By Matthew Gaude & Shawn McGuire

As the bond markets entered November, we have seen an extraordinary decline in interest rates, over 100 basis points (or 1%), which is a big move in a very short period of time. Following is a chart of the 10-Year Treasury Bond showing where it briefly hit 5% on October 19th and has declined to below 4% as of today!

Following is a chart of the 6-month T-Bill, where yields topped out at 5.60% on October 17th and declined to 5.33% as of December 13th, 2023.

This decline in interest rates has been driven by investors pricing in a lot of Fed rate cuts in 2024. Importantly, that expectation for the Federal Reserve to cut interest rates comes despite: 1) The Fed directly pushing back on the idea of near-term rate cuts as late as December 1st and 2) Economic data that doesn’t yet support cuts, meaning inflation is still too high. Following is a CNBC headline from December 1st:

During a speech Federal Reserve Chairman Jay Powell gave at Spelman College on December 1, 2023, Powell mentioned, “It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease. We are prepared to tighten policy further if it becomes appropriate to do so.” Powell also noted that policy is “well into restrictive territory” and that the balance of risks between doing too much or too little on inflation are close to balanced now. However, the remarks gave some credence to the idea that the Fed at least is done hiking as the string of rate hikes since March 2022 have cut into economic activity. Powell noted that inflation “is moving in the right direction.”

Prior to the Federal Reserve meeting on December 13th, investors believe the Federal Reserve will lower the fed funds rate from today’s 5.25-5.50% to 4.00-4.25% or 4.25-4.50% by year-end 2024. That’s four to five rate cuts next year. We see it priced into the big drop in Treasury yields, as illustrated above, and action in fed funds futures. That’s a significant shift from just a few weeks ago when “higher for longer” was all the rage. The only question is will the Federal Reserve start lowering rates in March or May?

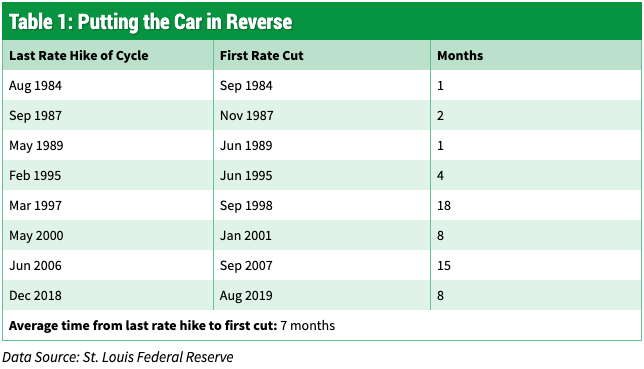

Economic growth is finally slowing down, and the Fed is “proceeding carefully.” Investors are currently projecting rate cuts could begin as soon as March 2024. What does history tell us? Following is a chart showing the average time from the last rate hike to the first rate cut:

December 13th, 2023, Federal Reserve Meeting

Some of the questions may have been answered as a result of the December 13th Federal Reserve meeting with the following headline:

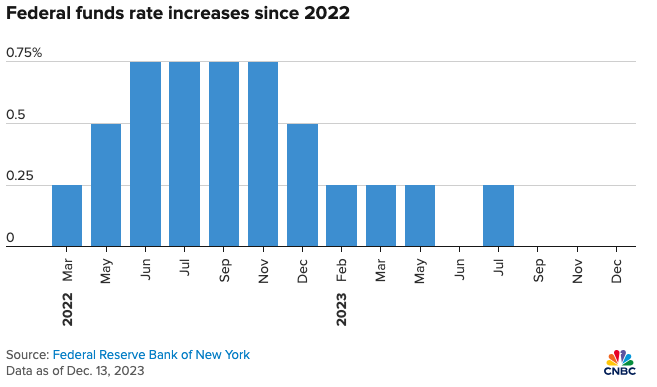

This is the headline from www.cnbc.com on December 13th, after the Federal Reserve meeting. Following their two-day meeting, the Federal Reserve decided to not raise interest rates this month. This was the third consecutive meeting the Federal Reserve chose to hold rates steady, following a string of 11 rate hikes, including four in 2023 (as seen in the chart below). The Federal Reserve kept interest rates at 5.25%.

The Fed surprised investors by making a dramatic and blatant dovish shift as it abandoned the “higher for longer” mantra of the past several months and instead 1) Signaled three rate cuts in 2024, 2) Clearly told markets rate hikes are over, and 3) Admitted that rate cuts were discussed at the meeting. So, was the dovish Fed decision a bullish game-changer? In the short term, yes. In the longer term, no. In the short term, the dovish Fed decision will put further pressure on Treasury yields and assuming there is no surprise bounce back in inflation nor any sudden collapse in growth (both of which are very unlikely until at least mid-January at the earliest), there’s nothing to stop this short-term rally.

However, beyond the short term (basically the next month), the outlook becomes more mixed for two reasons. First, the expectation gap between what the Fed says will happen (three cuts) and what the market expects (six to eight cuts) remains wide, which will leave the market vulnerable to a hawkish (bearish) surprise in the new year. Second, the dovish Fed decision still doesn’t address the major question facing markets that likely will define performance in 2024: Is the economy just seeing a mild slowing of activity or is this the start of a real, larger-than-expected slowdown? If it’s the former, then the dovish stance by the Fed and anticipated rate cuts will likely spur a rally in stocks through 4,900-5,000 in the S&P 500 in 2024. However, if it’s the latter and the economy is truly starting to slow, then the euphoria over a dovish pivot by the Fed yesterday will be misguided because the Fed will be too late and markets will have to acknowledge a real economic slowdown. Bottom line, the Fed’s dovish surprise does support the November/December gains. And it clears the path for a potential melt-up into year-end (and partially beyond) as long as we don’t get any upside surprises on inflation and/or growth. However, the dovish Fed does not address the major issue facing markets in 2024: Does growth slow a lot or a little?

Turning to the press conference, Powell did nothing to push back on the idea of rate cuts in early 2024, and even admitted (purposefully or not) that rate cuts were discussed at the meeting, yet another dovish development. Bottom line, the press conference simply added to the shockingly dovish surprise from the Fed yesterday, as Powell has done a 180-degree turn from the “higher for longer” and “not ready for rate cuts” commentary of the past few months.

It seems the Federal Reserve has moved closer to the bond market’s expectations of interest rate cuts in 2024 and beyond. December’s new Summary of Economic Projections released December 13th; the Federal Reserve didn’t change short-term interest rates today, but it made major changes to its projections for short-term interest rates. Not one policymaker on the Federal Open Market Committee thinks the short-term interest rate target will be higher a year from now than it is today (5.375%). And while the median forecast from policymakers in September was one rate cut of 25 basis points in 2024, now the median projection is 75 bps. In turn, the median policymaker projects another 100 bps in rate cuts in 2025 and then another 75 bps in 2026.

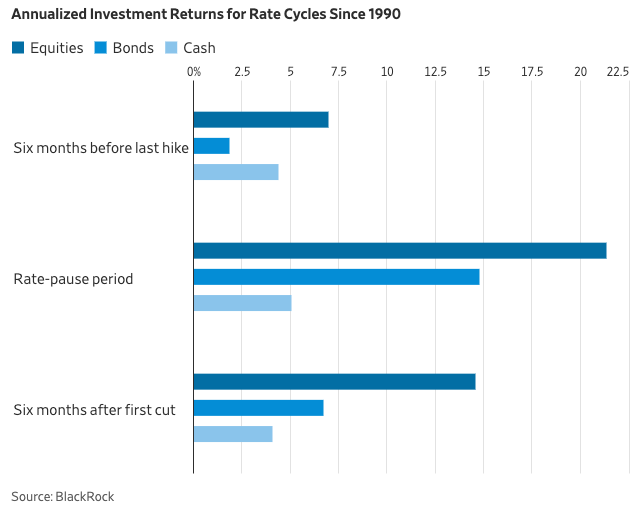

Stocks and bonds both tend to perform better in a pause before rate cuts than after, according to an analysis from BlackRock. Since 1990, stocks purchased in the six months after the first rate cut in a cycle have returned an annualized average of 15%, compared with a 21% return for investments made during the pause. Bonds returned an average 15% in the pause before the cuts, and 7% afterward.

How Many Rate Cuts in 2024 Will the Federal Reserve Make?

Will the bond market continue to price in even more interest rate cuts in 2024? In recent weeks, as expectations for a soft landing in 2024 have intensified, Wall Street has ramped up expectations on the timing and scope of rate cuts next year.

Importantly, we wanted to make sure we understood just how big the gap is between what the Fed says will happen with rates and what the market expects. To keep things simple, prior to today’s Federal Reserve meeting, the Fed was telling us there will be two rate cuts next year. The market was expecting a minimum of four, and possibly six or seven. This matters because how much the Fed “moves” toward the market expectations via the statement will determine if the FOMC decision is positive or negative for stocks. As a result of the projected rate cuts and inflation slowly decreasing, the stock and bond markets took the news as very bullish.

What does this mean for our fixed-income investment strategy?

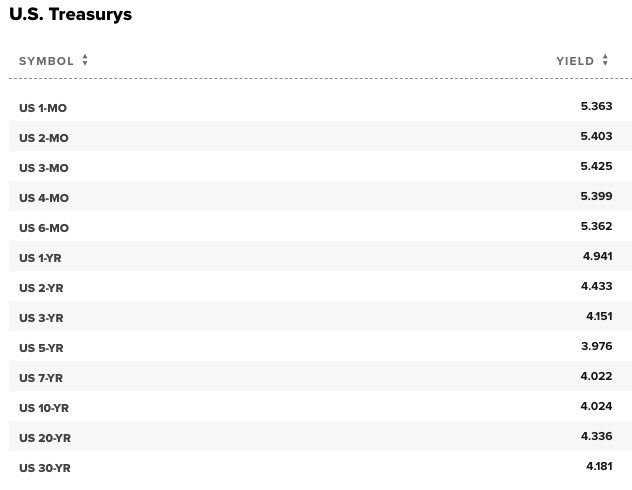

1. The first part of our strategy has been buying 3-month, 4-month, and 6-month T-Bills. The chart below shows rates from CNBC.com on 11/7/23. Below the chart is a comparison of interest rates as of 12/13/23. You can see the difference in interest rates when at one point we were able to get over 5.50% annualized interest on a 6-month T-Bill. Now the 6-month T-Bill is at 5.34%. Our strategy has been when T-Bills are redeemed, we have been able to reinvest at the same to higher rates than before. We may not have that chance anymore. We knew this opportunity would not last forever, however, we wanted to take advantage while we could. Short-term rates will not be going lower immediately, but will be dependent on when the Federal Reserve cuts interest rates. T-Bills and money markets have been the fixed-income investment of the year for risk-free money. This will change, but not overnight. Risk-free rates at 5% are still attractive, which allows us to continue reinvesting in 3-month, 4-month, and 6-month T-Bills until the Federal Reserve lowers interest rates below the 5% threshold. Check out The Wall Street Journal’s December 13th article titled “Money Moves to Make If You’re Expecting the Fed to Lower Interest Rates.”

The following are interest rates as of 12/13/2023:

2. Intermediate-term (12 month) bonds. Since 2022, we have been purchasing high-quality bonds from banks such as JPMorgan, Wells Fargo, Bank of America, Citigroup, and Royal Bank of Canada. When we first started buying bonds toward the end of 2022, we were receiving 4.50% on a Royal Bank of Canada bond that matured on 11/20/2023. We have seen interest rates come down slightly from the 5.7% JPMorgan 12-month corporate bond that was issued several months ago. Unfortunately, there are very few quality bonds being issued currently. Those that are being issued are 2-3 years in duration, which we are looking at more closely for the potential to lock in higher yields over a 24-to-36-month time period.

3. The third part of our three-pronged strategy has been our Leader High Quality Income Fund, which is currently paying 7.07%, and our Allspring Short-Term High Income fund paying 6.76%. They have been part of our core fixed-income portfolio and have performed very well. We will continue to hold.

4. A fourth area is preferred stocks. There have been fantastic opportunities over the last 6-8 months to purchase preferred stocks at steep discounts to par value. With the massive decline in interest rates over the last 45 days, we have seen the discounts move closer to par value, and in some cases, we have sold some positions that are no longer bargains, realizing gains. It is harder to find high-quality preferreds trading at large discounts, which makes this market more opportunistic.

In our last update on November 7th, we mentioned “we have mostly been focusing on purchasing shorter duration, 3 months-6 months when purchasing T-Bills. Due to the softening of the economy in several key areas as well as tightening financial conditions, we will be extending our purchases to slightly longer term, potentially up to 2 years. We are also seeing interest rates on fixed products such as fixed annuities and multi-year guaranteed annuities in the 5.95% to 6.15% for 3-5 years.” Since then, we have extended duration to high-quality corporate bonds with maturities ranging between 1-5 years. We have also seen insurance companies lower the interest rates they are offering on the multi-year guaranteed annuities from 6.15% for 5 years to ~ 5.50%.

We knew the time would come during this interest rate cycle when the Federal Reserve would start lowering interest rates, which would make shorter-term T-Bills less attractive as well as money market rates. We believe interest rates based on the 10-year Treasury Bond will eventually decline to below 3%, possibly even as low as 2.80% over the next 12-18 months. Contrary to what we have experienced over the last 45 days with the massive decline in interest rates, the continued decline will not happen overnight. Based on the growth of the economy and inflation, we will see spikes in interest rates, which is when we will become more opportunistic in the various fixed-income areas.

Do you have questions about your finances as we head into 2024? The Live Oak Wealth Management team is here to assist. If you would like to set up a review, simply click here to schedule an appointment online.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.