Bonds are now top of news in the financial media. We’re all reading CNBC and Fox Business articles that stocks are plunging because the 10-year Treasury yield is rising. We are getting a lot of questions about yields in relation to the stock market, so I wanted to take time to provide an updated “lay of the land” on what’s happening in the bond market, and what it means to us as investors.

Why Are Bond Yields Spiking And Causing A Decline In Stocks?

Bond yields are not spiking because the Federal Reserve is getting less dovish. Instead, bond yields are spiking because the markets are anticipating a looming explosion in economic growth and, likely, inflation (both of which are negative for bonds). Current Q1 2021 GDP growth is estimated at 9%! And that’s before we get an additional ~$1.9 trillion in stimulus. The additional stimulus should come right before the U.S. economy totally reopens. All the while, the Federal Reserve is adamant about telling markets they have no plans to reduce liquidity (so no tapering QE, never mind hiking rates).

Now, all that positive economic growth is good for corporate earnings and for stocks, as long as yields don’t rise too quickly—and that’s the problem the past few weeks.

Rising yields are not likely to be a bearish gamechanger, because rising yields will not, by themselves, result in the destruction of the four pillars of the rally: historic Fed easing, massive fiscal stimulus, COVID vaccine optimism, and no double-dip recession.

An Increase In Interest From All-Time Lows

Treasury yields started moving sharply higher this past month (remember that as yields go up, prices go down). And while the upward march began in earnest last August when the 10-year Treasury yield bottomed at an all-time low rate of 0.50% based on closing prices, the past week we saw the 10-year break through the 1.25% threshold and touch 1.55%, a new high for the year. That’s a massive move in such a short time. And while it’s not the end of the world, it’s concerning considering how low rates have fueled recent economic growth.

The stock market naysayers have grown louder as a result. They’ve jumped on the inflation bandwagon, eyeing the change in yield. They’ve focused on the stimulus introduced by both the Federal Reserve and Congress into the financial system.

The implication of rising rates is it will drive up costs, either making it harder to invest in growth or hurt profitability. So, when asset managers worry about rising interest rates, the first sector to drop is technology stocks.

Currently, we have a situation where short-term rates have held tight while longer-term rates are moving higher. This distinction is important because the reason for the current rise in rates is likely due to the bond market pricing in higher economic growth prospects. Following is a chart showing the 1-, 5-, 10-, & 30-year Treasury rates going back 10 years.

We believe more good news on the economy will continue to push yields higher, but there are also forces in play that may help slow the pace down.

Why Are Higher Interest Rates Causing A Decline In Technology Stocks?

The core issue here is economic growth. Due to economic reopenings, stimulus, and vaccine optimism, global investors are pricing in a huge jump in economic growth, which is why yields are rising.

And this expectation of better growth is causing the unwind of last year’s flood into tech shares. During the pandemic, investors poured into tech for two reasons. First, the pandemic benefitted most tech companies; second, tech earnings growth is much less sensitive to broad economic growth than other market sectors. So, in 2020, courtesy of the pandemic, investors who wanted earnings growth had nowhere to go but tech. That, in turn, sent tech shares screaming into historically high valuations. But the looming reopening of the economy and acceleration in economic growth means investors can get exposure to earnings growth in sectors that aren’t as richly valued as tech. In a growing economy, financials, industrials, energy, and materials sectors can enjoy earnings growth, and those sectors trade at a much lower valuation than tech. So, investors are leaving tech for these “cheaper” sectors, and the 2020 flood into tech is now being reversed.

The fact that yields are rising while tech is falling is because they are both reacting to the same thing: expectations of better economic growth. And this rotation will continue until 1) tech reaches a more historically typical valuation or 2) growth prospects change.

The bottom line is that rising yields aren’t causing tech to drop; it’s just happening at the same time because growth expectations are surging.

What Are We Expecting For The Rest Of The Year?

We believe interest rates will continue to rise due to increasing growth and inflation expectations and, eventually, Federal Reserve (Fed) normalization. We believe yields will continue to move higher throughout the year. We also believe if rates move too high too fast, the Federal Reserve will intervene to make sure rising rates don’t become too restrictive and disrupt equity markets or the real economy. A number of consumer loans are influenced by the levels of the U.S. bond market, most notably mortgage rates. A more interesting question, at least to us, is not where rates will be at the end of the year but how quickly rates rise from here.

It seems there are opposing forces pushing against each other to determine the appropriate level of rates. On the one hand, growth and inflation expectations are pushing yields higher, while the prospects of potential Fed intervention and increased savings demands due to aging demographics (both U.S. and non-U.S. savers) may help keep rates contained. We’ll continue to watch how this dynamic unfolds and see who ultimately wins this tug-of-war. Who says fixed income markets are boring?

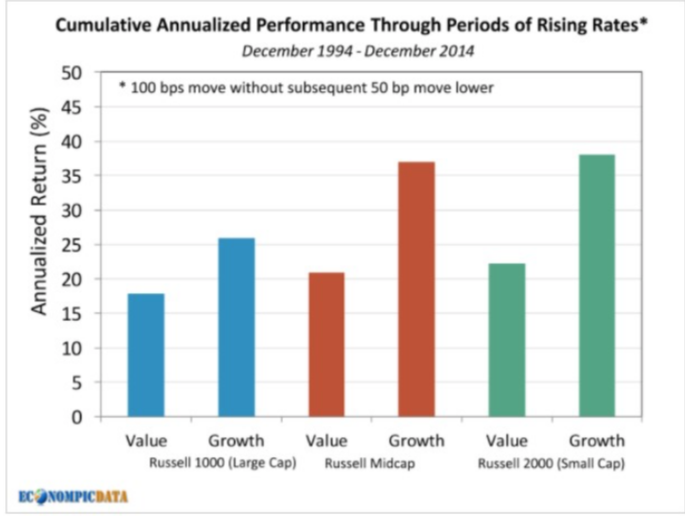

How Do Stocks Perform During Periods Of Rising Interest Rates?

Growth stocks do tend to do better when rates are low.

But it’s also worth remembering that the stock market generally holds up well when rates are rising. What happens to various segments of the U.S. stock market historically when rates rise 1% or more?

Surprisingly, growth has performed even better than value in large-, mid-, and small-cap stocks when rates have risen in the past.

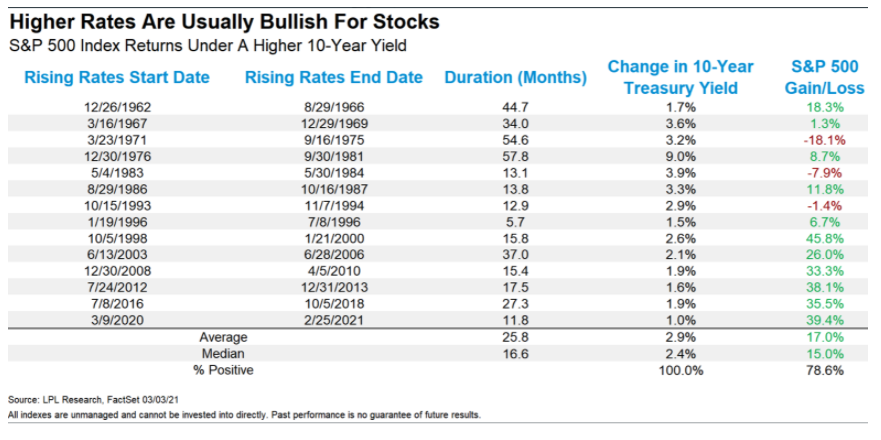

It may also be instructive to look at some historical examples of rising rate environments.

From 1954-1960, the 10-year Treasury yield went from 2.3% to 4.7%. In that time, the S&P 500 was up 207% in total (17.4% annualized).1

Then from 1971-1981, rates went vertical, rising from 6.2% to 13.7%. This period included sky-high inflation and the brutal 1973-1974 crash, but nominal returns were still pretty decent, at 113% in total (7.1% annual).2

From 1993-1994, rates shot up from 6.6% to 8.0%. The S&P 500 was still up nearly 12% in total despite some carnage in the bond market.3

At the tail end of the dot-com bubble, rates rose from 5.5% in 1998 to 6.5% in 1999. It didn’t matter. Stocks were up more than 55% (although that was followed by a 50% crash beginning in early 2000).4

From 2003 through 2007, rates went from 3.3% to 5.1%. The S&P rose nearly 83% (12.8% annualized) before the onset of the 2008 crash.5

And the latest rising-rate environment saw the 10-year go from 1.5% in 2012 to 3% by 2018. Even with the mini-bear market at the end of 2018, stocks were still up 131% in total.6

The problem with the current rate environment is we’ve never experienced interest rates this low before.

But rising rates, in and of themselves, don’t always spell doom for the stock market.

What Can The Federal Reserve Do To Stop Rising Interest Rates?

Federal Reserve Chairman Jerome Powell delivered a blow to the inflation camp’s argument, telling members of the Senate Banking Committee that he doesn’t expect inflation to “rise to troubling levels.”

The rate on the 10-year Treasury yield is tied to other interest rates; in particular, it’s tied to home loans. Banks and other financial institutions use it as a guide to set the rates on fixed- and floating-rate mortgages. So, when you buy a new home or refinance an existing home, the 10-year yield helps set that rate.

In addition, the U.S. 10-year Treasury is considered one of the safest investments in the world, not to mention the most liquid. So investors view it as a gauge of the domestic economy. When money managers are concerned about the growth outlook, they seek out the safety of those bonds. And when they’re encouraged that growth is headed higher, they tend to sell those bonds.

Starting last March, COVID-19 gripped the globe. Governments everywhere introduced social-distancing restrictions and shut down their economies to stop the spread. Asset managers needed to protect their clients’ funds. They sold risky assets like stocks in favor of safe-haven assets like bonds. And now with the economy rebounding, they’re selling bonds and investing that money back into stocks.

Now we’re coming up on the anniversary of those economic lockdowns. Gross domestic product (GDP) for the second quarter of last year plummeted 31.7%, one of the worst numbers on record. We haven’t seen anything like it since the Great Depression that began in the late 1920s.

But considering this fact, there’s an important point to remember: We’re going up against an easy comparison.

The economic statistics are about to lap some of the lowest-growth numbers we’ll ever see…and hopefully never see again. That means it’s going to be very difficult not to see signs of massive growth compared with a situation where there was virtually no growth. It’s going to look and seem like a big jump in inflation.

But the Fed isn’t buying it…

Federal Reserve Chairman Jay Powell stated the central bank expects a temporary move higher on base effects. But it doesn’t see any of the increased spending by the government having a long-lasting impact. And if for some reason there’s an unwanted move higher, the Fed has the policy tools available to deal with it.

Put another way, the Fed’s balance sheet is bigger than everyone else’s; it can step into the bond market at any time and increase purchases. If the 10-year Treasury yield was to rise because of selling pressure, the central bank can either keep it in check or even push it lower.

In addition, Powell said the job of restoring the economy isn’t done. He feels there’s still a long way to go, and he’s optimistic about the growth outlook for the second half of this year. And the central bank chief stated it will be a “long time” before it changes the policies it has adopted to restore full employment.

In truth, media, analysts, and stock market commentators just fit the narrative to what is going on at the time in the markets. In other words, it’s all noise and meaningless.

So, if you still don’t believe me, let me ask you this: Are markets not able to rally when rates rise? If you knew market history, you would know that markets have risen during times when rates rise and have also risen during times when rates fall, as we have proven in this article. So history tells us that the direction of rates is meaningless with regard to the trend of the stock market, and in our opinion will prove to be an excellent buying opportunity.

Stock Market Outlook

I have read many articles over the last year, and the one commonality I have seen, other than confusion, is the persistent name-calling by both investors and analysts alike. The rally off the March 2020 low took most investors and analysts by surprise. Most were looking for the next crash, which was certainly around the corner.

And, as the market continued to climb, they were all dumbstruck as to how the market could possibly climb when the COVID death rates were increasing and a significant part of the economy was in lockdown. I mean, it would be reasonable to assume the market would crash again based upon all these factors, right?

But they were all working under the erroneous assumption that the market is a reasonable environment. The truth is that the market is an emotional environment and does not care about reasons. Rather, reasons are what analysts and investors attempt to postulate in order to explain a market move after the fact.

And when the market did not turn down, but rather continued to scream higher and higher despite all the reasons being proffered by the masses for its inevitable next crash, we began to see analysts and investors calling the market names. Whether they called the market a “bubble” or “irrational” or “manic” or “risky” (or many other names), all they accomplished with their name-calling was evidencing their exasperation caused by their lack of understanding of the market environment.

And if you still doubt this perspective, and believe things like news or politics really matter to the market, consider why the oil complex has been rallying so strongly since election night despite a Biden win. Moreover, consider that the stock market rallied 1,500 S&P 500 points off the lows during some of the worst death rates being reported and during economic shutdowns seen throughout the country. If 2020 has not taught you a lesson about news or event following, then I’m not sure anything will.

So let’s enjoy the good times and the current “Roaring Twenties” as we have them now in the stock market. We are currently setting up for a major market rally for 2021 based on our research, likely lasting into 2022 and potentially into 2023. However, once this rally runs its course, I believe we are setting up what may eventually be entitled “The Greater Depression.”

I am still expecting one more pullback, which we are currently experiencing. Our downside target is 3,500-3,650, while the upper end of this support should hold this decline. This represents a decline of approximately -2.77% to -6.7% from current levels of S&P 500 of 3,754 before we see the next market rally to our target of 4,300.

And, yes, keep in mind that this is a pullback of the rally off the November low. Since we have not seen much in the way of pullbacks for many months, this may feel quite bad. But, in fact, this is still quite shallow thus far. Please stay focused on the bigger picture, as it is not likely that this bull market has ended.

It is up to you to view the market objectively in order to recognize when the next melt-up phase will take hold despite all the contrary news or noise presented around you. And that, my friends, is one of the most difficult lessons that Mr. Market teaches to those who do best within the financial markets. Oftentimes, you must unlearn that which you have been erroneously taught for decades in order to learn the most profitable lessons Mr. Market has to offer. That is also why individual investors tend to underperform the stock market benchmarks, because most investors manage by emotion.

So, to put it quite simply, we are rather bullish for 2021 as long as we retain the current market structure. Ultimately, this same larger market structure seems to be pointing up toward our next objective of 4,300 in the S&P 500, followed by 4,600, and then higher as we look toward 2022 and 2023 before the bull market off the 2009 lows comes to an end.

I still think we have many innings left in this baseball game. But, like all good things, this bull market will also come to an end.

About Matthew

Matthew Gaude is an *investment advisor representative and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. Working first as a commodity broker and then as a Business Development Manager for a national broker-dealer in previous jobs, he has the insights and experience to help clients understand the complexities of the market and implement strategies to minimize risk. To learn more about Matthew, connect with him on LinkedIn or visit www.liveoakwm.com.

About Shawn

Shawn McGuire is a financial advisor and the co-founder of Live Oak Wealth Management, a financial services firm in Roswell, Georgia. He serves the planning and investment needs of corporate employees, those approaching or in retirement, and 401(k) plan sponsors. He has worked in financial services since 2002 in positions ranging from financial advisor to stock broker and portfolio manager. As a CERTIFIED FINANCIAL PLANNER™ professional, he is trained to help clients with virtually all their financial needs. To learn more about Shawn, connect with him on LinkedIn or visit www.liveoakwm.com.

Securities offered through American Portfolios Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through *American Portfolio Advisors, Inc., a SEC Registered Investment Advisor. Live Oak Wealth Management, LLC is independently owned and not affiliated with APFS or APA.

Any opinions expressed in this forum are not the opinion or view of American Portfolios Financial Services, Inc. (APFS) or American Portfolios Advisors, Inc. (APA) and have not been reviewed by the firm for completeness or accuracy. These opinions are subject to change at any time without notice. Any comments or postings are provided for informational purposes only and do not constitute an offer or a recommendation to buy or sell securities or other financial instruments. Readers should conduct their own review and exercise judgment prior to investing. Investments are not guaranteed, involve risk, and may result in a loss of principal. Past performance does not guarantee future results. Investments are not suitable for all types of investors.