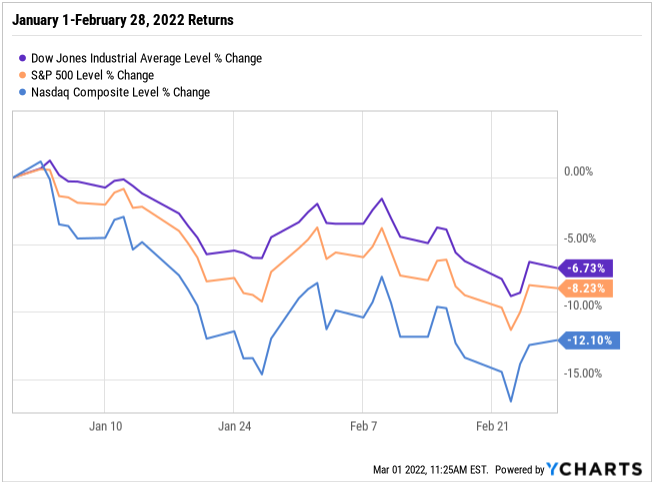

From January 1-February 28th, the Dow Jones Industrial Average is -6.73%, the S&P 500 is down -8.23% and the Nasdaq is -12.10%.

S&P 500 Corrections > 5% since March 2009 Low

We have updated this chart to reflect the S&P 500’s -14.6% intra-day decline through February 24th. This is the greatest decline we have seen since the -35.4% decline in March 2020.

Every one of these events would have represented a great reason to sell in the moment, had you been around for it. All of those sales would have been regretful not long after. The declines we have experienced have created excellent opportunities for us.

This does not make going through a market correction or the volatility we are experiencing any easier. But I do want to highlight what we wrote in our 1st Quarter market update “But just begin to mentally prepare yourself for the certain and likely deep bearishness that the next expected decline will elicit as we look toward early 2022. We will need to see that extreme bearishness in order to set up the rally to 5163-5500SPX later in 2022. So, while you will undoubtedly be bombarded with many “beliefs” that the bull market is over, I still maintain a high probability expectation that 2022 will see further gains in the market.

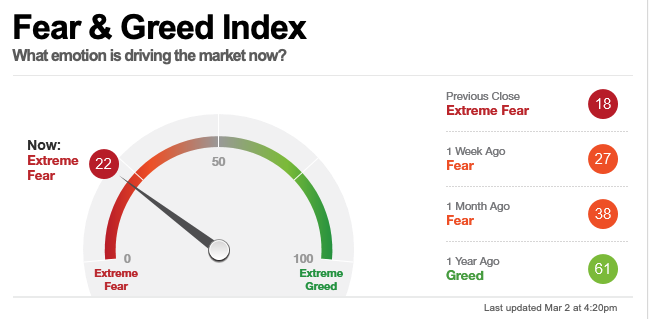

Keeping with our comments, the majority of American investors are once again very scared about the stock market. In fact, CNN’s “Fear & Greed Index” shows that we hit “Extreme Fear” levels several times toward the end of 2021 – for the first time since the bottom of the COVID-19 crash in 2020. And with the market’s recent sell-off, investors are getting scared once again. We are currently at an extreme fear reading of 22, up slightly from a level of 15 on February 24th, however still in an area that we want to focus on buying opportunities.

And as we’ve seen throughout history, these moments of extreme pessimism and fear – like what we’re seeing right now – make the best opportunities for investors…

Of course, we saw it again in mid-2020, when COVID-19 was still casting a long shadow of pessimism over our country’s economy. And we all know what happened next… Stocks went on to double off their March 2020 bottom. Although we are not expecting the type of performance from the March 2020 bottom, we are still expecting better markets as we get into the second quarter and the remainder of this year.

This chart below shows the few times the Fear & Greed Index has approached extreme fear levels. The few times it touched the extreme fear level in 2021 and in March 2020, have produced excellent buying opportunities. Now is another time that we have entered the extreme fear levels below 25.

These are the times to take advantage of opportunities, usually when they are the hardest from a mental and emotional standpoint.

Inflation and Commodity Prices

We have been consistent in the fact that we believe inflation will be with us longer than most analysts and news media is telling you. The increase in not only energy prices, but grain prices will continue to elevate inflation levels as well as the prices we are (and will) be paying at the grocery store. The first reason is that Russia is one of the world’s three largest oil producers, along with the United States and Saudi Arabia, and plays a central role in OPEC+ (the Organization of the Petroleum Exporting Countries and allied producers).

The last week of price action in the energy markets have been unprecedented and historic as the Russia/Ukraine conflict has fueled demand across the oil and refined products complex, sending prices to multi-year, and in some regional markets, all-time highs.

The International Energy Agency agreed Tuesday to release 60 million barrels of oil from global reserves, in an effort to ease some of the current supply constraints. According to the agency, the 60 million barrel release accounts for 4% of members’ emergency stockpiles of 1.5 billion barrels. Half of that total — 30 million barrels — will come from the US Strategic Petroleum Reserve, and the other half will come from allies in Europe and Asia. Those other allies include Germany, the United Kingdom, Italy, the Netherlands and other major European countries, as well as Japan and South Korea. (2)

The coordinated drawdown is just the fourth such effort in the IEA’s history. 60 million barrels will do little to meaningfully move the needle and is not enough to absorb lost supply from Russia. The number is equivalent to about 6 days of Russian production, and about 12 days of Russia’s exports. (2)

On Monday February 28, Canada said it was banning Russian oil imports, but so far it’s the only nation to target Russia’s energy complex directly. The financial sanctions imposed by the U.S. and Western allies could carve out room for energy payments to continue.

But the ripple effects are already showing. Ahead of Russia invading Ukraine the global oil market was already tight. Demand has bounced back, while supply has remained constrained.

The prospect of supply disruption is fueling higher prices due to several factors:

- The oil demand recovery from Covid-19 has been stronger than many expected

- Supplies have not kept pace as OPEC+ is still unwinding its production cuts and only adding approximately 400,000 new barrels of production monthly

- U.S. shale companies continue to take a cautious approach to spending and are not investing in new oil wells

- The market is focusing on concerns about low spare capacity and inventories, as well as depressed investment by the global oil and gas industry since 2015.

With the Biden administration’s pursuit of a “clean energy revolution, we’ve knowingly ceded control of the oil market to OPEC. And OPEC has every incentive to drive prices higher. Add to this, we now have the additional catalyst of a potential shock to an already undersupplied market. If sanctions were placed on Russian energy exports, there’s no telling how high the crude oil market might spike.

Bottom line, the energy markets are in turmoil right now with a drastic supply and demand imbalance having emerged due to the sanctions on Russia. Looking forward, that will continue until there is a resolution to the conflict with Ukraine and the sanctions are ultimately removed. At this time, the market is “demanding” a ceasefire and unwind of sanctions with screaming oil prices and seeing a $125/barrel oil print before the end of the week. That is by no means out of the question if there isn’t some degree of desolation.

You may not be aware of this fact. Ukraine is the world’s fourth-largest exporter of both corn and wheat. It is also the world’s largest exporter of sunflower seed oil, an important component of the world’s vegetable oil supply. Together, Russia and Ukraine supply 29 percent of all wheat exports and 75 percent of global exports of sunflower oil. (3)

Russia’s invasion of Ukraine could push U.S. food prices even higher while the disruptions could drag on for months or even years, as crop production in the area could be halted and take a long time to restart. This new inflation shock comes at a time when global markets remain extremely strained because of pandemic-related disruptions. The price changes impacted commodity prices in recent days and could flow through to higher costs at grocery stores and restaurants soon.

Grocery manufacturers are concerned that, while the vast majority of ingredients and materials for American products are sourced domestically, the economic effects of Russia’s invasion of Ukraine will be global.

According to Katie Denis, vice president of communications and research for the industry organization Consumer Brands Association, “We’re already seeing energy prices rise and commodities futures for wheat and corn spike. That’s going to prompt concern when costs to make and ship goods continue to set records and consumer demand continues to be above levels not seen since March 2020,” she said. “There is no slack in the system, making weathering disruption significantly more difficult.”

Bottom line, the energy markets are in turmoil right now with a drastic supply and demand imbalance having emerged due to the sanctions on Russia. Looking forward, that will continue until there is a resolution to the conflict with Ukraine and the sanctions are ultimately removed. At this time, the market is “demanding” a ceasefire and unwind of sanctions with screaming oil prices with the possibility of seeing a $125/barrel oil price. That is by no means out of the question if there isn’t some degree of desolation.

Below is a chart of the Bloomberg Commodity Index. This index is made up of energy, grains (corn, soybean, wheat, soybean oil), soft commodities (OJ, coffee, cotton), livestock and industrial metals (copper, aluminum, nickel, zinc). As you can see, commodities continue to increase at a rapid pace as the majority of all commodities to make new highs in prices.

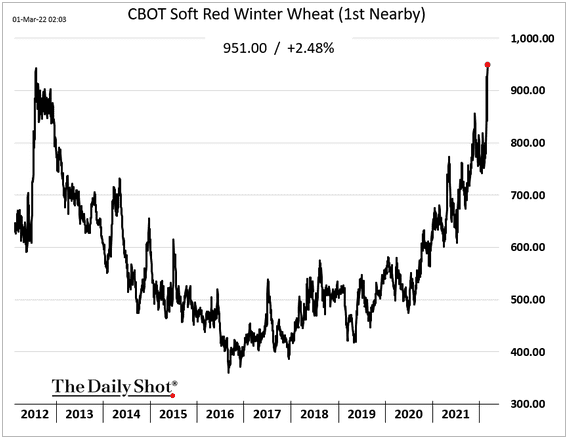

Here is a chart of wheat futures with prices exceeding the highs back in 2012.

Market Outlook

Let’s take a look at the bigger picture. We have been very vocal and consistent that we would see more volatility in 2022 as well as a 7%-10% pullback in the market sometime during the first quarter. We have experienced both volatility and the pullback in the market.

So although the “news” is still not getting any better, the market is still following our price patterns that we have been laying out over the past several weeks and we have been able to take advantage of the pullback opportunities. We believe we have seen the bottom, leaving plenty of room to the upside in the coming months. It is during these times when we see the market move in opposition to what the “news” would suggest.

To summarize, we have a set up in place with extreme bearishness in the stock market, the S&P 500 has approached our downside objectives and there are news headlines about how we are now in a bear market, all which we have prepared you for as we entered 2022. This is why we focus on market sentiment which is what drives the stock market, not news headlines, presidential elections, or wars.

We understand the risks facing both the markets and the economy, and we are committed to helping you effectively navigate this still-challenging investment environment. Successful investing is a marathon, not a sprint, and even intense volatility is unlikely to alter a diversified approach set up to meet your long-term investment goals.

Therefore, it’s critical to remain patient and stick to the plan, as we’ve worked with you to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.”

W remain vigilant toward risks to portfolios and the economy, and we thank you for your ongoing confidence and trust. Please rest assured that our entire team will remain dedicated to helping you successfully navigate this market environment

Please do not hesitate to contact us with any questions, comments, or to schedule a phone call or web meeting/in person meeting click here.

________________

(3) https://www.washingtonpost.com/business/2022/02/26/ukraine-russia-wheat-exports/

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.