The first six months of 2022 were a nightmare for the financial markets. Both stocks and bonds declined significantly at the same time. This doesn’t happen very often, especially not for two consecutive quarters. In fact, you could argue we just lived through one of the worst six months ever for stocks and bonds.

That’s the bad news. But I also have some very good news, which we will discuss this month. July was an eventful month, both from the stock market as well as from the economic data that was released.

July’s global equity rally was concentrated in U.S. stocks. Monthly returns in U.S. equities scaled in typical “risk on” fashion, with small caps up more than large caps and the NASDAQ beating the S&P 500. The rally in European equities was roughly half that of U.S. stocks. Emerging markets basically went nowhere in July.

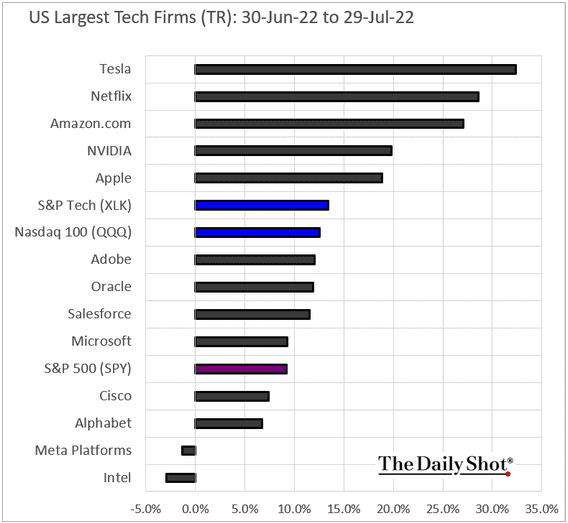

The standout July gains in Apple, Amazon, and Tesla are collectively responsible for 2.7 points of the S&P 500’s 9.1% gain in July, or 30% of the advance in U.S. large caps last month. Without these three stocks, the S&P would have only been up by 6.4% in July.

Stocks ended July higher across the board, with all three U.S. indexes rising in July. The S&P 500 recorded its strongest monthly gain since November 2020.

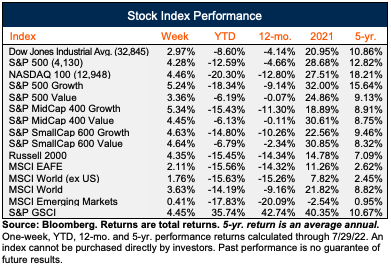

- The S&P 500 was up 9.1% in July, marking its best July since 1939, according to Dow Jones Market Data. The Dow industrials were up 6.7%, while the Nasdaq Composite rose 12%. All three remain down in 2022, as illustrated in the above performance chart. (1)

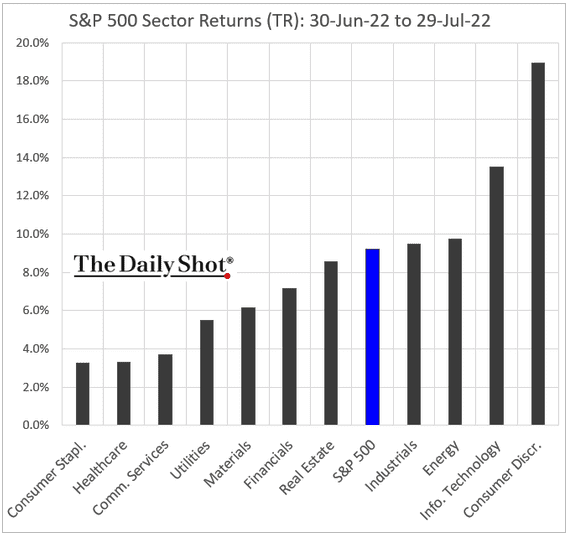

- Consumer discretionary and information technology stocks led the way up in July, with both sectors of the S&P 500 rising at least 13%.

- Bond yields retreated, with the 10-year yield dropping for three straight weeks to finish at 2.642%. (2)

Most U.S. large-cap sectors underperformed the S&P 500 last month. Leadership came from either cyclical names that had been beaten up recently over recession fears (Industrials, Energy) or tech-heavy YTD laggards (Consumer Discretionary, Tech itself). Classic safe haven sectors (Healthcare, Consumer Staples) were the worst performers in July, but remain some of the best performers YTD.

Technology companies have been some of the most beaten-up stocks this year, down anywhere from -10% to -40%+. July was a very good month for most of the large-cap technology companies such as Tesla, Amazon, Apple, and Nvidia. The only two negative large-cap technology companies were Facebook and Intel. We believe this to be very constructive price action where we can be selective in purchases of high-quality technology companies that will pay off as we go into the end of 2022 and beginning of 2023. The most recent earnings reports have shown that it pays to be bigger as these companies (such as Microsoft or Amazon) can withstand the current economic environment while most other companies lack the necessary scale or resources.

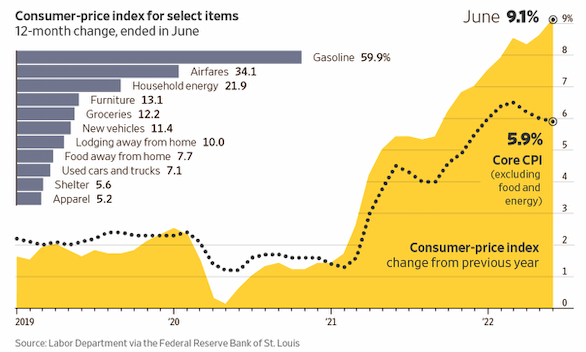

U.S. consumer inflation accelerated to 9.1% in June, a pace not seen in more than four decades, adding pressure on the Federal Reserve to act more aggressively to slow rapid price increases throughout the economy.

The Consumer Price Index’s advance for the 12 months ended in June was the fastest pace since November 1981, the Labor Department said on Wednesday. A big jump in gasoline prices—up 11.2% from the previous month and nearly 60% from a year earlier—drove much of the increase, while shelter and food prices were also major contributors. The June inflation number increased from May’s 8.6% inflation rate.

With the large inflation readings still being felt by many households and consumers, the question is will the Federal Reserve increase interest rates by 1% or stick to a .75% increase?

The Federal Reserve matched expectations by raising rates 75 basis points on July 28th. The Federal Open Market Committee (FOMC) stated job gains remain “robust” and the unemployment rate low, despite a still-tight labor market and elevated inflation. It noted inflation remains high due to supply-and-demand imbalances created by the COVID-19 pandemic. The central bank has now raised rates in four consecutive meetings, bringing the target fed funds rate to a range of 2.25%–2.50%. This is comparable to levels in 2019.

Wall Street was already in a good mood before the Fed’s announcement, with all three indexes up comfortably. Once the rate hike hit the news, stocks edged even higher after it was clear there would be no surprises.

But it was when Federal Reserve Chairman Jay Powell took to the podium and alluded to an eventual rate slowdown that we saw a sharp move higher in stocks.

From Powell:

The central bank said recent data on spending and production indicates economic activity is starting to soften. In addition, Chairman Powell indicated a willingness to slow the pace of rate hikes by acknowledging that the economy is slowing (which is what the Fed wants) and the full effect of the rate hikes have not yet been felt in the economy. Moreover, Powell said the Committee would react to growth, labor market and inflation data (becoming data dependent) instead of only focusing on inflation data. Fed Chair Powell also mentioned that it may be appropriate to slow the pace of rate hikes in the coming months which also opens the door for potential rate cuts in 2023.

In June, the central bank had significantly raised its outlook for interest rates. At the time, policymakers predicted that interest rates would end the year at around 3.4%, almost double their March forecast of 1.9%. For 2023, the Fed guided for interest rates of 3.8% compared with the prior 2.8% projection. And for 2024, it guided for 3.4% compared with the previous 2.8%.

The FOMC also increased its projection for longer-run interest rates from 2.4% to 2.5%. This is important because that’s the equivalent of a neutral stance on rates (i.e., one that neither hurts nor helps the economy). Based on that guidance, policymakers have now achieved their near-term goal of getting interest rates to neutral sooner than later. Still, the Fed will hold three more meetings, in September, November, and December, to raise rates potentially by another 1%. That means a rate increase of 0.5% is likely in September and then 0.25% each in the last two.

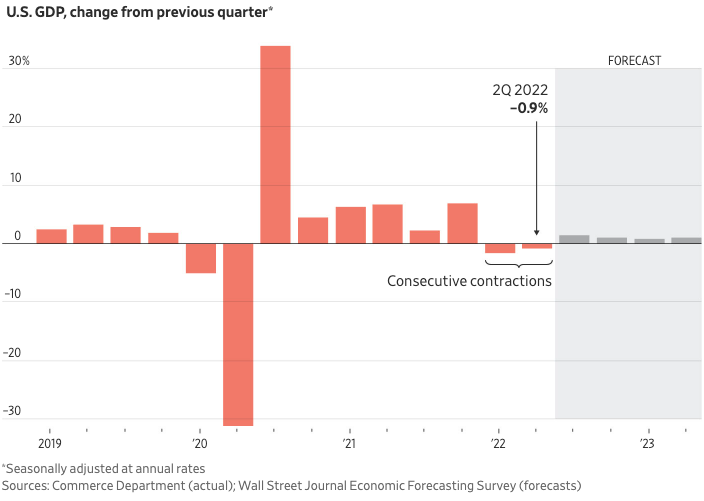

The U.S. economy shrank for a second quarter in a row—a common definition of recession. Gross domestic product, a broad measure of the goods and services produced across the economy, fell at an inflation and seasonally adjusted annual rate of 0.9% in the second quarter, the Commerce Department said Thursday. That followed a 1.6% pace of contraction in the first three months of 2022.

The report indicated the economy met a commonly used definition of recession: two straight quarters of declining economic output.

The official arbiter of recessions in the U.S. is the National Bureau of Economic Research, which defines one as a significant decline in economic activity, spread across the economy for more than a few months. Its Business Cycle Dating Committee considers factors including employment, output, and household income—and it usually doesn’t make a recession determination until long after the fact.

We wrote an article recently titled “Is a Recession On the Horizon?” which you can read here. We discussed the different economic data points that help determine if the U.S. economy is in a recession. The problem today is that we are facing multiple conflicting data points in this confirmation-bias economy. For example, do you want to see a recession? Just look at GDP, interest rates, and retail and consumer sentiment. Don’t want to see a recession? Just look at the labor market, personal income, and travel/leisure services.

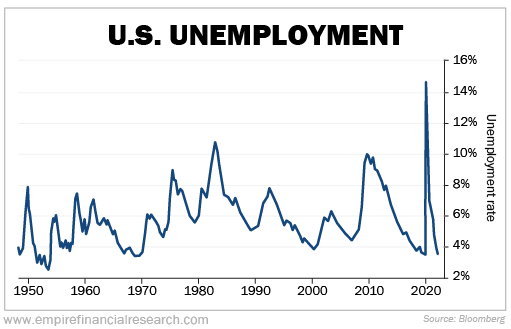

In the past 60 years, the U.S. has never had a recession without a preceding spike in initial jobless claims; and far from seeing such a spike, the labor market is extremely tight. The U.S. unemployment rate is 3.6%, the lowest level since the start of the pandemic, and only 0.1% above the 50-year low reached just before the pandemic in February 2020.

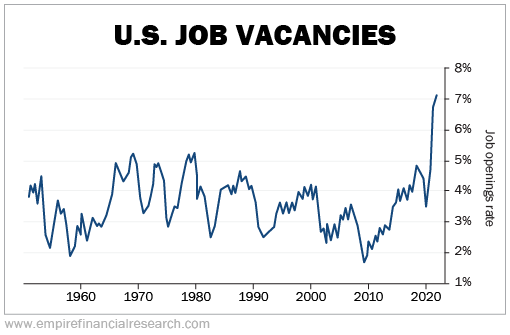

Meanwhile, the job vacancy rate is at an all-time high:

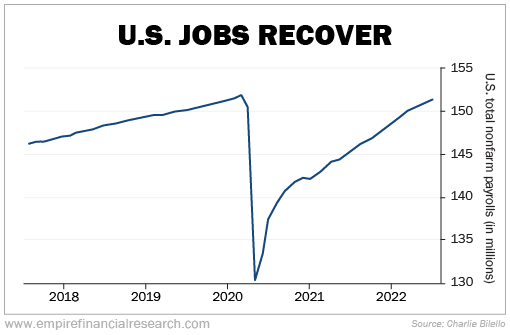

Additionally, the U.S. has almost fully recovered the jobs lost in the early months of the pandemic:

To me, what really matters for the stock market is a combination of consumer spending, corporate earnings, inflation, interest rates, and valuations—and in these areas, the story is solid. As for inflation, some important components are moderating.

The prices of most commodities have fallen considerably recently. Copper is down nearly 30% from its all-time high in March. Corn, wheat, and soybeans are all down over 25% from their highs and below the levels they were at before Russia invaded Ukraine. Used car prices are down 7% over the last six months, and the price of energy products (most importantly, oil, natural gas, and the price at the pump) have also fallen sharply.

Yes, the economy is slowing, but to the extent there is a recession, I expect it to be mild and short, which is already reflected in lower stock prices pretty much across the board this year. Keep in mind, the stock market is a forward-looking indicator. So, whether we are in a recession or not, bull markets almost always begin before a recession ends. Stocks discount current economic conditions and do not wait for the data to confirm.

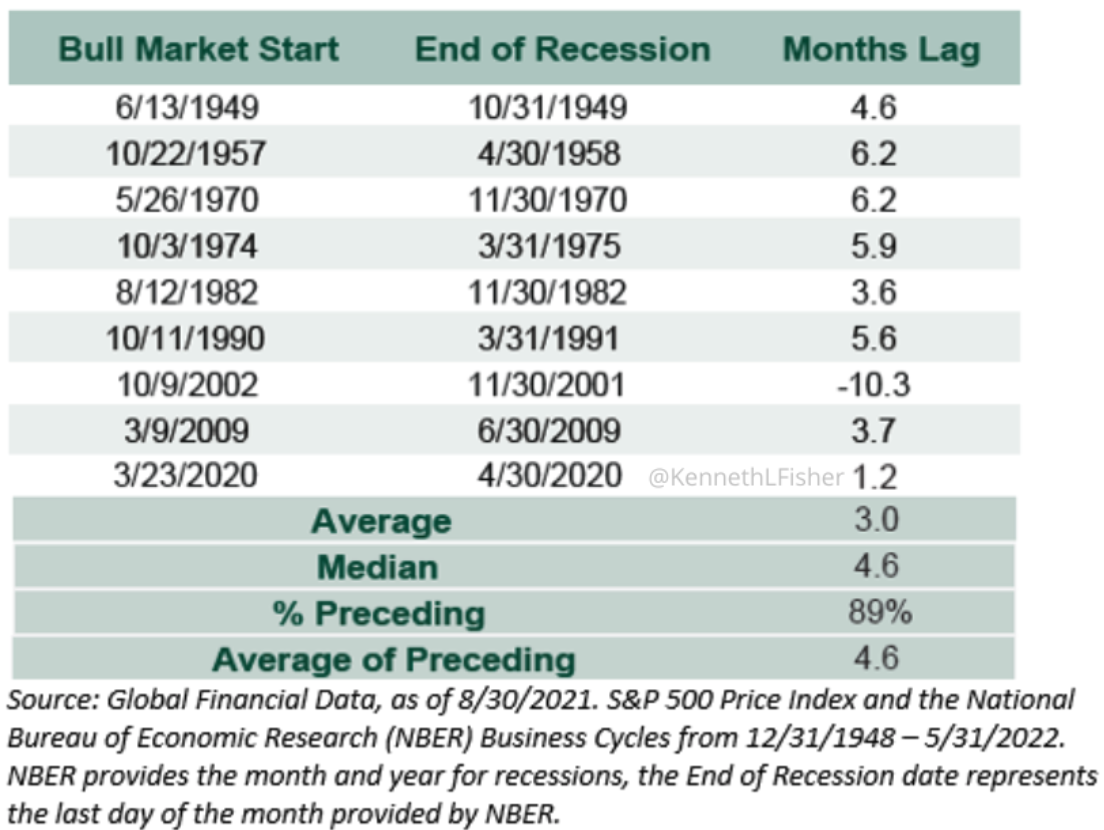

As the following chart shows, you will see the end of a recession and when the corresponding bull market starts. On average, there is a three-month lag time between a bull market starting and when the end of a recession has been declared, with a median time of 4.6 months. We have discussed multiple times that if you wait to invest until economic data starts to get better or when a recession is over, you will have missed the bulk of a move higher in the stock market.

How and When We Are Taking Advantage of Opportunities in the Stock AND Bond Market

There is never real clarity, and it is when uncertainty is highest that stocks tend to be cheap from a longer-term perspective. Investors need to look beyond the short-term volatility and invest in the longer-term healthy prospects for the economy. It is hard, if not impossible, to catch the bottom. But there are lots of great investment opportunities already.

We are in the more optimistic camp. Our perspective is that markets have it more right than wrong. U.S. economic growth is slowing, inflation should start to come down, the Fed can reduce the magnitude of its rate increases, and corporate earnings will remain strong enough to support investor confidence. U.S. equity markets are not totally out of the woods, but the Fed signaled we are now past the worst of its rate hikes, and Fed funds futures are even factoring in rate cuts for next year. There’s no Fed meeting for another seven weeks, so this clarity should continue to reduce volatility and act as a tailwind for U.S. equities.

The challenge has been, is this going to be a sustainable rally, or another fakeout? As you can see in the chart below, in March we had a stock market rally and then the market turned lower. In April, the stock market rallied and then turned lower again to make new lows. We saw the same thing happen in May and again in June where the S&P 500 made a new low at 3640. The market has made some great strides in terms of price action to indicate that the bottom was in June, however, we are in a “show me” market environment. It will still take us several months until we have a better idea as to how the market intends to take shape over the coming year. And the size and depth of the next drop will be one of the key determining factors. Next support is 3900-3950 on the S&P 500, which is where we will look to add to existing as well as new positions.

Our investment thesis this year has been to stick with large-cap and dividend-paying companies as they have the resources and ability to raise prices to sustain and do well in this current economic environment. By no means have these companies been spared the decline we have seen in the stock market, and in some cases, some have even seen larger declines such as the mega-cap technology companies. As we go through this earnings season, we are starting to see the advantage these types of companies have, which is being reflected in the rebound of their stock prices.

In addition to the large- and mega-cap companies, other areas we are buying include semiconductors, utility companies, real estate, and are allocating more toward growth over value. We believe it will be difficult to outperform the S&P 500, so our core portfolio will include the large- and mega-cap companies as well as the equal weight S&P 500.

The other area which presents some exciting opportunities is in the bond market. Specifically for non-retirement accounts, we believe municipal bonds are very attractive at current levels as well as investment-grade corporate bonds, long-term treasuries, and preferred stocks. Although we have seen the 10-year yield come down from 3.48% to 2.69%, we believe that over the next 12-18 months, interest rates will continue to decline, although we may see one more push higher in rates before we start a multi-month rally in prices (lower interest rates).

This market reminds me of the 2016-2018 time frame. For those that may remember, many thought the world was coming to an end during the 2015 market correction. Yet many different segments of the financial markets were setting up for a major rally that we were expecting in various risk assets across the world; I noted at the time that I was expecting a “global melt-up.” Currently, I am again seeing the potential for many markets to align for a rally for the coming year or so. This includes the potential for the bond market to strike a bottom over the coming months and begin a 12-to-18-month rally, along with various world equity markets. It is not often you see this type of alignment, but this is what these various charts seem to be suggesting.

We have been consistent that we would start to see the stock market improve in late summer/early fall. We seem to be following that path. Patience has been the key this year. Not being too aggressive in buying earlier this year as risk increased has been the key to capital preservation and living to fight (or, in our case, invest) another day. Sometimes the best thing to do is nothing. We have experienced investor sentiment reach levels we have not seen in decades, other than in March 2020, which will help lay the groundwork to potentially propel the stock market to new highs in 2023. We are excited about the rest of the year, and although we expect continued volatility going into 2023, we will continue to keep you updated.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.

_________________

(2) https://advisorscapital.com/portfolio/have-we-hit-bottom-yet/