By Matthew Gaude & Shawn McGuire

The marathon journey to retirement is nearly over, and the finish line is finally in sight! You’ve been working your whole life to reach this milestone, and you’re ready to put those years of calculating, strategizing, and saving behind you. But if you’re feeling tempted to hang up your financial planning hat…not so fast. In order to take full advantage of your golden years, it’s important to continue to make sound financial decisions and take action when it comes to your financial strategy.

Retirement brings its own set of challenges to the table, and we’ve found that most retirees face the same 5 financial planning challenges within the first 10 years. Let’s discuss these challenges so you can be prepared and confident to tackle them.

1. Not Creating a Withdrawal Strategy

This is an area you may hear least about when it comes to retirement planning. This is tax planning, reviewing your tax return and most importantly, distribution optimization. You’ve saved for years, and now you need that money to live on. How you take it out is just as important as how you put it in. That’s why you should capitalize on your wealth by determining a tax-efficient way to withdraw funds in your golden years.

Different financial accounts are taxed at different rates. Traditional IRAs and 401(k)s get taxed at the ordinary income tax rate when you withdraw. Roth IRAs and Roth 401(k)s are taxed beforehand, so the money is withdrawn tax-free. Funds in a taxable investment account are taxed at the capital gains tax rate, which is different than your ordinary income tax rate.

Calculating when might be the best time to pull from each account is enough to give anyone a headache. But the last thing you want is to get hit with a hefty tax bill when you’re trying to stretch your money for decades.

We review our client’s tax returns. We run diagnostic reports and discuss them with our clients. We discuss tax tips. And we review their retirement accounts and discuss the best way to distribute income so you are not paying extra taxes, especially when you turn 72. We also discuss the benefits of Roth conversions as a generational wealth transfer tool, among other concepts.

Creating a withdrawal strategy with the help of a trusted professional can help ensure you’re withdrawing funds at a sustainable rate and that you’re doing it in a tax-efficient way.

2. Throwing the Budget Away

Many people spend their retirement years doing all the things they never got to do when they were working: starting a passion project, remodeling the house, traveling the world, and more.

It’s easy to underestimate the amount of money you’ll spend during those first few years when you don’t account for all these “extras.” Overspending, even for a short period, can shave years off the longevity of your assets. The solution? Create a spending plan. Calculate your monthly income given your withdrawal strategy, and then create a budget, tracking your money along the way so you stick to your goals.

3. Ignoring Inflation

Another major challenge we see new retirees face is the desire to play it safe in the stock market. This can do more harm than good as it can lead to inflation risk.

The long-term average inflation rate for healthcare expenditures is 5.25%, (1) and the current average inflation rate is a whopping 5%. (2) This means retirees are more likely to feel the effects of inflation due to necessary expenses, such as healthcare costs.

As tempting as it may be, resisting the urge to worry about short-term stock market volatility may be a good option. With a retirement that could easily last 20 to 30 years, inflation is still a significant threat to your nest egg. Sit down with a trusted professional who can help you strike a balance between principal protection and growth.

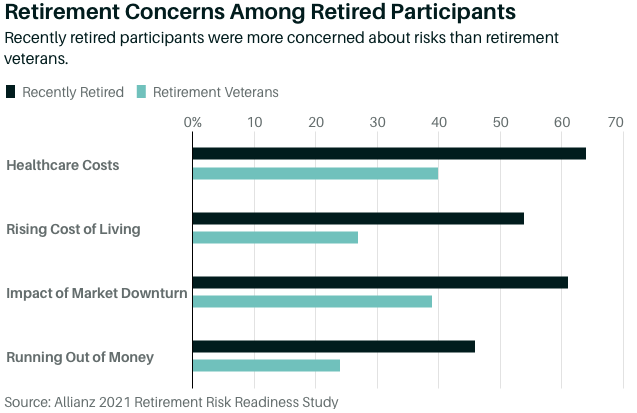

A 2021 Retirement Risk Readiness Study from Allianz insurance company found that 71% of participants were worried about the rising costs of healthcare, 67% were worried about rising costs of living, and 66% were worried that market downturns would affect their savings. These percentages represent significant increases from the survey’s 2020 results. (3)

Overall, however, concerns were not uniform across the age groups. People who had retired within the previous 10 years were more concerned than those who had been retired for more than 10 years. Nearly 65% of recent retirees were worried about healthcare costs being too high, compared with 40% of retirement veterans. Similarly, 54% of newly retired respondents were worried about rising costs of living, compared with 27% of veterans. Newer retirees are looking at rising consumer prices and “are feeling terrified,” whereas those who have been retired for more than 10 years benefitted from some of the best conditions for retirement— a strong bull market and controlled inflation.

4. Neglecting to Create an Emergency Fund

Could you comfortably pay for an unexpected, major expense in retirement without jeopardizing your financial future? For most of us, the answer is no. Just as you were taught to have an emergency fund in your formative years, it’s even more critical to have one in your retirement years.

Most professionals recommend that retirees have at least 12 to 18 months of expenses in an easily accessible savings account. (4) This may sound like a lot, but an emergency fund serves two purposes: it covers unexpected expenses and it can provide stability during economic downturns. This means you can optimize your portfolio to help beat inflation, as suggested above, while having a safety net to fall back on.

There are other factors that should be considered in determining how much of an emergency fund to maintain, including pensions, other guaranteed income streams, and your required minimum distributions (RMDs). Working with a professional can help you determine how much of an emergency fund to maintain given your specific situation.

5. Planning on Your Own

When facing any challenge, you know that the best outcome results when you seek out the professional most qualified. You turn to a doctor for health concerns. You turn to a mechanic for car trouble. So although you might have DIY’d your personal finances up until now, retirement is not the time to wing it. Having a trusted wealth manager by your side can be the difference between having a retirement fund that dries up or one you can’t outlive.

To learn more about our TRAC financial planning process, click here. We must be able to focus on investment management, financial planning and tax planning and distribution optimization. If you envision a 3 lane highway, we must be able to change lanes when needed, and merge the various disciplines to get the best results for our clients. By only staying in one lane-by focusing exclusively on investment management, you miss out on the benefits that come with considering financial planning and taxes, which are the other two lanes. In short, you compromise your financial well-being by focusing only on one area.

Our team at Live Oak Wealth Management would love to be the qualified professionals you turn to for help tackling these challenges (and others) on the road to a comfortable retirement—in fact, our focus is to secure, maintain, and protect your financial lifestyle throughout every stage of life. If you would like to find out more about how we can help, call our office at 770-552-5968 or email [email protected]. Or, if you prefer, you can simply click here to schedule an appointment online.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.

________________

(1) https://ycharts.com/indicators/us_health_care_inflation_rate

(2) https://www.usinflationcalculator.com/inflation/current-inflation-rates/

(4) https://www.thebalance.com/how-much-emergency-savings-do-retirees-need-4582473