By Matthew Gaude & Shawn McGuire

In January, we received several inflation reports that indicated inflation is not coming down as fast as analysts and economists had expected in 2024.

Following are some headlines from The Wall Street Journal and CNBC.com summarizing the inflation results:

The Consumer Price Index (the price of a weighted average market basket of consumer goods and services purchased by households) rose 0.3% in January and 3.1% year-over-year. Both readings were higher than the respective forecasts of 0.2% and 2.9%.

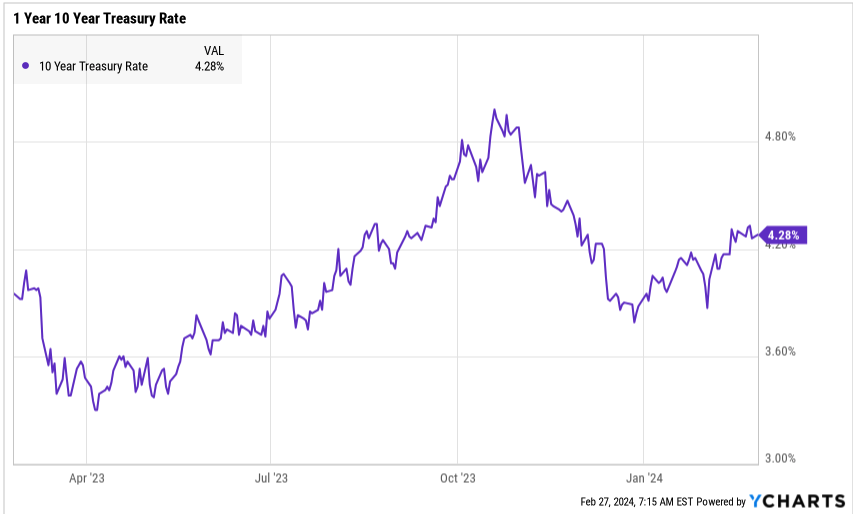

Although these numbers do show inflation has come down from over 9% in June 2022, it has remained persistent. The 3.1% headline inflation number was the lowest reading since last June. While inflation has indeed fallen sharply, it’s looking like it will be difficult to get the last 1 to 2 percentage points of inflation out of the system to reach the Fed’s target of 2%. And that means fewer rate cuts coming this year. As a result, the 10-year Treasury rate ticked up to 4.28% from a low of 3.79% on 12/27/23.

But for Wall Street, which refuses to take the Fed at its word about the timing and scope of rate cuts, this is bad news. Any inflation readings that come in on the high side give the Fed more reason to go slow with rate cuts.

From The Wall Street Journal:

…Bond yields rose after the release, which fueled worries that firmer-than-expected inflation would reduce the probability of the Federal Reserve lowering interest rates in the coming months.

Interest-rate futures, which before Tuesday’s report implied the central bank would probably begin cutting rates by its May meeting, now suggest a June start date is more likely.

As we entered 2024, the bond market was expecting the Federal Reserve to cut interest rates 6-7 times this year. As each inflation report has been released, the odds of rate cuts have continued to decrease to the current expectation of 3 rate cuts, which is the number of interest rate cuts the Federal Reserve estimated in their December economic updates. Remember, back in December, Wall Street put 90% odds on the Fed beginning to cut rates in March. And here we are now, adjusting to a new “probably in June” outlook.

The Federal Reserve held their first meeting of 2024 on January 30th-31st. During Federal Reserve Chairman Jay Powell’s Q&A and statement from their meeting, they updated their policy stance to the following:

- The Federal Reserve sent a tepid signal that it is done raising interest rates but made it clear that it is not ready to start cutting.

- The Federal Open Market Committee removed language that had indicated a willingness to keep raising interest rates until inflation had been brought under control and was on its way toward the Fed’s 2% inflation goal.

- However, it also said there are no plans yet to cut rates with inflation still running above the central bank’s target.

Additional comments from Fed Chair Jay Powell in his news conference included the following:

- Powell said policymakers are waiting to see additional data to verify that the trends are continuing. He also noted that a March rate cut is unlikely.

- “I don’t think it’s likely that the committee will reach a level of confidence by the time of the March meeting.” Powell added, “We want to see more good data. It’s not that we’re looking for better data, we’re looking for a continuation of the good data we’ve been seeing.”

Bottom Line

Although these reports show that inflation is still declining, the market was expecting more and the market reaction was clearly disappointing. As Treasury yields surged to a multi-month high, stocks dropped sharply in response, and investors dropped rate cut expectations for the May Federal Reserve meeting.

We believe the Federal Reserve will still cut interest rates, however, probably not until sometime in the second half of 2024 (so now June vs. May). The key distinction with last week’s CPI and PPI was this: The data showed inflation was still falling, but more slowly than expected. For inflation data to be strong enough to challenge the bullish momentum, it has to imply inflation has stopped falling and is rising again, because that will challenge the idea of any rate cuts in the near term.

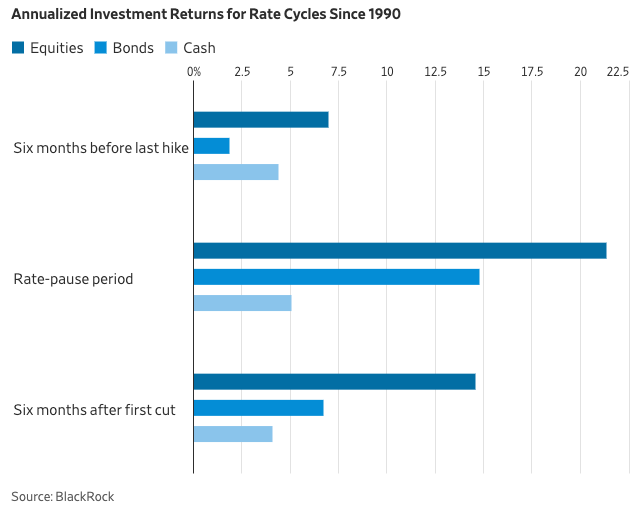

Stocks and bonds both tend to perform better in a pause before rate cuts than after, according to an analysis from BlackRock. Since 1990, stocks purchased in the six months after the first rate cut in a cycle have returned an annualized average of 15%, compared with a 21% return for investments made during the pause. Bonds returned an average 15% in the pause before the cuts and 7% afterward.

Strategy Significance

What does this mean for our fixed-income investment strategy?

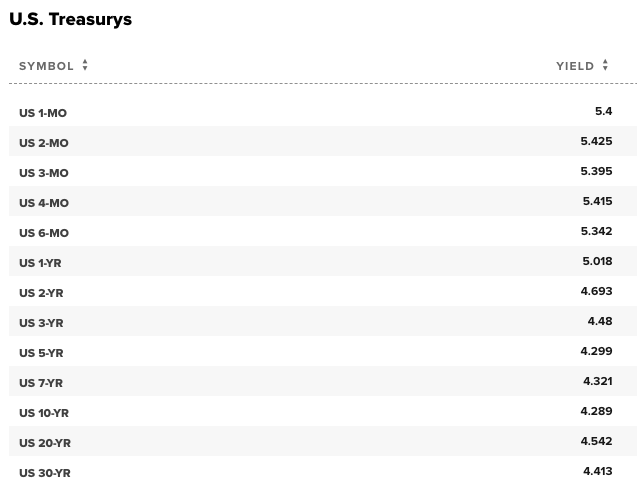

- The first part of our strategy has been buying 3-month, 4-month, and 6-month T-Bills. Short-term rates have held relatively steady and will until the Federal Reserve starts to cut interest rates. At one point last year, we were able to get over 5.50% annualized interest on a 6-month T-Bill. Now the 6-month T-Bill is at 5.34% (rates are from CNBC.com on 2/27/24). Our strategy has been when T-Bills are redeemed, we have been able to reinvest at the same to higher rates than before. We may not have that chance anymore. We knew this opportunity would not last forever, however, we wanted to take advantage while we could. Short-term rates will not be going lower immediately, but will be dependent on when the Federal Reserve cuts interest rates. T-Bills and money markets have been the fixed-income investment of 2023 for risk-free money and continue to be with over $6 trillion in money markets and cash equivalents. This will change, but not overnight. Risk-free rates at 5% are still attractive, which allows us to continue reinvesting in 3-, 4-, and 6-month T-Bills until the Federal Reserve lowers interest rates below the 5% threshold.

Following are interest rates as of 2/27/2024:

2. Intermediate-term (12-month) bonds: Since 2022, we have been purchasing high-quality bonds from banks such as JPMorgan, Wells Fargo, Bank of America, Citigroup, and Royal Bank of Canada. When we first started buying bonds toward the end of 2022, we were receiving 4.50% on a Royal Bank of Canada bond that matured on 11/20/2023. We have seen interest rates come down from the 5.7% JPMorgan 12-month corporate bond that was issued several months ago. Unfortunately, there are very few quality bonds being issued currently. As these bonds mature, we are reinvesting in our core bond funds as well as several new fixed-income funds we have purchased.

3. The third part of our three-pronged strategy has been our Leader High Quality Income Fund, and our Allspring Short-Term High Income Fund. Part of our core fixed-income portfolio, they have performed very well.

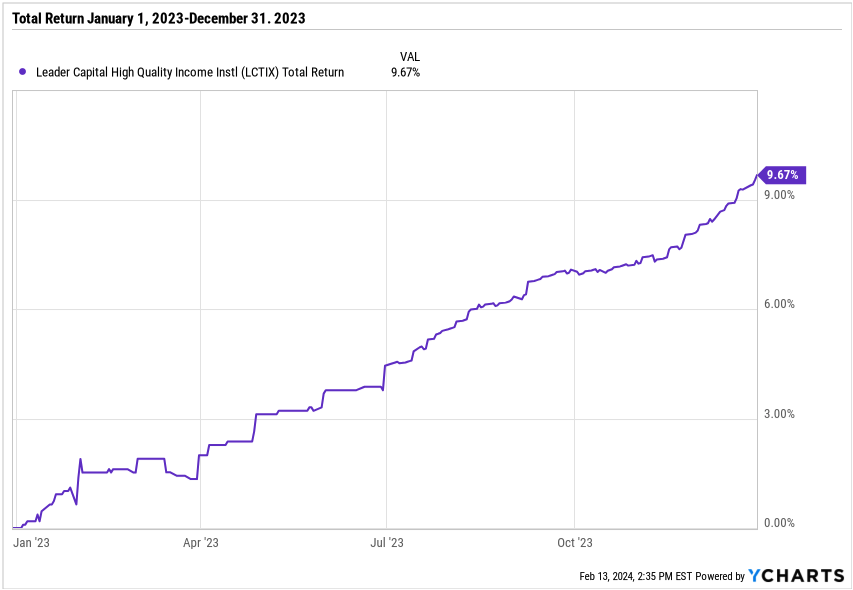

Let me take a minute and update you on our 2 core bond funds. The first is the Leader High Quality Income Fund. The fund is currently yielding 6.81% as of 1/31/2024. Following is a chart of the total return of the fund for 2023. Total return means capital appreciation plus dividends received during the year. The total return for the Leader High Quality Income Fund for 2023 was 9.67%. This is the type of investment we strive to find for you—an investment with low volatility and consistently increasing throughout the year. This is one reason why the fund continues to be ranked #1 in their bond category. I just wish we could find more investments like this.

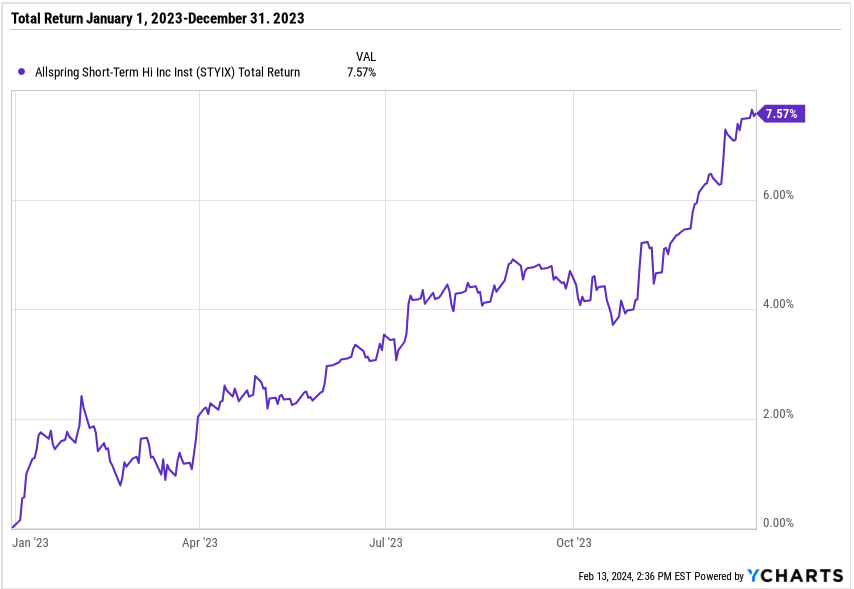

The second fund is the Allspring Short-Term High Income Fund currently yielding 6.17%. As you can see, the total return in 2023 was 7.57%, inclusive of dividends and capital appreciation. We saw the fund start to pick up performance in November when the market started to anticipate that the Federal Reserve would soon “pivot” from raising interest rates, to pausing and then eventually starting to lower rates in 2024, which the Fed did confirm during their December meeting.

We are very happy with the performance of both the Leader High Quality Income Fund and the Allspring Short-Term High Income Fund. This is a good time for us to reiterate our position on the Federal Reserve lowering interest rates. We have been of the opinion that inflation could be around longer and take more time to get to a level that makes the Federal Reserve comfortable to start to lower interest rates, meaning rates stay higher for longer.

In the Meantime…

We will continue to eagerly earn higher rates of interest at current levels. Now for a short bond lesson. There is an inverse relationship between bond prices and interest rates. As interest rates go lower, bond prices go higher, and vice versa. So, although we will be earning less interest, bond prices will go up, thus increasing the value of the bonds in our funds. If you go back to the Allspring Short-Term High Income Fund chart above and look at the time period from October-December 2023 when interest rates declined from 5% to 3.79% on the 10-year Treasury, this is an example of when interest rates declined substantially, thus increasing bond prices and the effect on returns.

We have also added some additional bond funds to your account, which we will discuss in more detail with you during our meetings. In the meantime, if you would like to set up a review, you can simply click here to schedule an appointment online.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.