Last week, the headwinds on global stocks and bonds grew stronger thanks to ill-timed and ill-conceived government policy from the UK. The new Truss administration unleashed another round of massive stimulus, and in the process sent global bond yields surging, and by default, equity prices falling. It’s not an exaggeration to say this event is the reason the S&P 500 hit a new low Monday. Global yields are surging, as is the dollar, and this is pressuring global stocks. So, I want to make sure you understand 1) Why it’s happening, 2) What it means for markets, and 3) What fixes it.

What Happened:

New UK Prime Minister Truss announced a massive new tax cut and stimulus plan for the economy. The plan included 60 billion pounds in aid to UK citizens and corporations to offset higher energy prices this winter. In addition, the plan abolishes planning additional income tax rates, cancels a planned corporate tax rate increase, eliminates caps on banker bonuses, and cuts the stamp duty tax. In short, the plan has the UK spending a lot of money but taking in a lot less. Why is this a problem? Because too much government spending was partially responsible for the inflation mess the world is in, and doing the same thing again will only make it worse!

First, unleashing a massive stimulus plan is not going to help the inflation problem. It will make it worse. Second, the UK government finances itself via selling bonds, just like the U.S. This is the worst bond market in multiple decades, so enacting a fiscal plan that only ensures the UK government will have to issue more bonds at a time when interest rates are spiking ensures the UK government will pay a lot more in interest to its borrowers. It’d be the personal equivalent to running up a large credit card balance when rates are at their highest! It just makes paying that interest in the future more difficult. Third, it puts the UK government somewhat at odds with the Bank of England. The Bank of England is raising rates to try and bring inflation down. Crashing the pound (which the Truss administration has done) only makes taming inflation more difficult for the BOE.

Why Does This Matter to You?

First, it has injected massive volatility into markets that need to be stable right now. The British pound is trading like a penny stock. At the lows on Monday night, the pound was down nearly 9% in two trading days! Then it bounced nearly 4% Monday morning before dropping to close down 2%. More important than the pound volatility is the massive upward pressure that rising GILT yields are putting on the rest of the world. A week ago, 10-year GILT yields were 3.30% (GILTs are UK government bonds, their equivalent for U.S. Treasuries). On Tuesday, the 10-year GILT yield was 4.28%. That’s a 95 bps increase in only a few days! That increase in GILT yields is pulling up other global bond yields. The 10-year Treasury yield is up nearly 30 bps in a week, while 10-year German bund yields are nearly 40 bps higher—and literally nothing has happened in the U.S. or EU to justify those moves (it’s all a function of exploding GILT yields).

Combine it all: Additional economic uncertainty, intense volatility in traditionally stable assets, and higher bond yields—it’s no surprise that stocks have been under pressure since Thursday.

When Does it Stop?

The pace of the decline in the pound and rise in GILT yields is the big problem, so the fastest way for this to stop would be for the Bank of England to announce a surprise interest rate hike. That would stabilize the pound and bring 10-year GILT rates lower as the market prices in lower inflation and lower growth. That did not happen, however. Instead, the Bank of England issues a non-specific “we’re watching markets” message, and for those of us who lived through 2008, we know how markets react to those non-specific platitudes. That was proven again as the Bank of England announcement resulted in the immediate decline in global stocks (the S&P 500 turned negative after that announcement), a drop in the pound, and an increase in bond yields. Looking forward, the Bank of England needs to step in and help stabilize the pound via a rate hike or very hawkish rhetoric, because the longer this extreme volatility lasts, the more likely it is to cause some sort of financial stress.

Here is the headline from Wednesday’s Wall Street Journal:

The financial conditions became so severe that the Bank of England had to step in and buy UK government bonds. From the WSJ:

The Bank of England on Wednesday said it would buy UK government bonds with long maturities “on whatever scale is necessary” in an effort to restore order to the market after a large set of government tax cuts sent borrowing costs soaring.

The furious selloff in UK government debt in recent days ripped through normally staid parts of the financial markets. Pension funds and insurers who hold financial derivatives tied to UK debt in particular faced the possibility of severe losses, according to analysts. The Bank of England stepped in to try to stop those losses from running out of control, analysts said.

The Bank of England said that in the days since the government’s tax announcement, UK asset prices have suffered a significant decline that could weaken the country’s financial system and economy if left unchecked.

“Were dysfunction in this market to continue or worsen, there would be a material risk to UK financial stability,” according to the Bank of England. “This would lead to an unwarranted tightening of financing conditions and a reduction of the flow of credit to the real economy.”

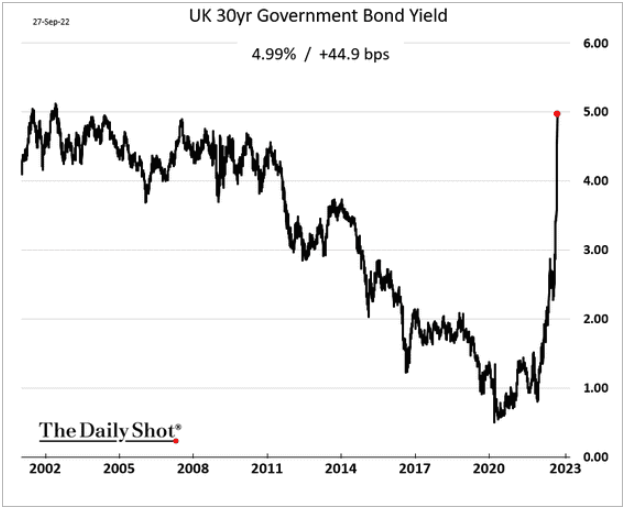

Here is a chart of the UK 30-year government bond yield. The yield has been in a parabolic move over the last several weeks, which is why the Bank of England had to step in and buy long-term UK government bonds to try and stabilize their financial markets.

While this announcement will provide some short-term relief from spiking yields, it doesn’t solve the inherent problem in the UK. Here’s what I mean: The British pound has fallen sharply and 10-year GILT yields have risen sharply in reaction to the Truss government’s fiscal spending plan, which aims to give money to British citizens to counter high electricity bills this winter, while simultaneously cutting lots of taxes (which will also stimulate the economy). This policy is, oddly, directly at odds with what the Bank of England is trying to do. Like every other developed central bank in the world (except Japan), the BOE is dramatically hiking rates to tame massive inflation (over 10% per year in the UK). Literally, on one hand, the Truss government has unleashed massive stimulus which will put upward pressure on inflation, while on the other hand, the Bank of England is aggressively hiking interest rates to try and lower that very same inflation!

Just like a bank would frown at the news that a heavily indebted borrower had decided to massively increase their debt load, global bond and currency markets frowned at the UK when Truss announced a plan that would stimulate inflation and simultaneously make pounds and GILTs less valuable! Not surprisingly, the market reacted by selling both! For now, the announcement has worked, but for trading in GILTs and the pound to return to normal, one of two things has to happen: 1) Truss must scale back (or ideally abandon) her fiscal spending stimulus plan, and/or 2) The Bank of England must announce a massive rate hike that will effectively offset Truss’s fiscal plan. If it seems like these two are on opposite sides, then you understand this correctly! And that’s why it’s so strange.

Why Does This Matter to Us?

It matters to us because basically the sole reason the S&P 500 made a new closing low and intraday low was because of the GILT-inspired spike in Treasury yields, and the pound-inspired rally in the dollar. Positively, the Bank of England announcement prevented a sudden collapse in stocks. But for this to become sustainable, the UK must get its proverbial act together and have the BOE and the Truss administration work together—the way we’d expect from a developed economy!

Bottom line, the markets do not need an injection of more uncertainty right now, as it already pressured stocks to fresh 2022 lows. If that can go away, the outlook for U.S. stocks and bonds will improve, although it’ll still be far from an all-clear.

We will continue to keep you updated.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stockbroker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.