By Matthew Gaude & Shawn McGuire

If you’ve been paying attention to the headlines lately, you probably know about the problems our current recording-breaking inflation is causing. Here are a few:

Consumers are paying more for almost everything we are purchasing. Commentators and analysts have been spending a lot of time debating about the dramatic rise of inflation and whether it is “persistent” or “transitory.” What may have seemed like a slight inconvenience at first is now becoming a much larger issue as people watch their purchasing power degrade right before their eyes.

As the holiday season approaches, many are wondering how much they can afford to spend on their loved ones or how seriously their retirement plans will be affected. These are valid concerns, especially with the heaviness of the ongoing COVID-19 pandemic. It’s completely understandable to worry and wonder when things will go back to normal.

The best way to assess the situation is to take a look at the factors surrounding why inflation is rising. The COVID-19 pandemic was unlike anything the world has ever seen. The entire global economy came to a complete standstill for the only time in modern history. It’s to be expected that the rebound from such a once-in-a-lifetime event will be just as enigmatic as the event itself. Here are some reasons why inflation is at an all-time high and what it means for your long-term purchasing power.

Inflation, Defined

According to Investopedia, inflation is “a decrease in the purchasing power of money, reflected in a general increase in the prices of goods and services in an economy.” (1) It can be characterized as persistent or transitory. Transitory inflation (2) is temporary and happens when supply doesn’t meet demand. If left unhandled, it can turn into persistent inflation, (3) which results in a more permanent increase in prices due to a continuous mismatch in supply and demand.

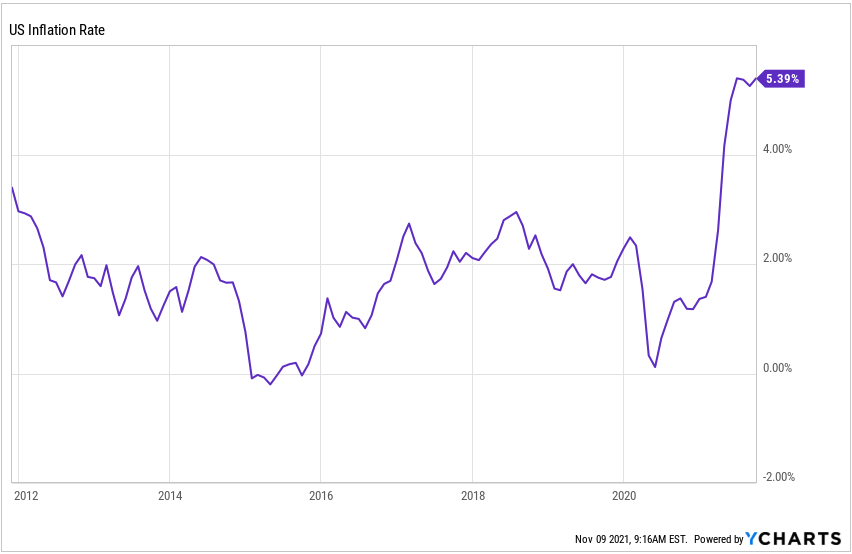

The Consumer Price Index (CPI) is a common measure of inflation. The most recent CPI report from September 2021 suggested that inflation has risen an astounding 6.2% over the past year! (4) That is significantly higher than the typical 2% rise we see in an average year.

Here is a chart of the U.S. inflation rate going back the past 10 years:

Why Is Inflation So High?

Fortune recently published a story comparing the costs of goods and services today to those costs one year ago. (5) See if the numbers below better reflect your personal inflation experience:

- Bacon: +19.3% over the past year

- Ground beef: +10.8%

- Pork ribs: +19.2%

- Chicken: +7.5%

- Fresh fish: +10.7%

- Eggs: +12.6%

- Apples: +7.8%

- Carbonated drinks: +5.3%

- Peanut butter: +6.2%

- Food from vending machines: +6%

- Beer (retail, not at a restaurant or bar): +1.6%

- Gasoline: +42.1%

- Propane, kerosene, and firewood: +27.6%

- Natural gas: +20.6%

- Rental cars: +42.9%

- Living room, kitchen, and dining room furniture: +13.7%

- Washer and dryer: +19.1%

- Women’s dresses: +9.5%

- Children’s shoes: +11.9%

- New cars: +8.8%

- Used cars: +24.4%

- TVs: +12.7%

- Hotel rooms: +17.5%

- Haircuts: +5%

Let’s add another huge one…rent.

From CNBC last month: (6)

Demand for single-family rental homes is showing no sign of easing up, and that is pushing rents through the roof, especially for the highest-priced properties…

Nationally, rents rose 9.3% in August, year over year, up from a 2.2% year-over-year increase in August 2020, according to CoreLogic.

That 9.3% average number masks many higher-price markets. For example, in Las Vegas, rents are up 15%. In Phoenix, 19%. And in Miami, they’re up a whopping 21%…again, in just one year. (7)

To better understand if inflation will last, let’s take a look at the factors contributing to its rise.

Devalued Dollar

When the COVID-19 pandemic first hit and the global economy shut down back in March 2020, many wondered if the economy was going to collapse. With millions of Americans furloughed or without jobs, drastic measures had to be taken to keep the country afloat.

The U.S. government instituted expansionary monetary and fiscal policies in order to pump money back into the economy. This was accomplished through stimulus payments, extended unemployment benefits, small business loans, moratoriums on evictions and student loan payments, and changes to the rules around required minimum distributions from retirement accounts.

This is all to say that the money supply in the U.S. increased at a rapid rate, jumping from $15.5 trillion in February 2020 to $18.8 trillion in October 2020, an increase of over $3 trillion dollars. (8) Though experts agree that these drastic measures were necessary to keep the economy from collapsing, they also agree that the increase in money supply devalued the dollar, meaning it takes more dollars to buy the same item since each dollar is less valuable. This was the beginning of the resurgence of inflation.

Supply Chain Disruptions

If there’s one thing that’s been in the news even more than inflation concerns, it’s supply chain disruptions. Since the vaccine rollouts and slow return to pre-pandemic life, companies have struggled to keep up with manufacturing and distributing goods. This is because many distribution centers cut their hours when the global economy came to a halt in anticipation of a huge drop in demand for consumer goods. The drop in demand, however, did not come.

As people across the globe spent days, then weeks, then months in their houses, demand skyrocketed for exercise equipment, home goods, and office supplies. Factories increased their output, but the distribution chains have struggled to get everything where they need to be.

Additionally, the increased production has also caused a shortage in raw materials, thereby exacerbating the gap between overall supply and demand for even basic items. As demand continues to outpace supply, prices are driven higher and higher.

The hope that supply chain issues would fade after a few months has proven drastically wrong, as recent delta-driven shutdowns in Asian country factories and ports, (9) as well as large buildups in American ports, (10) have only made matters worse.

Labor Shortages

Continued labor shortages are another factor driving inflation. In what is being called “The Great Resignation,” millions of workers across America have quit, retired, or considered quitting their jobs as they reevaluate the role that work plays in their lives. (11) As such, many companies are finding that they have to pay higher wages in order to attract and retain employees. These increased costs often get passed through to the customer in the form of increased prices for goods and services.

Government Spending

When the federal government passed the CARES Act in March 2020, there was a strong justification for doing so. Regardless, federal spending has created the largest government deficit in U.S. history. In the most recent fiscal year (ending September 30, 2020), the U.S. had a $3.129 trillion budget shortfall—that’s more than twice the $1.4 trillion deficit during the 2008 financial crisis. (12)

The economy is doing well, but it is largely due to the excessive spending in Washington. If you put enough money into the hands of consumers, coupled with the stress of the pandemic, they will spend. This has caused an increase in demand, which has served to push inflation higher. If the government continues to spend at the same rate and the supply chain problems persist, inflation will continue to rise.

How Does Inflation Affect the Stock Market?

If higher inflation is here to stay, it would seem to be a big risk to the stock market. It is possible an inflation scare could spook investors, but there’s no clear sign of this from the historical data.

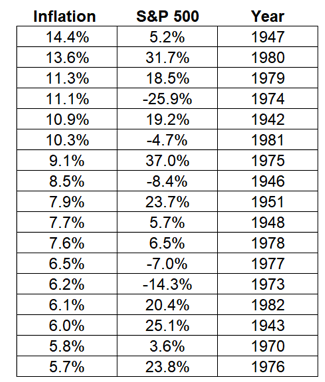

Here’s a table that ranks the highest calendar year rates of inflation with the corresponding returns on the stock market: (13)

The average returns for the S&P 500 in these years were 9.4%. That’s basically the long-term average over the past 90+ years.

Eight out of the 17 years were double-digit returns. Nearly one-third of the time, returns were more than 20% when inflation was the highest.

It does make sense the stock market would hold up in an inflationary environment if you think about it from the perspective of corporations. It’s not like most companies willingly eat higher prices themselves. Most of them pass along those higher prices to their customers. This is the environment that we are in currently.

So input costs rise but so do profits. In fact, some of the highest earnings growth historically occurred in the 1940s and 1970s.

What do these two decades have in common?

Both decades experienced high rates of inflation (as you can see from the table above).

So, Will Inflation Last?

Several points seem to indicate that the high rate of inflation we are experiencing right now is transitory in nature. The three main components of inflation mentioned above are all reactions to the pandemic and subsequent economic shutdown. Prior to March 2020, the U.S. economy was performing quite well and on track for another 2% inflation year. (14)

In fact, the Federal Reserve Chair Jerome Powell testified to Congress in June 2021 that “As these transitory supply effects abate, inflation is expected to drop back toward our longer-run goal.” (15) Since then, he tried to take the focus off of inflation, which he admitted was hot, by telling us that the Federal Reserve aren’t thinking about an interest rate liftoff, in response to inflation, because we aren’t at “maximum employment.” (16)

His exact words: “We don’t think it’s time yet to raise interest rates. There is still ground to cover to reach maximum employment both in terms of employment and in terms of participation.” (17)

Furthermore, the central bank is forecasting inflation to decrease to 2.2% in 2022 and carmakers expect their chip shortages to be resolved by 2023, an indication that supply chain disruptions should be resolved in the short-term future. (18) While it can be disheartening to hear that high levels of inflation will last through 2021 and possibly 2022, it’s good to know that it likely won’t be the rampant out-of-control inflation of the 1970s.

Chair Jerome Powell has told us that “maximum employment” was the condition to start increasing interest rates.

What’s happened since?

- October had a booming jobs report, with an unemployment rate that dropped to 4.6%, on 5% wage growth. (19)

- And then another effective oral COVID treatment option was introduced.

- And then Biden’s vaccine mandate for businesses was blocked by a federal court.

- And then the House passed the $1.2 trillion infrastructure bill.

- On Monday, November 8, the foreign travel ban was lifted.

This is a cocktail for maximum employment, which adds to the inflation pressures.

That said, it’s clear to everyone paying attention that inflation is being driven by factors other than bottlenecks at the ports. Wages. Shelter costs. Transportation costs. Food. Energy. Many of these are sticky. When they go up, they don’t come back down. This includes energy, in the current case. An agenda-forced underinvestment in fossil fuels has created a structural supply shortage. And there’s also this issue: a 30% growth in money supply over the past 18 months (inflationary).

Let Us Help You Protect Against Inflation

If you’re concerned about how inflation is going to affect your financial plan, know that you don’t have to go through it alone. Experts agree that emotional investing and making financial decisions based on the wild day-to-day changes of the market are the last thing you want to do in response to rising inflation.

Be sure to review your investment and retirement plans for proper diversification and risk tolerance levels. If you have questions or concerns about your portfolio, or would like to discuss how rising inflation could impact your financial plan, reach out to us today. At Live Oak Wealth Management, we have the tools and expertise to guide you through today’s high-inflation environment. Call our office at 770-552-5968 or email [email protected] to review your plan today. Or, if you prefer, you can simply click here to schedule an appointment online.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insight and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors. Seek tax advice from a tax professional. Neither APFS nor its Representatives provide tax, legal or accounting advice.

____________

(1) https://www.investopedia.com/terms/i/inflation.asp

(2) https://finance.yahoo.com/news/inflation-transitory-persistent-210149448.html

(3) https://finance.yahoo.com/news/inflation-transitory-persistent-210149448.html

(4) https://www.forbes.com/advisor/investing/why-is-inflation-rising-right-now/

(8) https://www.statista.com/statistics/1121054/monthly-m2-money-stock-usa/

(10) https://www.nytimes.com/2021/10/11/business/supply-chain-crisis-savannah-port.html

(13) https://awealthofcommonsense.com/2021/10/inflation-vs-stock-market-returns/

(14) https://www.statista.com/statistics/244983/projected-inflation-rate-in-the-united-states/

(15) https://www.forbes.com/advisor/investing/why-is-inflation-rising-right-now/

(17) https://www.npr.org/transcripts/1051478945

(19) https://www.nytimes.com/2021/11/05/business/economy/october-2021-jobs-report.html