By Matthew Gaude & Shawn McGuire

Thinking about retirement should be exciting and stress-free. But unfortunately, a necessary evil in planning for your golden years includes thinking about the possibility and cost of long-term care (LTC). Since nearly 70% of today’s 65-year-olds are going to need some form of LTC, it’s important to incorporate these costs into your overall retirement plan. To ensure you are well-equipped to retire in Georgia, it’s essential to get a clear understanding of your anticipated needs for LTC.

Cost of Long-Term Care in Georgia

The following data shows average costs based on facilities all over Georgia, so the actual costs of care may vary drastically in your specific location. Additionally, some LTC needs can be fulfilled by family and friends, which means these costs may not be necessary for all retirees depending on the support system of the person who needs care.

Keep in mind that some illnesses, such as Alzheimer’s, will almost always require LTC during the later stages of the disease, no matter how supportive or available loved ones are to help.

Regardless of the situation, it’s worth considering the potential need for LTC as part of your retirement plan. The following table shows the median cost of care in Georgia:

| Type of Care | Monthly Median Cost in 2020 | Monthly Median Cost in 2040 |

| Adult Day Healthcare | $1,355 | $2,447 |

| Home Health Aide | $4,099 | $7,403 |

| Assisted Living Facility | $3,500 | $6,321 |

| Nursing Home: Semi-Private Room | $6,722 | $12,141 |

| Nursing Home: Private Room | $7,173 | $12,955 |

As you can see, costs are projected to increase substantially over the next 20 years. Nursing home care, whether in a semi-private room or private room, may be well above most people’s monthly mortgage payments, which is all the more reason to plan ahead.

Factors That Impact Long-Term Care Costs

When planning for LTC costs, there are a few things to consider in addition to your location. The following factors can impact your costs:

- Type of care needed

- Duration of care

- Time of day care is needed

- The provider you choose

Assisted living facilities have lower costs than nursing homes, and a semi-private room in a nursing home will have a lower cost than a private room. Some facilities may have all-inclusive fees, while others may charge extra for any services beyond the room and food. For home care services, the time of day when care is needed will also impact the cost. Keep in mind that weekends, holidays, and evenings are typically more expensive than weekdays.

So, what can you do to build these costs into your retirement plan?

Two big questions loom as the American population comes of age for long-term care: How do I plan for it? Can I afford it?

When it comes to planning for a safe and secure retirement, long-term care (LTC) can be a confusing and unaddressed challenge to many families’ financial security. Some of the hesitancy can be pinned on human nature—we don’t like to think about the unpleasant possibility of needing help being fed, bathed, or using the bathroom. Some might think it won’t happen to them; others can’t think that far down the road.

Additional Hurdles:

- Underestimating the cost of care

- Knowing the cost and not comprehending how to pay for care

- Mistakenly assuming Medicare and health insurance will cover LTC needs

- Traditional long-term care insurance has had a bad rap, due in part to significant premium hikes on early policies that were initially mispriced and delivered inconsistent benefits.

- Some find it problematic to pay a great deal of money for something they may never use.

Planning Can Help

While it might sound simplistic, handling these issues starts with a conversation to get the ball rolling. The act of discussing and planning can help alleviate the emotional, financial, and physical stress related to LTC. According to a 2018 study by Genworth, of those who prepared, 66% wished they had taken steps to plan sooner.

In those situations where LTC was needed, 84% of caregivers and 75% of recipients report they would have “done things differently.” Without a plan, you may have to make in-the-moment and subpar decisions to help a loved one. Crisis planning can end poorly.

How to Pay for LTC

The good news is that planning and products have evolved. Let’s dig into what can be done today to help ease the worry and challenges posed by growing older.

1. Medicare vs. Medicaid

Several strategies are at your disposal to help cover costs associated with LTC.

But not Medicare. Most people believe their LTC needs will be covered by Medicare. Medicare will pay for short stays in skilled nursing facilities that provide rehab or therapy services after a hospital stay. However, Medicare does not cover long-term care.

In contrast, Medicaid covers long-term care costs at home or in a skilled nursing facility. In fact, Medicaid is the primary payer for long-term care services. The biggest issue is that many people who need long-term care never qualify for Medicaid assistance. Here’s why:

- Income thresholds. Individuals must have limited income and assets to qualify. If one is above those thresholds, current assets must be “spent down” before utilizing Medicaid.

- Lookback period. There is a lookback period when assessing eligibility. In most cases, a review of financial records, going back five years, will seek to uncover whether assets were sold or given away to meet your state’s asset limit.

- Medicaid pending. Even if an individual qualifies, there might be a period called “Medicaid pending” where benefits have been denied or the recipient not approved. This can be quite stressful, especially if immediate care is needed. Not all facilities will accept a person who is in pending status.

- Bed availability. Additionally, a bed may not be available at a preferred facility.

2. Self-Funded Long-Term Care

Perhaps an individual cannot qualify for traditional long-term care insurance (LTCI) due to existing health issues. In this situation, they will have to use savings or investments to pay for care out of pocket and should set money aside for two to three years of LTC. Planning early is key to success.

The downside to this approach is not knowing how many years of care may be needed. Alzheimer’s has an average life expectancy after diagnosis of eight to ten years, according to the Alzheimer’s Research and Prevention Foundation. The funds to cover five years in a facility may be available but would deplete all assets in year six with nothing left for beneficiaries.

3. Use Pre-Tax Savings, Like an IRA

Another strategy designates pre-tax savings (IRA) to purchase LTC protection. Retirement assets can be surprisingly substantial, and a good source for LTC needs. Some things to think about:

- Tax change alert: The SECURE Act of 2019 instituted an important change to lifetime “stretch” IRA options. Previously, non-spouse beneficiaries were allowed to stretch their required minimum distributions (RMDs) over their life expectancies, thereby extending tax implications. The SECURE Act now requires non-spouse beneficiaries to take all distributions within a 10-year period following the death of the retirement account owner. This compels the beneficiary to pay taxes sooner.

- As a solution, the IRA owner could purchase a hybrid life insurance policy with proceeds from the IRA and gain LTC coverage with a death benefit. If long-term care is not needed, the death benefit flows to the estate tax-free.

Purchasing a hybrid life insurance policy with proceeds from an IRA means if long-term care is not needed, the death benefit flows to the estate tax-free.

4. Explore Roth IRAs and Backdoor Roth IRAs

Assets pulled from traditional IRAs are taxed as ordinary income. Luckily, Roth IRAs are funded with after-tax monies, and feature tax-free growth, tax-free withdrawals, and no RMDs. Earmarking a Roth for LTC costs or premiums may be an excellent strategy.

Higher earners will also benefit by using what is called a backdoor Roth IRA. This is an IRS-permitted method allowing one to fund a Roth IRA even if income is higher than IRS limits for standard Roth contributions or conversions.

Funds can be used to pay for LTC costs or pay premiums for coverage. Please note: Taxes must be paid on monies converted to a backdoor Roth IRA and it will likely count as income, possibly pushing one into a higher tax bracket.

5. Health Savings Accounts

A health savings account (HSA) is a hidden jewel in your LTC and retirement planning arsenal. The approach is simple, effective, and tax-advantaged.

- Contributions to an HSA reduce annual taxable income and grow tax-deferred until monies are used to cover eligible healthcare expenses.

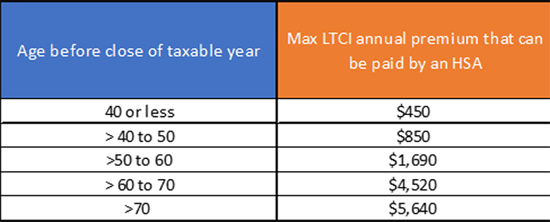

- HSA withdrawals for medical expenses and LTCI (long-term care insurance) are tax-free when they meet certain guidelines. Based on age, one can use HSA monies tax-free to pay LTCI premiums (see Figure 1). To make this work, the long-term care policy must only cover long-term care services. Most LTCI policies qualify.

Figure 1: 2021 Amount of HSA Assets That Can Be Used to Cover Long-Term Care Insurance

Source: Internal Revenue Service

- After age 65, the money can be used for absolutely anything without penalty (although ordinary income taxes will be due on withdrawals). While there are annual contribution limits, there is no maximum accumulation limit for an HSA. For example, 2022 annual contribution limits are: $3,650 self only, $7,300 family contribution limit, plus a $1,000 catch-up provision for those age 55 and up.

6. Existing Life Insurance

There are a few ways an existing life insurance policy can help fund LTC. Individuals may have traditional life insurance policies that could be sold to a life settlement company. Proceeds will depend on the age and health status of the policyholder. Some life insurance policies offer “accelerated benefits” in the form of a cash advance against the death benefit. Some insurance carriers may make an accelerated benefit available even if it is not in the contract. Either way, the upside may outweigh any reduction in death benefit for beneficiaries.

Let’s Finish Where We Started—If Not Now, When?

Thinking about long-term care can be difficult, but as they say, “Necessity is the mother of invention.” Challenges along the way have led to innovations in recent years, and there’s reason to feel hopeful about one’s ability to address the long-term care conundrum.

Planning for Long-Term Care

Thinking about paying for these costs on your own feels overwhelming, but you have options. The three most common options include:

- A stand-alone LTC insurance policy. These policies have been decreasing in popularity because the annual premiums can be quite expensive and policies usually don’t offer any cash benefits to survivors. Therefore, stand-alone policies may only be good for those who can afford the premium and are relatively certain they will need LTC coverage later in life.

- Addition of a LTC rider to an existing life insurance policy. If you have a permanent life insurance policy, many insurers offer an add-on called an LTC rider. If LTC is needed, the funds are available through your policy’s death benefit. If you don’t spend the total benefit available, your beneficiaries will receive the balance upon your death.

- LTC add-on to a fixed or indexed annuity. If you own an annuity, you may be able to purchase a similar add-on, in which additional amounts would be added to your monthly annuity income if you ever need to pay for LTC.

No matter which option you consider, it is important to plan ahead. Premiums increase as your risk of serious illness increases, meaning younger people typically have lower overall premium costs. Because of this, LTC planning is generally recommended for individuals between the ages of 50-60.

With Georgia’s population of 85+ seniors set to quadruple over the next 30 years, it’s more important than ever to assess your family’s LTC needs.

How We Can Help

Thankfully, you are not alone in planning for the possibility of LTC. Whether you are just starting to think about retirement, or it’s right around the corner, Live Oak Wealth Management is here to help guide you through the process. We have the tools and expertise you need to plan for a retirement with the possibility of LTC. Call our office at 770-552-5968, email [email protected], or click here to schedule an appointment online.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.