The August inflation report was released Tuesday morning and came in a few tenths of a percentage higher than expected, which is a major reason why the Dow Jones Industrial Average declined -1297 points (-3.94%), the Nasdaq declined 632 points (-5.16%) while the S&P 500 declined 177 points (-4.32%) while interest rates increased on Tuesday.

August’s CPI (a measure of prices paid for things like energy, housing, and healthcare) showed an 8.3% increase over this time a year ago. That’s down from the 8.5% annual increase in July and 9.1% in June, but it was above Wall Street’s consensus expectation of 8.1%.

A couple tenths of a percent in the wrong direction sent the markets plunging, with the S&P 500 Index selling off roughly 4% today, and the tech-heavy Nasdaq Composite Index down about 5%. It was the market’s biggest one-day drop since June 2020. This shows you just how sensitive and uncertain the topic of inflation is for the stock market.

Had this one inflation number come in at 7.9% or 8%—or anything lower than the 8.1% investors hoped for—the markets likely would have rallied. That’s what happened last month when July’s inflation reading was lower than the 8.7% investors expected. The S&P 500 Index rose 2% that day, and the Nasdaq jumped 3%.

This illustrates what a fine line the market is straddling right now. These are extreme reactions considering we’re talking about a difference of a few tenths of a percentage point.

Here is a headline from The Wall Street Journal:

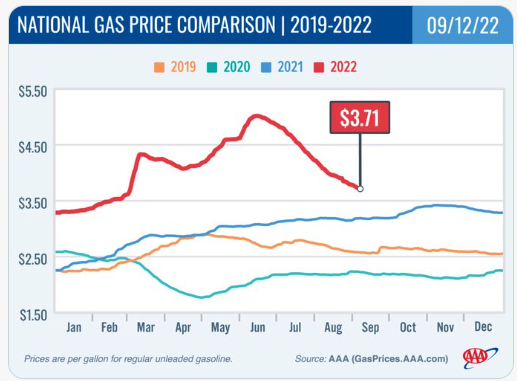

Much like July’s report, the only notable decrease in inflation came from energy prices. Gas prices in the U.S. moved down to $3.71/gallon (national average), 26% below their all-time high in mid-June and at their lowest levels in 6 months. The prices for shelter, medical care, household furnishings, new vehicles, motor vehicle insurance, and education were among those that increased over the month.

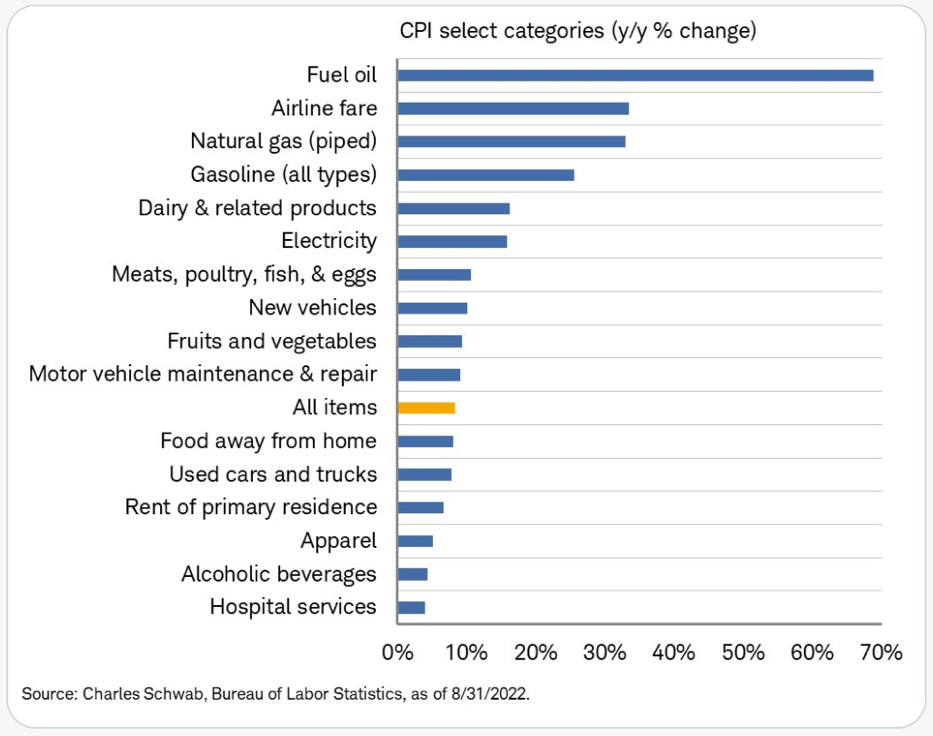

Here is a chart illustrating the increase in the top categories with the largest change in prices over the last 12 months. Even though we have seen energy prices decline over the last several months, over the last 12 months, fuel oil, natural gas, and gasoline continue to be up 30%+. The only other category that was negative in August were used cars and trucks, at -.10%.

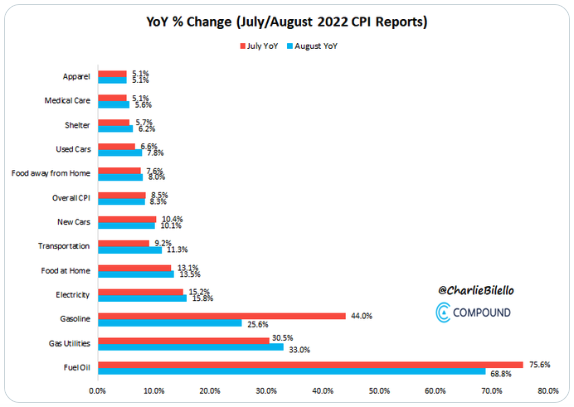

Following is the August CPI report vs. July. The report illustrates a lower year-over-year (YOY) percentage increase in gasoline, fuel oil, and new cars. The report also illustrates a higher year-over-year percentage increase in gas utilities, transportation, used cars, electricity, medical care, rents, food at home, and food away from home.

The Federal Reserve meets again on September 20-21. There is a high probability that Fed Chairman Jay Powell will increase interest rates by another .75%, bringing the Fed Funds Rate to 3.00%. In a speech at their annual Jackson Hole meeting on August 25th, Federal Reserve Chairman Jay Powell delivered a stern commitment to halting inflation, warning that he expects the central bank to continue raising interest rates in a way that will cause “some pain” to the U.S. economy. In addition, Powell said in his speech, “We are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2%.” Looking into the future, the central bank leader added that “restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy.”1 The continued high inflation numbers we are

experiencing will solidify the need for another .75% increase next week and the potential for more interest rate increases at the Federal Reserve’s meetings in November and December.

Certain prices will tend to be “stickier” or stay at elevated levels due to input costs. In addition, how many companies do you know that voluntarily lower their prices? Not many. Even though we have seen energy prices decline over the last several months, energy is a big cost for most companies and may take a while to filter through to lower costs.

Stock Market Outlook

This market is now presenting us with one of the most uncertain times I have dealt with over the last 13 years at our firm. And the month of September will likely be key to a resolution of the uncertainty. We are now approaching an apex to the point of decision for the market. Based on our methodology, it is clear that the market is now at a major crossroads that will determine the next 500+ moves. Yet it still has not tipped its hand as to the resolution. In fact, I cannot remember another time frame wherein the market was at a crossroads with such a significant and diametrically opposed resolution—but we are now at such a point in the market.

The stock market is currently in a position to either go up approximately 500 points to 4400 or down 500 points to a new low of 3430. These are two diametrically opposed extreme potentials in the market, which will lead to a 500+-point resolution in exact opposite directions. That is why I noted at the start of this market update that I do not recall being in a market posture with such significant uncertainty. The manner in which I expect that this uncertainty will resolve will only be seen as to how far this decline goes, and how far the next rally advances will be the difference in the next 500+-point move in the market. We need to see the S&P 500 reclaim 4175 to mount any kind of bullish price action.

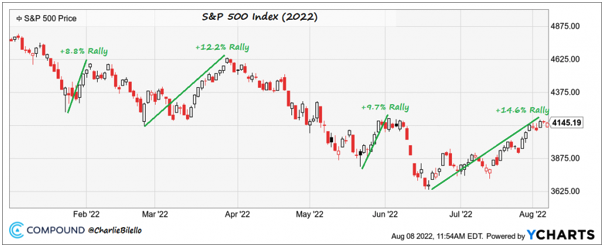

The stock market continues to be in a “show me” state and has to prove to us that the lows are in while presenting positive price action that could lead to new highs. Here is a chart showing the stock market rallies which have turned into new lows no fewer than four different times this year:

In summary, the nature of the market reaction over the next few weeks will provide us with a strong clue as to whether we have begun a rally to 5150SPX+, or if we need one more loop lower toward 3400SPX before that rally begins.

How We Can Help

If you would like to schedule a review and planning meeting, call our office at 770-552-5968 or email [email protected]. Or, if you prefer, you can simply click here to schedule an appointment online.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.