By Matthew Gaude & Shawn McGuire

Federal Reserve officials at their June 12th/13th meeting indicated that inflation is moving in the right direction but not quickly enough for them to lower interest rates.

“Participants affirmed that additional favorable data were required to give them greater confidence that inflation was moving sustainably toward 2 percent,” according to the June meeting notes. To summarize the June Federal Reserve meeting:

- Inflation has eased substantially but remains too high.

- The Fed reasserts long-term inflation target of 2% but does not see 2% inflation this year or in 2025.

- Strong pace of immigration has boosted labor market participation.

- The Fed says the unemployment rate remains low.

- Economic outlook is uncertain and the Fed is attentive to risks, mentioning that the budget deficit is very large and unsustainable.

- The Fed needs greater confidence that inflation is headed to 2%. Moving too fast creates risk of inflation returning.

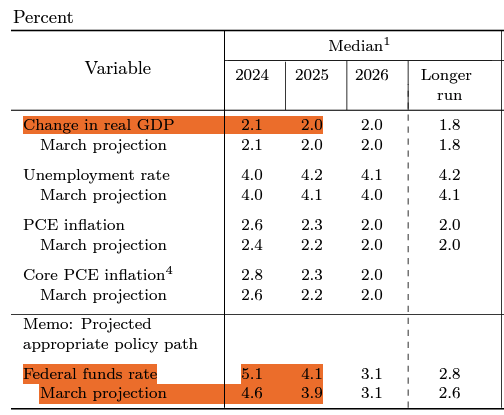

As part of the Federal Reserve’s quarterly economic projections:

- Federal Reserve officials raised their 2024 inflation forecast from 2.4% to 2.6%.

- Median forecast of officials shows just one rate cut in 2024.

- Median forecast shows 1% of interest rate cuts in 2025. This is an increase from .75% of cuts in 2025.

Takeaways

We believe the biggest takeaway is that data is more important than the Fed (at least for the foreseeable future). Throughout 2024, we and others have stressed that economic data will be more important than Fed speak or even Fed policy, and that was proven out as a cooler-than-expected Consumer Price Index (CPI) report. More broadly, the bullish mantra for stocks in 2024 has been 1) stable growth, 2) ongoing disinflation, 3) sooner-than-later Fed rate cuts, and 4) artificial intelligence enthusiasm; and three of those four were reinforced.

During the press conference, Jay Powell mentioned that growth is slowing. Powell mentioned it several times, and while the data is still showing solid activity, the bottom line is that the Fed is no longer just focused on inflation but on inflation and growth. If the Fed is going to cut rates sooner rather than later, it likely will be in response to slowing growth—and that’s usually not a good sign for stocks. Bottom line, inflation is continuing to cool and the Fed will likely cut rates in the coming months. That’s been assumed all year, and that assumption has powered stocks to current new highs. But it’s also becoming clear that growth is starting to slow; and I’ve said this before and will keep saying it: the biggest question for this market isn’t “When will the Fed cut?” or “Is inflation falling?”

In our May 6th interest rate update, we discussed the slowing of consumer spending in certain discretionary areas such as restaurants, Home Depot, and consumer staples companies such as Mondelez, Clorox, and Colgate Palmolive. We can add two more companies that reported disappointing earnings as a result of reduced consumer spending: Nike and Walgreens.

As we enter second quarter earnings, I believe we will continue to see more of these types of earnings announcements.

As a result, the 10-year Treasury rate ticked down from 4.70% on April 25th to 4.28% as of 7/9/2024.

What Does This Mean for Our Fixed-Income Investment Strategy?

The first part of our strategy has been buying 3-month, 4-month, and 6-month T-Bills. Short-term rates have held relatively steady and will until the Federal Reserve starts to cut interest rates. At one point last year, we were able to get over 5.50% annualized interest on a 6-month T-Bill. Now the 6-month T-Bill is at 5.28%. As T-Bills are redeemed, we are now re-investing in 3-month T-bills. Short-term rates will not be going lower immediately, however, will be dependent on when the Federal Reserve cuts interest rates, which we believe could be at their September meeting. T-Bills and money markets have been the fixed-income investment of 2023 for risk-free money and continues to be with over $6 trillion in money markets and cash equivalents. This will change, but not overnight. Risk-free rates over 5% are still attractive.

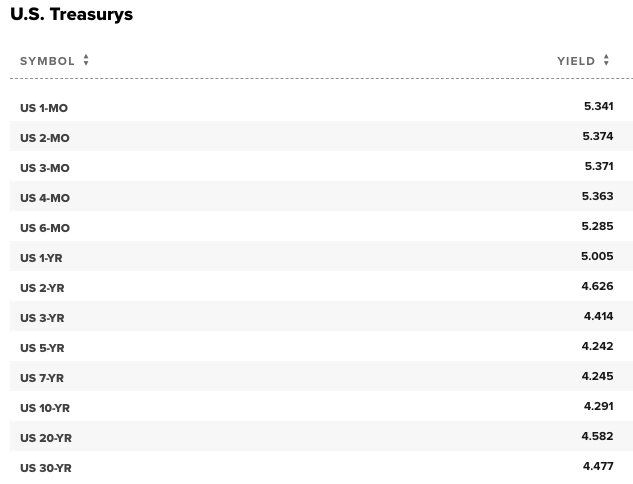

Following are interest rates as of 7/9/2024. There has been very little change in short-term Treasury rates as the 3-month and 4-month have been around the 5.36%-5.40% while longer duration rates have slightly decreased.

Secondly, intermediate-term (12 month) bonds: Since 2022, we have been purchasing high-quality bonds from banks such as J.P. Morgan, Wells Fargo, Bank of America, Citigroup, and Royal Bank of Canada. Unfortunately, there are very few quality bonds being issued currently. To date, there has only been one quality bond issued, an 18-month corporate bond issued by Bank of America paying 5.55%. As these bonds mature, we are reinvesting in our core bond funds as well as several new fixed-income funds and ETFs we have purchased.

Opportunities in Fixed Income

I want to revisit some insights from Howard Marks, co-chairman of Oaktree Capital, an alternative asset management firm with over $172 billion in assets, specializing in fixed income and credit markets. Below we highlight some of Howard’s comments in his “Sea Change” memo he wrote in December 2022:

The overall period from 2009 through 2021 (with the exception of a few months in 2020) was one in which optimism prevailed among investors and worry was minimal. Low inflation allowed central bankers to maintain generous monetary policies. These were golden times for corporations and asset owners thanks to good economic growth, cheap and easily accessible capital, and freedom from distress. This was an asset owner’s market and a borrower’s market. With the risk-free rate at zero, fear of loss absent, and people eager to make risky investments, it was a frustrating period for lenders and bargain hunters.

Of course, all of the above flipped in the last year or so. Most importantly, inflation began to rear its head in early 2021, when our emergence from isolation permitted too much money (savings amassed by people shut in at home, including distributions from massive COVID-19 relief programs) to chase too few goods and services (with supply hampered by the uneven restart of manufacturing and transportation).

How has this change manifested itself in investment options? Here’s one example: In the low-return world of just one year ago, high-yield bonds offered yields of 4-5%. A lot of issuance was at yields in the 3% range, and at least one new bond came to the market with a 2%+ yield. The usefulness of these bonds for institutions needing returns of 6 or 7% was quite limited. Today these securities yield roughly 8%, meaning even after allowing for some defaults, they’re likely to deliver equity-like returns, sourced from contractual cash flows on public securities. Credit instruments of all kinds are potentially poised to deliver performance that can help investors accomplish their goals.

We’ve gone from the low-return world of 2009-21 to a full-return world, and it may become more so in the near term. Investors can now potentially get solid returns from credit instruments, meaning they no longer have to rely as heavily on riskier investments to achieve their overall return targets. Lenders and bargain hunters face much better prospects in this changed environment than they did in 2009-21. And importantly, if you grant that the environment is and may continue to be very different from what it was over the last 13 years—and most of the last 40 years—it should follow that the investment strategies that worked best over those periods may not be the ones that outperform in the years ahead.

In October 2023, Howard Marks wrote a “Further Thoughts on Sea Change” memo. A few nuggets from this memo:

Please note, as mentioned earlier, that I’m absolutely not saying interest rates are going back to the high levels from which they’ve come. I have no reason to believe that the recession most people believe lies ahead will be severe or long-lasting. And with valuations high, but not terribly so, I don’t think a stock market collapse can reasonably be predicted. This isn’t a call for dramatically increased defensiveness. Mostly I’m just talking about a reallocation of capital, away from ownership and leverage and toward lending.

This isn’t a song I’ve sung often over the course of my career. This is the first sea change I’ve remarked on and one of the few calls I’ve made for substantially increasing investment in credit. But the bottom line I keep going back to is that credit investors can access returns today that:

- Are highly competitive versus the historical returns on equities,

- Exceed many investors’ required returns or actuarial assumptions, and

- Are much less uncertain than equity returns.

Unless there are serious holes in my logic, I believe significant reallocation of capital toward credit is warranted.

We share Howard’s thoughts to explain why we are able to get greater total returns from fixed income than we have in over two decades and another reason why we have started to shift funds that are maturing from T-Bills into our core bond funds and other fixed-income ETFs. This leads me to provide an update as to the yields we are currently receiving from our fixed income investments:

- Leader Capital High Quality Income Fund: Yielding 6.45%

- Allspring Short-Term High Income Fund: 5.31%

- Leader Short-Term High Yield Bond Fund: 10.71%

- Fidelity Floating Rate High Income Fund: 8.37%

- Fidelity Capital & Income Fund: 5.68%

- Janus Henderson Collateralized Loan Obligations (CLO) BBB ETF: 8.28%

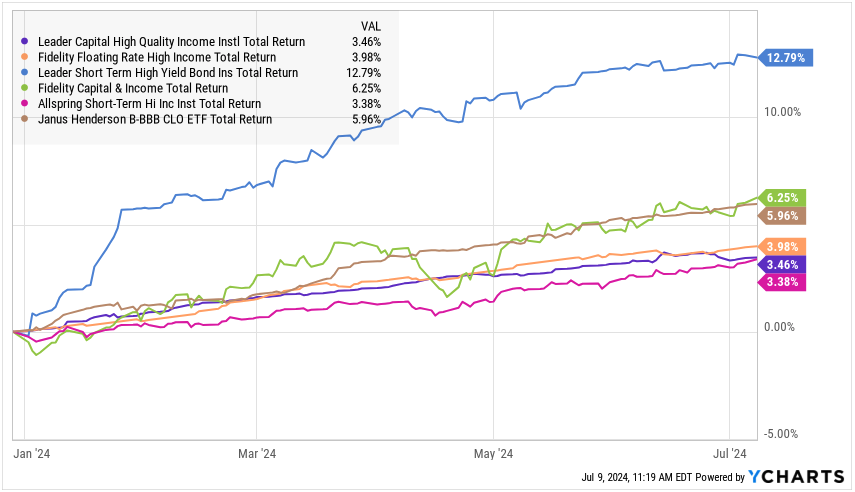

From a total return perspective (dividends plus capital appreciation), following are total returns from January 1, 2024–July 8, 2024:

John Lekas, the manager for the Leader Capital High Quality Income fund, was recently interviewed by Barron’s in an article titled “Where to Find Higher Yields Than Cash While Keeping Your Risk Low.” From the article:

One standout is Leader Capital High Quality Income (LCATX). Morningstar dings it for high expenses, but it is up 13% in the past year—when it was about 92% in high-quality CLOs—compared with 4% for other intermediate core-plus bond funds. “The CLO market can be a little tricky,” says portfolio manager John Lekas. “But once you get to A or better, it gets a lot simpler.” He recently moved about 15% of assets into Treasuries, which will rise in value if interest rates fall. “We need to participate in that,” he says. He’s also lately bought some high-quality floating-rate commercial real estate paper. He believes the beleaguered sector is near a bottom.

The funds mentioned above comprise the third part of our three-pronged strategy.

We’re Here for You

Do you have questions about our strategy or your portfolio? If you would like to set up a review, you can simply click here to schedule an appointment online.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.