By Matthew Gaude & Shawn McGuire

On December 29th, 2022, President Biden signed the second iteration of the sweeping retirement act, SECURE Act 2.0 of 2022, into law. Similar to the first version of this bill, it includes over 100 provisions that affect Americans of all income levels. In particular, there are a number of important changes to the rules around saving for retirement. Here’s what you need to know about SECURE 2.0 and how it could affect your retirement planning going forward. Due to the number of changes, we will be providing customized updates to you during our meetings regarding which new regulations will affect you starting in 2023 or in the future.

RMDs Are Changing Again

Perhaps the most significant change in SECURE 2.0 is the update to required minimum distributions. Under the original SECURE Act, the RMD age was increased from 70½ to 72 for taxpayers who have a traditional IRA or other qualified retirement accounts. With the new legislation, however, the RMD age has been increased to 73 for those born between 1951 and 1959. The RMD age will increase again in 2033 to age 75 for those born in 1960 or later. This can provide some much-needed tax relief for retirees who don’t necessarily need to withdraw funds at that age to pay for retirement expenses. It also allows those accounts to stay invested for longer, which can provide a boost to overall retirement savings.

Another notable change to the RMD rules includes a decrease to the steep 50% penalty for missed or late distributions. Starting in 2023, the penalty will drop to 25% of the missed RMD. Additionally, IRA owners will have the ability to reduce this penalty further (to 10%) if they take the RMD and file an amended tax return in a timely fashion.

SECURE 2.0 also changes the rules around RMDs for Roth contributions in employer-sponsored retirement accounts. Starting in 2024, Roth accounts will no longer be subject to the RMD requirement. The act also expands Roth eligibility to SIMPLE and SEP IRAs starting in 2023.

Increased Catch-Up Contributions

The SECURE 2.0 Act provides greater opportunities for retirement savings by increasing catch-up contributions. The most important changes include:

- IRA Catch-Up Contributions Indexed to Inflation: While the base contribution limit to IRAs ($6,500 in 2023) is indexed annually based on inflation, the catch-up amount ($1,000 in 2023) has traditionally been fixed. Starting in 2025, IRA catch-up contributions will be linked to inflation, allowing the contribution limit to increase as the cost of living increases.

- “Special” Catch-Up Contributions for Employees Age 60 to 63: The SECURE 2.0 Act increases catch-up contributions for employees aged 60 to 63 starting in 2025. As of age 50, retirement plan participants are able to make catch-up contributions up to $7,500 for 2023. The new law increases this amount to $10,000 (indexed to inflation) once you reach age 60.

- Roth Catch-Up Contributions Required for Those With Wages Above $145,000: Starting in 2024, employees with wages above $145,000 will be required to make any catch-up contributions to a Roth account, effectively eliminating the current-year deductibility of those contributions.

- Increased Catch-Up Contributions for SIMPLE Plans: In 2024, the catch-up contribution limit for SIMPLE plans (IRA and 401(k)) will increase by 10%. In 2025, the catch-up contributions will be increased to $5,000 (indexed to inflation) for employees aged 60 to 63.

529 Rollovers

Many Americans save for college education through 529 accounts, which allow up to $17,000 in gift-tax-free contributions per year, or $85,000 if the lump-sum election is selected. Contributions grow tax-free as long as they are used for eligible education expenses. If they are used for an unqualified expense, the earnings are taxable and the distribution is subject to a 10% penalty.

This is where rollovers come in. The new SECURE 2.0 provisions allow unused 529 funds to be rolled over into a Roth IRA starting in 2024. There are some strict limitations to this new rule, including:

- There is a lifetime rollover cap of $35,000.

- Rollovers are still subject to the annual Roth contribution limit ($6,500 in 2023), so it may take multiple years to completely roll over the funds.

- The rollover must be made to the 529 beneficiary’s Roth account (typically the student), not the 529 account holder’s Roth (typically the parent).

- The 529 must have been open for at least 15 years.

- Contributions and earnings made in the last 5 years cannot be rolled over.

Other Important Retirement Savings Provisions

The SECURE 2.0 is a wide-ranging law that covers many additional aspects of retirement readiness and overall financial health to help taxpayers better prepare for the future.

As part of this goal, the act expands and creates new opportunities for retirement savings. For instance, employers will now be able to offer employees the choice to receive matching contributions on a Roth or pre-tax basis. Previously matching contributions were always considered pre-tax. If Roth contributions are selected, they will be considered fully vested upon contribution. Though this might take some time for employers and payroll companies to implement, this option will allow employees to choose whether their matching contributions are taxed up front (Roth) or in retirement (traditional).

Employers will also be required to automatically enroll eligible employees in workplace retirement plans at a minimum 3% contribution rate starting in 2025. Retirement accounts will also be automatically portable, meaning account balances will immediately transfer to your new employer’s retirement account if you leave your current job.

Additionally, defined contribution plans will start offering emergency savings accounts for non-highly compensated employees starting in 2024. Contributions are limited to $2,500 per year, but the first four withdrawals per year would not be subject to taxes or penalties.

Also in 2024, employers will be able to match an employee’s student loan payments by contributing a matching amount to their retirement account. This provision provides an extra incentive for student loan borrowers to make payments on their loans, while also helping them save for retirement.

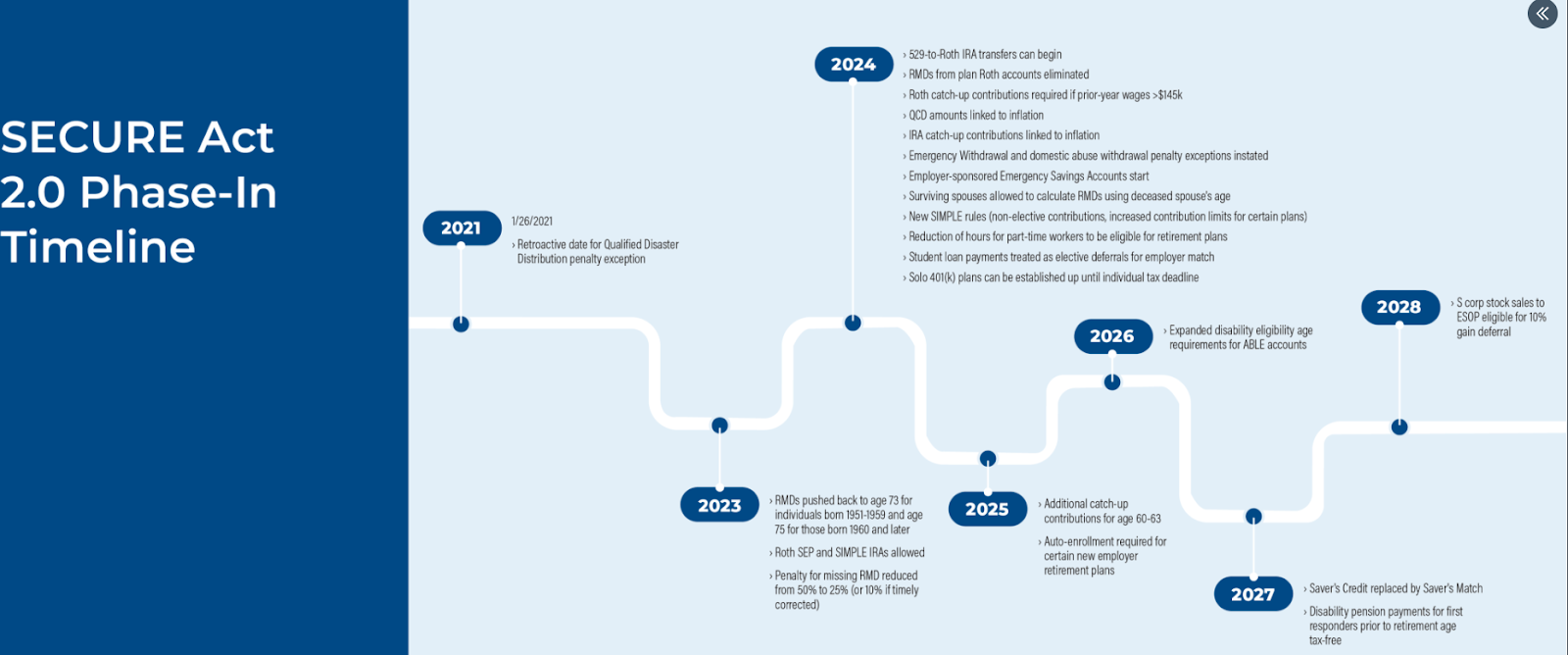

Key Dates to Remember

Many of the biggest provisions will go into effect over the next several years. Use this helpful diagram to keep track of when the changes will take place:

Do You Have Questions About SECURE 2.0?

There’s a lot covered in the new SECURE 2.0 Act of 2022, and this article is not an exhaustive list of all the provisions. Download our Secure Act Hand-out here. If you have questions about how the new rules apply to your situation, we’re here to help. At Live Oak Wealth Management, we can help you navigate the changes and make the most of the new savings opportunities available. To get started, call our office at 770-552-5968 or email [email protected]. Or, if you prefer, you can simply click here to schedule an appointment online.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.