By Matthew Gaude & Shawn McGuire

We still have plenty of time until the election, and at this point, who our President is come January is still anyone’s guess. But regardless of your preferred candidate, you are probably curious and maybe a bit nervous about how things will look once the election is over and we learn who will be leading our country for the next four years.

We recently discussed what a Trump second term might look like in terms of the economy, and now it’s time to turn to Biden and make some observations on the impact of a Democratic win on the markets and what that might mean for your finances.

A Note On History

As we discussed in our last article, history can tell us a lot about elections, presidents, and the markets. And while there’s no doubt that presidential policies do impact the economy, remember that timing is just as important as who is Commander In Chief. Regardless of who was in office when, every President experienced different international conflicts, civil unrest, job market fluctuations, or societal changes that also played into stock performance.

For example, when Nixon resigned after being threatened with impeachment, there was a sharp drop in the stock market. But was that the cause? Was it dependent on what year it was in the election cycle or what party was in the House or Senate? When that event happened, stocks were already being pulled down by a global oil shock, runaway inflation, and turmoil in the Middle East. Then there’s Clinton, who also faced impeachment but didn’t experience the same situation as Nixon. Instead, the S&P 500 continued its upward trajectory in spite of the impeachment proceedings. Often it’s the timing that matters more than the name of the person in office.

Biden’s Policies And The Economy

Let’s look at some areas where Biden’s policies could impact you and our economy as a whole. Many taxpayers are still learning about the agenda from Democrats should they regain power, and in particular, former Vice President Biden’s tax plan. In what is likely to be of little surprise to most Americans given the Democrats’ party platform, the cumulative tax proposals supported by presidential candidate Biden would create a more progressive tax system than we have today.

What might surprise you however, is just how progressive the sum of his proposed changes might be for certain high earners, but also because the potential for 2021 to be a major year of tax legislation that could influence tax planning today, through the end of the year (after the election outcome is determined), and into early 2021 as new legislation is finalized and potentially passed.

Taxes

The centerpiece of candidate Biden’s proposed changes to ordinary income tax brackets is a pledge not to increase tax rates on those making less than $400,000, and that various changes (from new income tax brackets and restrictions on deductions) would only impact earnings above the $400,000 threshold.

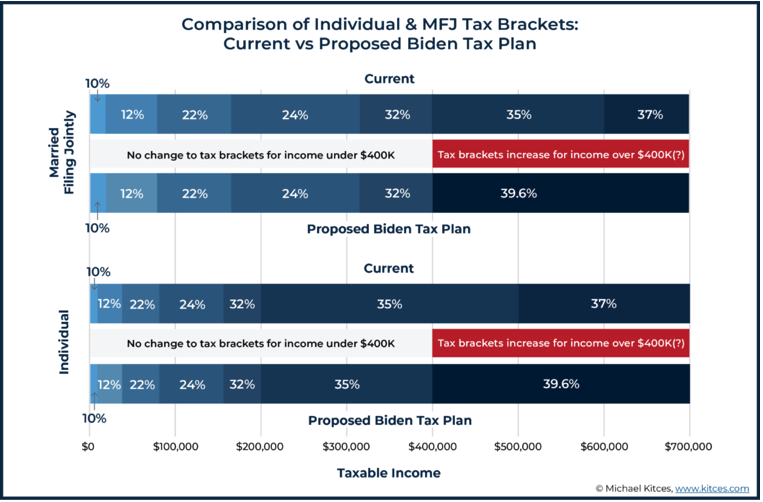

BIDEN TAX PLAN WOULD INCREASE THE TOP ORDINARY INCOME TAX RATE (BACK) TO 39.6%

One issue that always tends to garner a lot of interest is the top marginal income tax rate proposed by a candidate. To that end, Vice President Biden has proposed an increase of the top ordinary income tax bracket from the current top rate of 37%, to the top pre-Tax Cuts and Jobs Act rate of 39.6%. Absent legislation, this change is actually already scheduled to occur, as a part of the so-called “sunset” of the Tax Cuts and Jobs Act in 2026; by contrast, Biden’s proposal would advance the 2026 date forward to 2021 (or the soonest that his tax legislation could be implemented). (1)

Notably, though, while the Biden proposal would “only” increase the top ordinary income tax rate to its pre-TCJA level of 39.6%, it would lower the income threshold at which that top rate would apply.

More specifically, in 2017 the 39.6% ordinary income tax bracket did not apply to single filers until they had taxable income of more than $418,000. And it didn’t apply to joint filers until they had taxable income that exceeded $470,000!

BIDEN TAX PLAN WOULD ELIMINATE THE QUALIFIED BUSINESS INCOME (QBI) TAX DEDUCTION FOR HIGH EARNERS

$400,000 seems to be the “magic” number that Vice President Biden has settled on when it comes to figuring out whose income tax liability should be left alone, and who should be responsible for picking up more of the overall tax burden. To that end, in addition to imposing a “new” top tax rate of 39.6% on those taxpayers with $400,000 or more of income, the Biden tax plan also proposes to completely eliminate the Qualified Business Income (QBI) deduction for such individuals as well.

Under current law, the Qualified Business Income (QBI) deduction allows various “pass-through” business owners (including owners of partnerships and LLCs, S corporations, and even sole proprietors) to deduct 20% of their business income from their business income, such that they are only taxed on the remaining 80% of their income. This effectively reduces the tax bracket for pass-through business income by 20% of the otherwise-normal tax rate.

By contrast, under the new Biden proposal, the QBI deduction would no longer be available to anyone earning more than $400,000/year, regardless of whether their pass-through business was a Specified Service Trade or Business, or not. And because the QBI phaseouts have in the past been determined based on an individual’s own tax return, ostensibly even if one or multiple businesses all stayed under the $400,000 threshold, as long as the business owner’s income reaches or exceeds the threshold, the QBI deduction would be lost, even if the income threshold was breached due to non-business (i.e., other wage or portfolio) income!

BIDEN TAX PLAN WOULD CAP THE VALUE OF ITEMIZED DEDUCTIONS AT NO MORE THAN 28%

For high-earning individuals, the news doesn’t get much better on the deduction side of things. Specifically, the Biden tax plan calls for resurrecting an Obama-era proposal to cap the value of itemized deductions at 28%.

For taxpayers in the 10%, 12%, 22%, and 24% marginal brackets, this proposal would have little to no impact. Taxpayers in the 32%, 35%, 37%, or the proposed “new” 39.6% bracket, on the other hand, could see a substantial increase in their effective tax rate. For instance, a client in the proposed “new” 39.6% bracket who earns $5,000 and then immediately donates those dollars to charity would receive a $5,000 x 28% = $1,400 deduction. But their original tax bill on that $5,000 of income would have been $5,000 x 39.6% = $1,980, which in turn would still leave them with a $1,980 – $1,400 = $580 tax bill (the 11.6% tax rate differential) attributable to the $5,000 of income that they had earned and immediately donated and didn’t even have anymore!

Accordingly, the more a client’s marginal income tax bracket exceeds the 28% proposed cap for the benefit of an itemized deduction, and the greater the extent that the individual relies upon (or benefits from) itemized deductions reducing their tax bill, the greater the risk this proposal has to reduce their net-after-tax income. At a top tax bracket of 39.6%, this proposal would effectively result in a tax bracket as high as 11.6% on funds that were already received and donated.

NEW AND EXPANDED PERSONAL INCOME TAX CREDITS UNDER BIDEN TAX PLAN

Vice President Biden’s progressive tax proposals are further bolstered by an array of new and expanded credits, primarily targeted at lower- and middle-income households where they are most commonly utilized.

Such personal tax credits include:

- Child tax credit: The current credit of $2,000 per child under age 17 would be increased to $3,600 for children under age 6, and $3,000 for all other children under age 17.

- Child and dependent care credit: The current credit of a maximum of $3,000 for one child, and $6,000 for two or more children would be expanded to a refundable credit of $8,000 for one child, and a whopping $16,000 credit for two or more children.

- First-time home buyer credit: A new refundable and advanceable credit of up to $15,000. While specifics surrounding the credit have not yet been made public, the credit would most likely mirror the first-time home buyer credit first introduced during the (George W.) Bush administration in 2008, and later expanded by the Obama administration in 2009. In both situations, the maximum credit was capped at 10% of the purchase price of the home.

- Caregiver credit: A new credit of up to $5,000 would be created to assist individuals who provide informal care to those in need of long-term care. Additionally, Vice President Biden’s plan calls for enhancing the current tax breaks associated with the purchase of long-term care insurance, though how exactly that would be done is not entirely clear. (2)

BIDEN TAX PLAN PROPOSAL TO INCREASE LONG-TERM CAPITAL GAINS RATES BACK TO ORDINARY INCOME ABOVE $1M AND LIMIT 1031 EXCHANGES

While Vice President Biden has chosen $400,000 of income to be the “magic” income number when it comes to increasing a client’s ordinary income tax rate, over in “long-term capital gains land,” the new “magic” income threshold is $1 million. More specifically, to the extent that a taxpayer’s income exceeds $1 million, the Biden tax proposal calls for taxing both long-term capital gains and qualified dividends at ordinary income tax rates (which at that point would be 39.6%)…plus the 3.8% surtax on net investment income that would still apply as well.

Nevertheless, that still means that the top rate paid on such long-term capital gains income today, at 20% long-term capital gains tax + 3.8% surtax = 23.8%, would nearly double to 39.6% +3.8% = 43.4% for those with over $1M of income!

BIDEN TAX PLAN PROPOSES ELIMINATION OF STEP-UP IN BASIS AND NEW POTENTIAL DEEMED-SALE-AT-DEATH RULE

While the potential increase in long-term capital gains (and qualified dividend) rates would have a substantial impact for top earners, it is not the only seismic shift under the Biden tax plan when it comes to capital gains. In addition to eliminating the special tax rates for long-term capital gains and qualified dividends for income over $1 million, the Biden tax plan calls for eliminating the “step-up” in basis on inherited assets at death.

Under the existing rules, when the owner of an asset dies, the beneficiary of that asset generally receives the asset with a cost basis equal to the fair market value of the asset on the date of the decedent’s death. Known as the step-up in basis rules, the primary purpose of the rules is not actually to provide a tax break per se, but simply in recognition that once the original owner passes away and the beneficiary inherits, the beneficiary often wouldn’t know what the original cost basis is, especially since the original owner would no longer be around to explain it. Accordingly, the step-up in basis rules apply to virtually all inherited assets, except for certain assets (e.g., IRAs and other retirement accounts, NUA, accounts receivable, deferred interest of EE bonds) that are excluded and remain pre-tax assets when received by the beneficiary.

Vice President Biden’s plan calls for the elimination of the step-up in basis on all (non-IRD) assets that would otherwise be eligible, and would prevent the death of an owner from “wiping clean” the potential capital gains tax bill associated with the inheritance (and subsequent sale) of an appreciated asset.

Feasibility Of Biden Tax Plan Proposal To Eliminate Step-Up In Basis

While it’s certainly possible that such a rule could eventually be adopted, there are at least a few reasons for clients fearing such a provision might consider sleeping a little easier. For starters, there have been two big efforts to eliminate the unlimited step-up in basis rule over the past 50 years, and both were unsuccessful.

In 1976 Congress eliminated the step-up and implemented carryover basis. The decision proved so unpopular with the American public (and perhaps more significantly, financial institutions) that implementation was repeatedly delayed until Congress finally just undid the change altogether in 1980. And in 2010, the estate tax was supposed to be eliminated altogether, with carryover basis reinstated. But before the end of even that first year (2010), Congress had already given taxpayers the opportunity to opt back into the estate tax with an unlimited step-up in basis and had made the system “permanent,” and the only choice again beginning in 2011. Again, this was in part due to the reality that financial institutions, and the IRS itself, still weren’t sure how to track and determine compliance with the proper reporting of cost basis by a beneficiary that might not be due until years or decades after the original decedent passed away. (3)

BIDEN TAX PLAN CALLS FOR A RETURN TO THE PRE-TCJA FEDERAL ESTATE AND GIFT TAX EXCLUSION

Vice President Biden’s proposal for estate and gift taxes is rather straightforward. Notably, while not as progressive of a change as others in his own party have called for, Biden’s plan calls for an immediate halving of the current $11.58 million lifetime exclusion amount that applies to both estate and gift tax, reverting back to what the inflation-indexed exemption would have been under President Obama’s (and Vice President Biden’s) rules while they were in office. Notably, this lapse of the current estate tax exemption amount back to its pre-TCJA limits is already scheduled to occur in 2026 (after the Tax Cuts and Jobs Act sunsets), but the Biden tax plan would accelerate that reversion back to the old limits in 2021 instead.

Of course, even at roughly $6 million per person of lifetime exemption amount, the overwhelming majority of Americans would continue to be able to sleep well knowing that their new worth was not large enough to “burden” heirs with an estate tax liability (especially given the portability of the unused exemption to a surviving spouse, allowing nearly $12M of estate tax exemptions for a married couple).

Regulation

Increased regulation under a Democratic government could impact the finance industry as well as the energy section, especially oil and gas companies because of a stronger focus on alternative energy. It’s unlikely we’ll see anything resembling “Medicare for All” from a Biden administration, but we could see some expansion of the Affordable Care Act. (4) We all know that trade has been a hot-ticket issue under President Trump, especially with China. This uncertainty can often lead to supply chain issues, which can then lead to higher costs for businesses. Under Biden, trade issues may not be as volatile.

Local And State Governments

Biden may place more attention on local and state governments, including tax deductions, and COVID-related support, which could lower municipal bond default risk.

Sit Tight Before Taking Action

A lot of people are asking, “What do we do now? What are the things that we should be concerned about?” I would say that from an income tax perspective, there’s not much you can do today that we can’t do in the middle of November or early December.

We will have strategies to consider, depending upon the outcome of the election. As soon as that election occurs, based on the results, we will be in close communication with you.

Regardless of what happens in the election, Shawn & I are going to make sure that we are communicating with you. We will be able to drill down and figure out what you should potentially be doing before the end of the year. And of course, we will communicate that. That’s part of our service to you, to make sure you are up to date on the latest key tax changes.

Still Have Questions?

Regardless of who wins, you need a plan for your money now more than ever. Whether the markets face risks from the election, COVID-19, or international issues, sticking to a long-term plan built on your goals and your life circumstances will help you mitigate risk and stay level-headed in times of uncertainty. If you want to know more about how to set up your money to succeed no matter what happens in the election, call our office at 770-552-5968 or email [email protected]. Or, if you prefer, you can simply click here to schedule an appointment online.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional.

_________________