By Shawn McGuire & Matthew Gaude

It’s hard to open up a newspaper these days and not see a scary story about the debt ceiling debate. The Biden Administration is saying that a “default” is approaching if an agreement isn’t reached soon. The fight over the debt ceiling in Washington is a game of chicken with politicians behind the wheel.

Neither side wants to crash the economy by triggering a default on U.S. government debt. But each side wants the other to jump first. Only this time, the injured party could be the U.S. economy…U.S. stock and bond markets. So let’s look at how the debt ceiling fight could end in tragedy, what it means for your portfolio, and what steps we are taking if politicians drive the economy off a cliff.

The Debt Ceiling Is a Quirk of History

Before 1917, the debt ceiling didn’t exist; up to that point, Congress had complete authority over each new bond the Treasury issued. But to give the Treasury more leeway, and help fund America’s involvement in World War I, Congress allowed the Treasury to issue bonds at its discretion providing it didn’t breach a pre-agreed limit—or ceiling—on the total debt.

And this ceiling doesn’t automatically go up as Congress approves new spending. It must vote to raise it. That gives Congress the power to force the government to roll back its spending commitments.

And if Congress doesn’t approve a higher debt ceiling, the federal government has no choice but to default on its debt. Tax receipts alone aren’t enough to cover its spending commitments plus the interest payments on the debt. Congress has never gone through with its threat and refused to raise the debt ceiling. So, most folks think it won’t happen this time either.

They could be right. But there are reasons to worry that this time may be different. (1)

What Happens if There’s No Debt Ceiling Deal?

The first high-level meeting between Republican leaders and President Biden yielded no progress on the debt ceiling, and with potentially just three weeks until the “X” date (the date at which the Treasury hits the debt ceiling), there are concerns and questions about what might happen if there’s no deal? Given that, I wanted to provide a brief analysis of:

1) What a default might practically mean, and

2) What it could do to various asset prices.

More specifically, a day has not passed that we have not read or heard a lot of general, hyperbolic statements about what a default would mean for markets and the economy, with warnings of calamity, and catastrophe, etc. While those comments are effective in generating attention, they don’t do much to tell us what actually might happen, so the purpose of this analysis is also to be specific and explain what we think would occur in the event of a debt ceiling breach. Much of the basis of this analysis is based on the last debt ceiling drama in 2011.

What Happens if There’s No Debt Ceiling Deal?

First, there is an important difference between hitting the debt ceiling and the U.S. defaulting. Practically speaking, the debt ceiling prevents the Treasury Department from selling additional Treasury debt. That’s a problem because regular sales of Treasuries are how the U.S. government funds its day-to-day operations. However, if the debt ceiling is hit and the Treasury Department can’t sell additional Treasuries, it does not mean the U.S. is bankrupt or in default. What it does mean, is that the Treasury Department then has to “ration” its existing cash and decide whom to pay, and whom not to pay. So, the Treasury could pay interest on existing Treasury debt, soldiers’ salaries, Social Security, and not pay federal workers’ salaries and federal contractors (this is just a theoretical example). The important point is this: hitting the debt ceiling doesn’t mean the U.S. automatically defaults on its debt. But it does mean it’ll have to direct cash to essential services and payments and not pay “less essential” services. This matters because it’d create a huge headwind for economic growth and make a hard landing more likely.

First, the general uncertainty of the Treasury restricting payments would be a headwind on economic activity. Second, the delay of a paycheck from the federal government to workers, contractors, etc., would cause an even bigger headwind on economic growth. This is the practical negative for the U.S. hitting the debt ceiling, and it would be more than just general uncertainty weighing on the economy.

What happens to asset prices if there’s no debt ceiling deal? Fortunately, we have a blueprint for what to expect from this debt ceiling drama, because we had a very similar episode in 2011.

Flashback to 2011

While we view a default as a low-probability event, headline risk over the next few weeks could weigh on risk sentiment. Unfortunately, the market has also seen this before with a very similar episode in 2011. As a quick summary, a debt ceiling showdown in Washington resulted in the government hitting its debt limit on May 16, 2011. However, the Treasury pulled off some accounting maneuvers to narrowly avert a crisis and fund the government until August 2, exactly how long it took Congress to get a deal done. The damage done during this period included a sizable sell-off across equity markets, lower yield underpinned by a flight to safety, and a credit downgrade of U.S. debt to AA+ from AAA by Standard & Poor’s (S&P) rating agency.

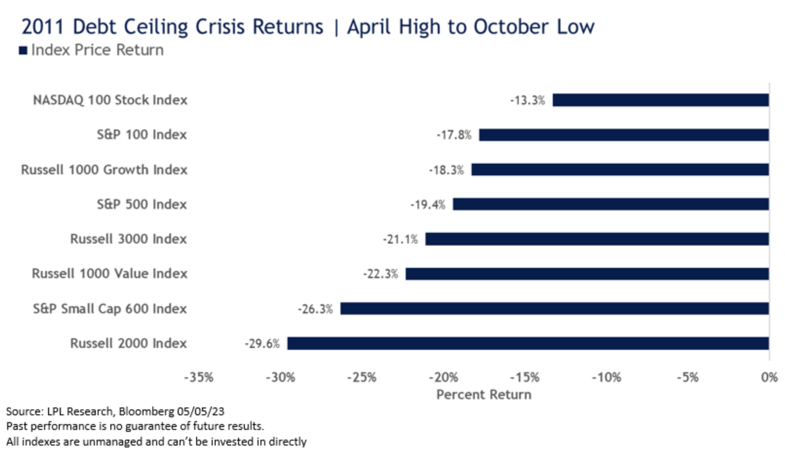

The chart below shows how several major indices performed during this period as illustrated by the market’s April high to the October low. (2)

Broadly speaking, here are the conclusions from the market performance during and after the 2011 debt ceiling drama. First, longer-dated Treasuries performed very well, and if there’s a place to “hide” during the debt ceiling drama, longer-dated Treasuries was it. The 2011 debt ceiling drama really intensified in May 2011, and the 10-year yield was around 3.2%. By the time the U.S. got to the eve of hitting the ceiling (late July/early August), the 10-year yield had declined to 2.7% (meaning the 10-year Treasury rallied). By the market bottom in late October 2011, the 10-year yield had dropped to 1.80%! And if we think about it, this makes sense because regardless of what happens in the next three weeks, no one credibly thinks that interest payments won’t be made on 10-year Treasury debt, nor that this short-term Washington fiasco will materially degrade the creditworthiness of the United States. (3)

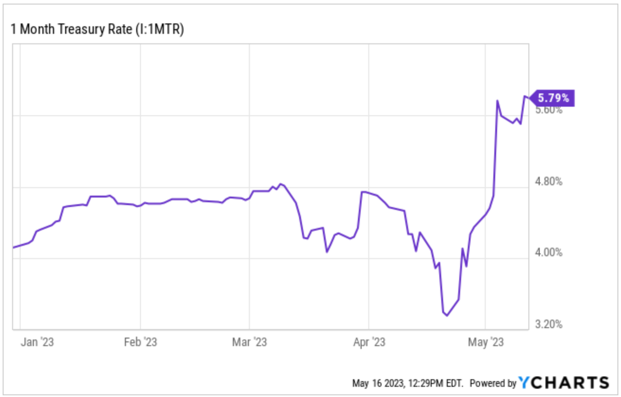

The yield on the one-month Treasury bill has surged on debt ceiling worries. The yield has surged from 3.30% to 5.79% over the last month as investors are demanding a higher yield during the X date.

Essentially, investors are looking at this event as a finite moment in time, almost like a pothole in the road. Yes, if we hit the pothole, it can cause some damage and discomfort, but it won’t derail the entire journey. And bond investors are avoiding this pothole by selling one-month Treasuries (the yield is over 5.7%) and buying longer-dated debt, and we expect that to continue.

Second, stocks do not do well following debt ceiling dramas, even if it’s resolved at the last minute. The S&P 500 fell 6% from May through August 2011 (when the debt ceiling drama really intensified) and dropped another 15% after a debt ceiling extension had been reached. The peak-to-trough decline for the S&P 500 was more than 20% from May through October. Finally, gold was flat over that time. Notably, gold went higher during the height of the debt ceiling drama, as gold rose 20% from early May through mid-August, although it gave back those gains over the remainder of the year. Essentially, gold did prove a useful hedge against debt ceiling uncertainty and likely will again this time. (4)

Bottom line: The debt ceiling headlines will become more intense and scarier in coming weeks, but we wanted this analysis to provide independent, clear, and fact-based coverage of what we can expect from an “events” standpoint if the U.S. hits the debt ceiling (an event that remains unlikely, but not impossible). Additionally, I wanted to provide a clear asset return blueprint so we have an idea of how different assets could perform as we approach the X date and beyond.

We believe the odds of the government defaulting on its debt obligations remain low. However, without a debt ceiling deal, the probabilities of a technical default are not zero and headline risk will remain elevated until a resolution is passed. The fixed-income market continues to price in increased credit risk in U.S. Treasuries as the X date approaches. In the event of a prolonged debt ceiling battle similar to 2011, watch for large caps to outperform small caps, growth to outperform value, and defensive sectors to outperform more cyclical sectors.

Here’s What We Are Doing

- Holding more cash. We may be giving up some yield short-term but we do not have to worry about volatility in short-term fixed income or equities.

- Purchasing 6-month T-Bills yielding 5.226% annualized which mature in November 2023.

- If we do see declines in equities or other markets, we will have the cash to take advantage of these opportunities.

- In our Bear Market Recovery Strategy we released in January, we discussed 4 markets that, based on our research, have outsized opportunities this year. One market is precious metals, gold, and silver. We have been buying the Gold Miners ETF (GDX) and the Silver ETF (SLV) since the beginning of the year. As we saw in 2011, gold increased by ~20% during the debt ceiling negotiations before pulling back the remainder of 2011.

- Buying 12-month corporate bonds yielding between 5%-5.35% from well-entrenched banks such as JPMorgan, Royal Bank of Canada, and Goldman Sachs. These bonds fall outside the concern of a U.S. debt default and could be some of the highest yields to lock in this interest rate cycle.

We will continue to keep you updated. In the meantime, if you have any questions or concerns, please give us a call or click here to schedule a meeting, web meeting, or phone call.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.

____________

(1) https://www.legacyresearch.com/

(2) https://lplresearch.com/2023/05/05/battle-inside-the-beltway/

(3) www.sevensreport.com May 11th newsletter

(4) www.sevensreport.com May 11th newsletter